Amazon 1Q'26: Rosy Near-term but "Cloudy" Long-term

Amazon’s highlight from 1Q’26 was that AWS has accelerated to 28%, which was the highest growth rate in the last 15 quarters. In fact, looking at the guide, it appears even a more pronounced acceleration is likely for 2Q’26. I will talk more about AWS, but as I typically do every quarter, I will first start with non-AWS segments of Amazon.

Both North America and International segment experienced margin expansion YoY.

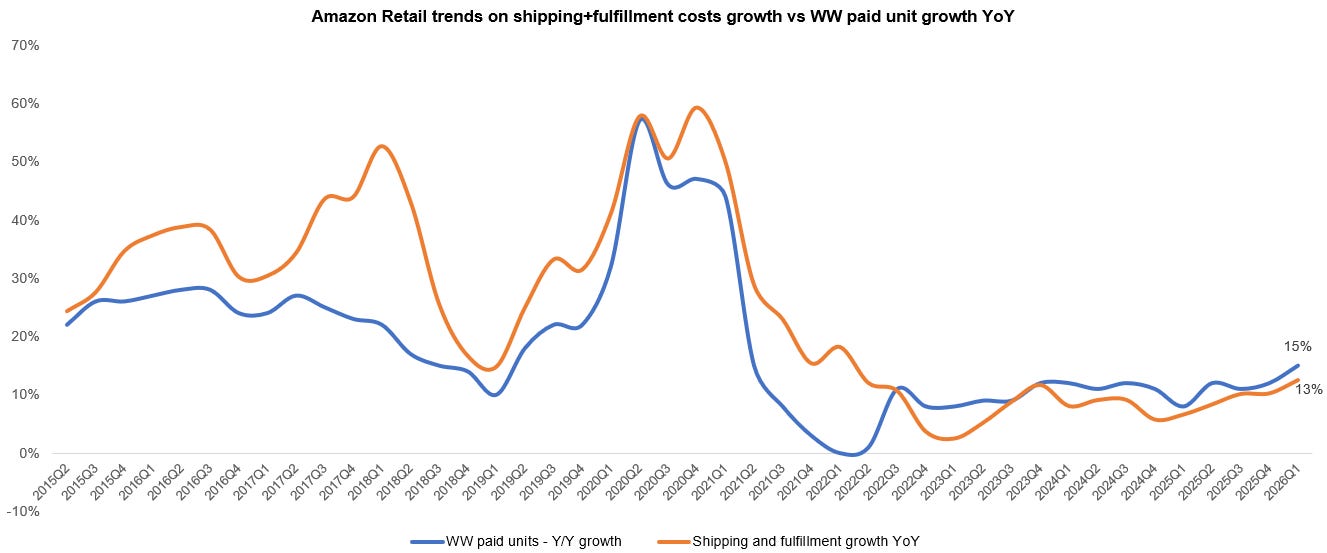

If you look at worldwide paid unit growth vs shipping+ fulfillment cost growth, you would notice that the latter used to consistently outpace the former pretty much all the time since 2015 until 3Q’22. Since then, unit growth has largely been faster than shipping+ fulfillment costs, indicating operating leverage in their logistics footprint.

The health of the core retail business remains in a very good shape. Units accelerated to 15% YoY, which was the highest since the tail end of Covid. What I found even more remarkable is that Amazon mentioned “in Q1, the average prices of products offered on Amazon.com decreased compared to the same period last year.” When I think about what has happened since 1Q’25 especially tariff and oil price shock, it is a pretty incredible stat.

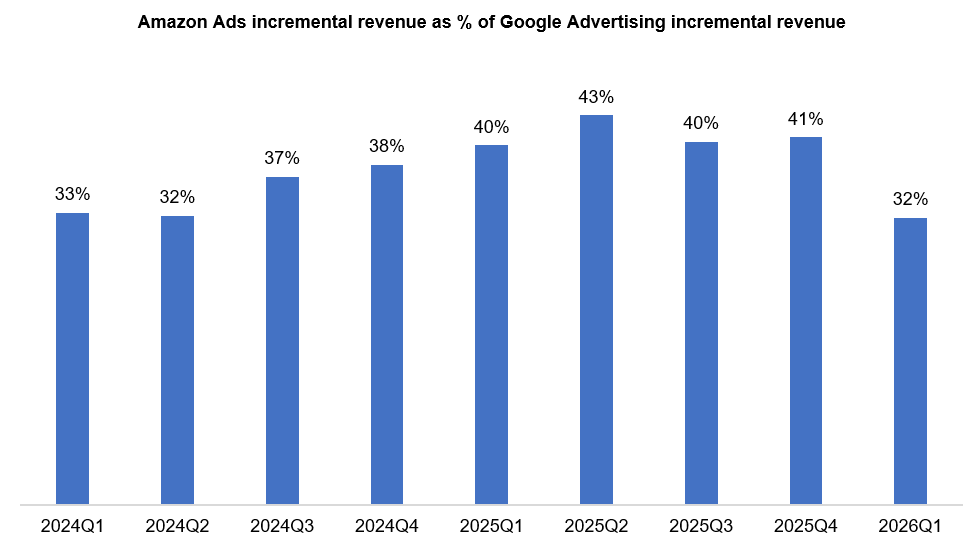

A big driver for retail profitability is advertising. Given Amazon ads are perhaps more of a competitor to Google than Meta, I pay close attention to Amazon’s incremental share in advertising compared to Google Advertising. It is interesting to observe a noticeable drop in Amazon ads incremental share compared to Google advertising which itself is losing share to Meta’s Family of Apps (FOA) ads.

For the last four consecutive quarters, Amazon ads grew at 22% rate (FXN). In contrast, Google advertising accelerated in each of the last four quarters from 10.4% in 2Q’25 to 12.6% in 3Q’25 to 13.6% in 4Q’25 to 15.5% in 1Q’26.

While I consistently made the case that AI is a massive tailwind for scaled digital advertising players, I suspect Amazon ads may be structurally positioned worse compared to Google and Meta. I will have much more sympathy to this thesis if I continue to see incremental share for Amazon ads (vs Google advertising) declining in coming quarters since I don’t want to extrapolate too much based on just one quarter. Why do I suspect this might be the case?

Amazon Ads is overwhelmingly bottom-funnel i.e. sponsored products served at the moment of purchase intent, where AI adds little ("buy AirPods Pro" doesn't need a reasoning model). Google Search, on the other hand, has always lived slightly further upstream (vs Amazon), where AI Mode and AI Overviews can genuinely improve the considered, comparative shopping query. AI also expands Google's ad inventory in ways Amazon's may not quite grow. Think shopping carousels inside AI responses, conversational query types that didn't previously exist whereas Amazon's inventory is structurally capped by SERP and product-page real estate that's already heavily loaded. Amazon mentioned Rufus which had MAU growth of 115% and engagement growth of 400%, but I wonder how Rufus is being used by customers. Personally speaking, I mostly ask Rufus to summarize reviews of a particular product on Amazon, but for more extensive product comparisons and considerations, I personally (and likely most customers) find general chat bots (Gemini/ChatGPT) more useful.

Of course, Amazon's first-party purchase data remains the highest-quality targeting signal in digital advertising, so I certainly don’t think Amazon ads business will be impaired, but Google's funnel position and inventory expansion can produce more incremental lift per dollar of AI investment, at least in this cycle. I’ll keep a close track and update my opinion accordingly.

A more nefarious bear case for Amazon ads is whether they become increasingly abstracted away by the OS layer. I share some of my readers skepticism of such bear cases, but given Google owns the OS layer, you can see why they may have more control than Amazon to navigate the evolving digital advertising landscape in the coming years.

One interesting tidbit from the call was that Amazon mentioned Prime Video is now a “profitable business in its own right”. For context, Amazon spent 22.4 Billion in video and music content spending in 2025, supermajority of which I think is related to video. Amazon reported $51.3 Billion LTM subscription revenue, majority of which is related to Prime subscription. If we assume $18-20 Billion content was spent on Video, Amazon is perhaps allocating ~40-50% of Prime subscription value to Video which, in addition to recent doubling of ad load on Prime Video, may have propelled Prime Video to be profitable.

Okay, enough about non-AWS business. Let’s get into AWS related discussion which will be behind the paywall.

Subscribers get the daily journal and five+ years of Deep Dives, i.e. full-length analyses with financial models on 65+ companies. The daily is just how I think out loud between the Deep Dives!