Meta 1Q'26: Nothing to Complain About

I know Meta’s stock is down after yesterday’s earnings, but I have a hard time complaining much as a shareholder. I will discuss why market may not share my enthusiasm later, but let me first share and explain why my own enthusiasm hasn’t abated post-earnings.

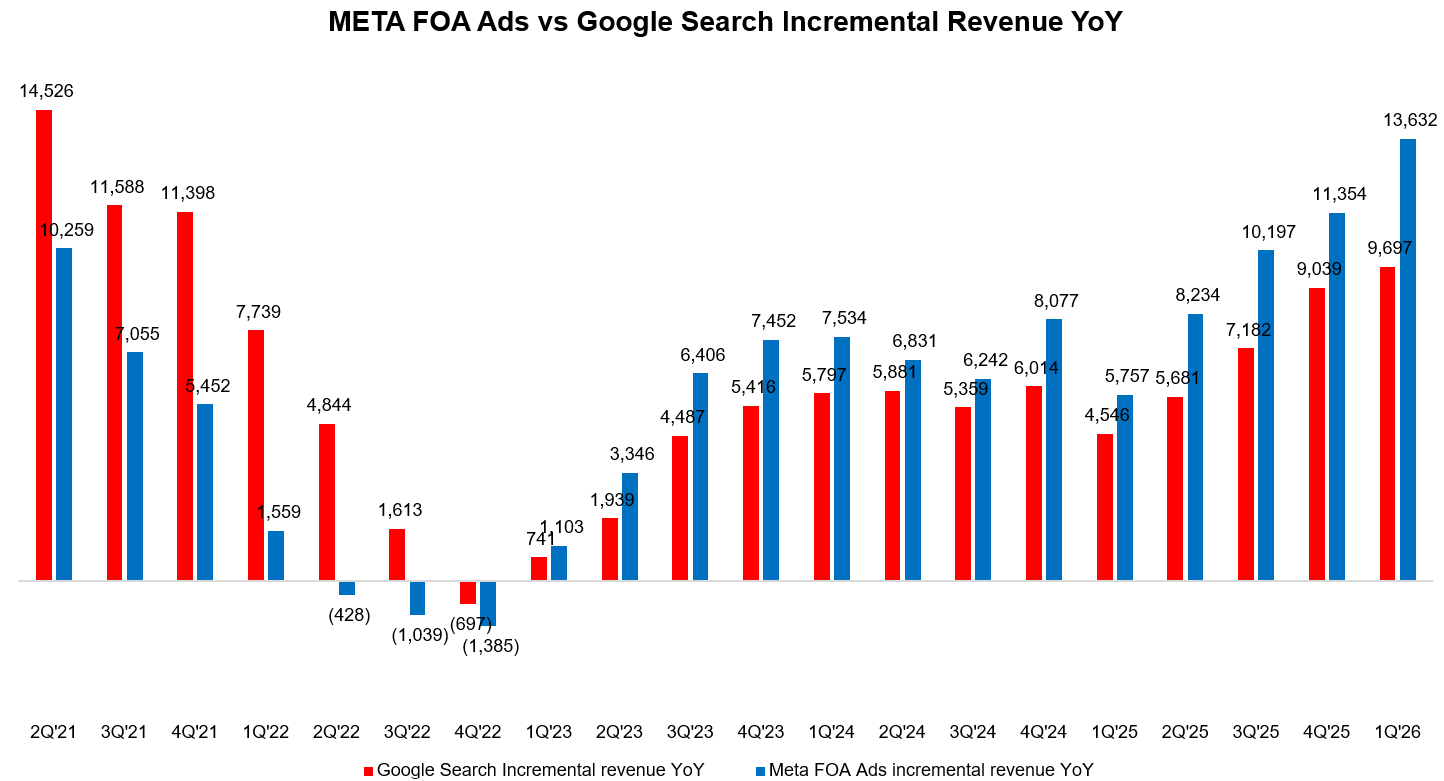

When I first saw yesterday that revenue from Google Search grew 19% YoY in 1Q’26, I thought that was downright incredible for a business of such scale. Then I looked at Meta’s numbers and updated my model.

Even such mindboggling search number paled in comparison with Meta’s Family of Apps (FOA) ad revenue growth. In 4Q’25, Meta’s ad revenue surpassed Google Search by ~$2.3 Billion. In 1Q’26, the gap increased to almost $4 Billion! Just to contextualize how fast Meta has been gaining share in digital advertising market, in 1Q’23, Google search LTM revenue was 42.2% higher than Meta’s FOA ads. Just three years later, Google search LTM revenue is now 11.6% larger; I won’t be surprised if Meta’s FOA actually becomes ~15-20% larger business than Google Search in five years. As Meta becomes better and better in AI-induced recommendations, it seems plausible that they can show you ads on their feed even before you decide to query it yourself on Google Search. As a result, the incremental share can continue to flow much more to Meta than Google search.

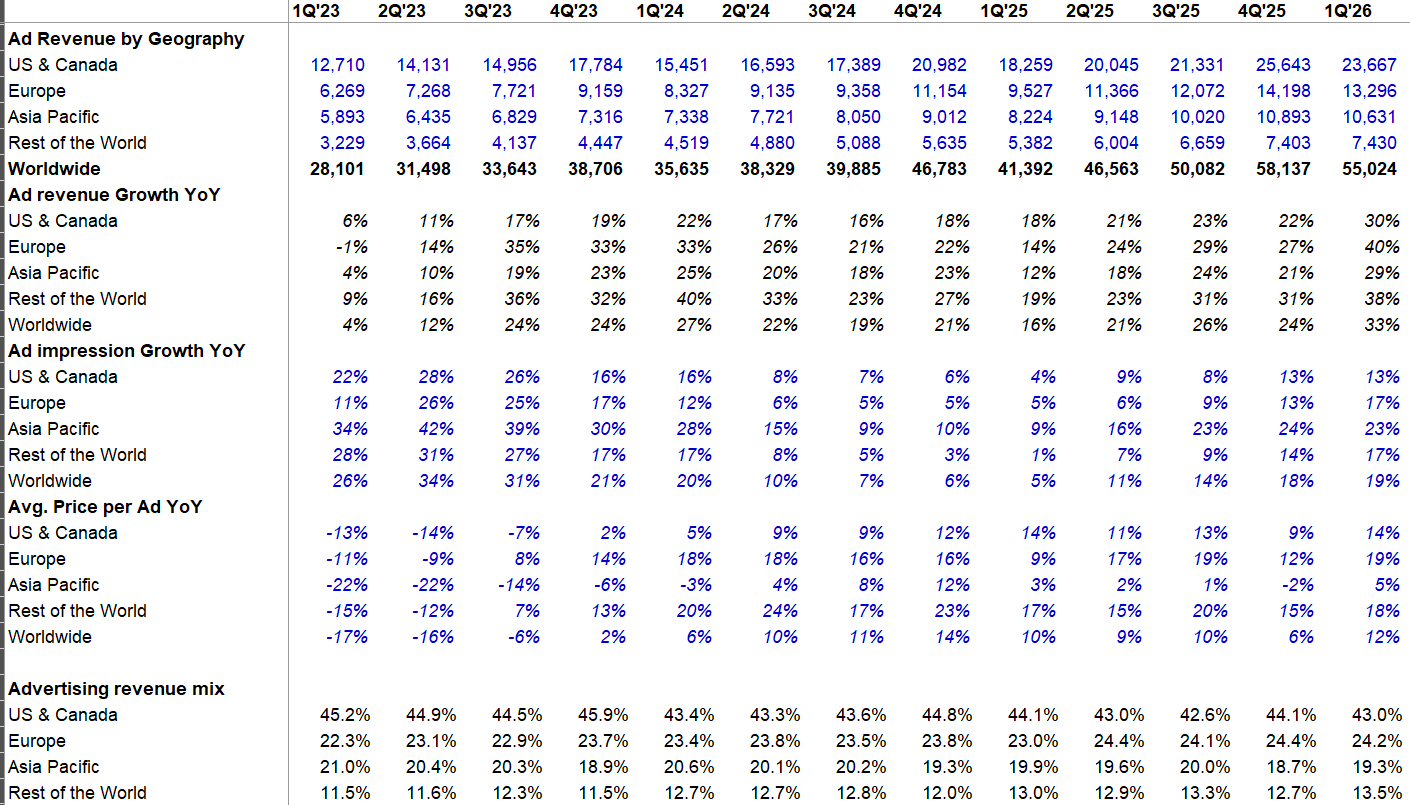

It is hard to realize looking at such numbers, but the war in Iran did have an impact on Meta. Internet outages in Iran and blocks in Russia led Meta’s Daily Active People (DAP) to decline QoQ. Meta also saw reduction in advertiser spend at the end of February which continued in March. While that understandably had a more pronounced impact in the Middle East, Meta mentioned in the follow up call that they also saw some softer trends in the US and Western Europe (they did mention the trends are improving a bit now, but their outlook embeds a range of scenario). The fact that Meta’s ad revenue grew in the US by 30% and in Western Europe by 40% (!!) DESPITE such softer trends in almost one-third of the quarter speaks volume of all the other tailwinds the company is currently enjoying.

Worldwide ad impression grew by 19% and average ad prices increased by 12%. There is a lot of concern among some investors that Meta may be intentionally juicing impression to show higher growth. I do not share this concern. Meta has explained again that larger driver of the impression growth is coming from users and engagement, not higher load. Ad loads did increase overall, but Meta has made it clear that they’re investing in the infrastructure to figure out users who don’t mind seeing ads and show materially fewer ads if you do. So the fact that ad load has increased on an average is not necessarily an indication that Meta is deliberately doing it to juice revenue growth, rather it is the mere byproduct of the fact that the ads are so good and relevant that most people not only do not mind seeing more ads and some of them may even enjoy seeing them.

Some of the tidbits Meta shared during the call which explains much more why impression growth has been increasing so fast (emphasis mine):

On Instagram, the ranking improvements that we made in Q1 drove a 10% lift in Reels time spent. On Facebook, total video time increased more than 8% globally in Q1, the largest quarter-over-quarter gain in 4 years.

Within the U.S. and Canada, ranking improvements we made drove a 9% increase in video watch time on Facebook in Q1. These gains are benefiting from advances we’re making across the full stack. Starting with data, we doubled the length of user interaction sequences we use for training on Instagram in Q1 and increase the richness of how each user interaction is described, enabling our systems to develop a deeper understanding of user interests.

Within our models, we’ve significantly increased the speed with which our ranking models index new posts, which is enabling us to recommend them sooner after they are published. We’re also applying more advanced content understanding techniques, which is enabling us to quickly identify posts that may be interesting to someone even if they haven’t engaged with a lot of similar content. These and other improvements have enabled us to increase the diversity and recency of recommended content with same-day posts now representing more than 30% of recommended reels on both Instagram and Facebook more than double the levels 1 year ago.

We’re also using AI to unlock more inventory by auto translating and dubbing videos into a viewer’s local language, enabling us to recommend a more diverse set of content. Over 0.5 billion users on each of Facebook and Instagram are now watching AI translated videos weekly.

In Q1, enhancements we made to Lattice’s modeling and learning techniques, along with advances in our GEM model architecture, drove a more than 6% increase in conversion rate for landing page view ads…In the second half of last year, we began rolling out our new adaptive ranking model, which is an LLM scale adds recommender model that we use for inference. This model improves our inference ROI by routing requests to more compute-intensive inference models when it determines there is a higher probability of conversion. (MBI Note: I have covered this more extensively here)

In Q1, we expanded coverage of our adaptive ranking model to support off-site conversions, which drove a 1.6% increase in conversion rates across the major surfaces on Facebook and Instagram.

Usage of our ad creative tools is also scaling with more than 8 million advertisers using at least one of our Gen AI ad creative tools and particularly strong adoption among small- and medium-sized advertisers. These tools are benefiting performance as well with advertisers using our video generation feature seeing more than 3% higher conversion rates in tests. (MBI Note: this was only 4 million in 2024, so number of advertisers using Meta’s Gen AI ad creative tools doubled in just 15 months. Meta mentioned most of them are SMBs who probably didn’t have any video ad budget before)

We also continue to invest in the value optimization suite, which helps advertisers maximize their return on ad spend by prioritizing the highest value conversions rather than optimizing solely for the most conversions at the lowest cost. Adoption by businesses has been strong following performance improvements we’ve made over the past year with the annual revenue run rate of our value optimization suite now over $20 billion, more than doubling year-over-year.

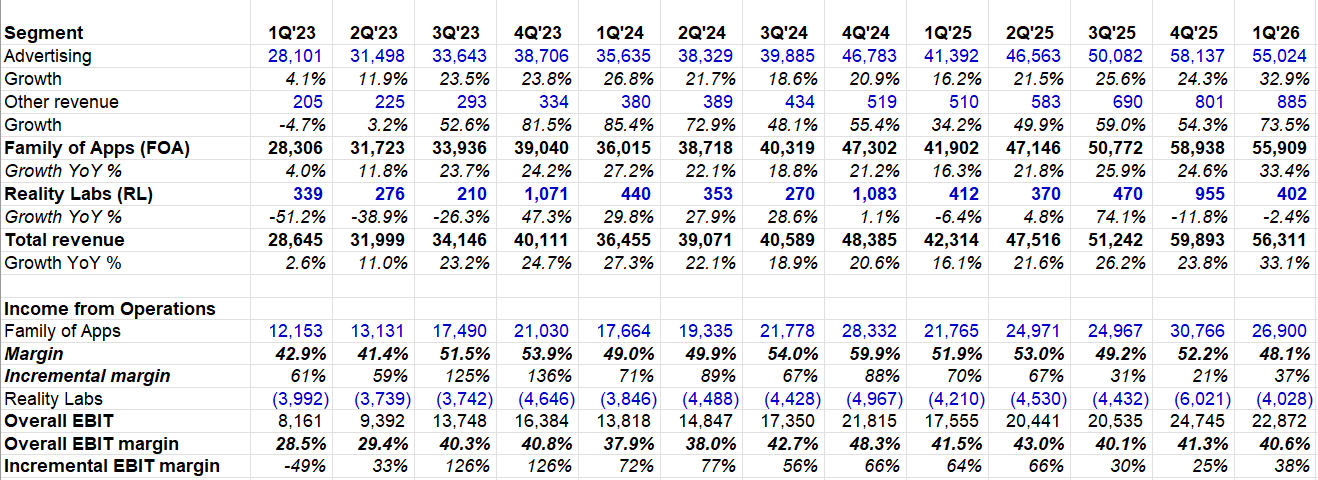

Drilling further into Meta’s segments, everything outside ads is obviously negligible. But I do want to highlight “other revenue” which was growing ~50%+ YoY in recent quarters. In 1Q’26, other revenue growth accelerated to ~74%! It won’t surprise me if “other revenue” continues to compound at more than 50% for the next five years! Meta’s messaging apps are still not quite as well monetized as their other properties are, so with AI, I think they are still in the early stage of ramp up in monetization there. Notice the following commentary from Meta (emphasis mine):

“…there are over 10 million weekly conversations between people and business AIs on our messaging platforms. That's up from 1 million at the start of the year, and we're going to continue expanding globally in Q2. And business AIs today are currently free for most businesses on our messaging apps. But as we make more progress, we expect that we will also work towards establishing a longer-term monetization model.”

It is also good to see that Reality Labs losses has gone down YoY. In fact, Zuckerberg mentioned even though they remain the largest investor in VR space, they would like their VR segment within Reality Labs to be “sustainable”. They will still incur losses due to investments in AI glasses, but I think the losses in Reality Labs may have already peaked in 2026 and it will go down over time from here.

Superintelligence

While Muse Spark did pretty well in benchmark, the more reassuring confirmation of Muse Spark came from engagement gains Meta saw due to the model. From the call:

In tests we ran leading up to the launch, we saw meaningful engagement gains that accelerated week-over-week with each new iteration of the model. We’re seeing similar games within Meta AI following the broad rollout of our new model with double-digit percent increases in Meta AI sessions per user.

…before this, we have been prototyping a bunch of things using other different models, whether it was our previous older models or kind of using the APIs from other companies. And now we’re unlocked to be able to go build things and get them to scale on top of our own models.

Agents are the new buzz word in AI, but Zuckerberg mentioned that he is yet to see agents that are suitable for mass consumer use as he mentioned “there aren’t that many that I would want to give to my mother”. I think that’s a good framing for a consumer internet company such as Meta. I am optimistic about their recent acquisition of Dreamer which was also more focused on solving agents for consumer use cases. One of the key points that I think Zuckerberg wanted to land in yesterday’s call is that thanks to AI, Meta’s scope is materially increasing. See his comments below (emphasis mine):

Right now, our apps primarily help people accomplish 3 important goals: connecting with people, learning about the world and entertainment. But we’ve always wanted our apps to understand more of people’s goals so we can help improve their lives in all the ways that they want. These new AI models will let us understand this in more detail. So instead of just looking at statistical patterns of what types of people engage with what content, for the first time in Meta’s history, we’re going to be able to develop a first principles understanding of what you care about and what each piece of content in our system is about -- is that way we can show you more useful things for what you’re trying to accomplish. And we’ll also be able to create personalized content specifically for people to help you achieve your goals as well.

Zuckerberg again highlighted how AI is boosting productivity of some employees as one or two people today can build something that previously took dozens of people months. As I have mentioned earlier, many tech companies may be forced to layoff the bottom decile or quintile to make room for token budget for the top decile.

Many Meta shareholders seem to think Meta doesn’t need to have a SOTA model. Zuckerberg seems to have a different opinion on this. While I do think Zuckerberg cannot acknowledge that they don’t necessarily need SOTA model for their core business to thrive since that would hurt his recruiting pitch to marquee AI researchers, I do suspect he genuinely believes that Meta needs SOTA AI model. Notice his comments below (emphasis mine):

“…you’re not going to have leading models in the future if your models can’t improve themselves, right? So you’re getting to a point where today, the models are still able to learn from people -- and then I think at some point, the models will have to improve themselves. And that’s how the growth is going to -- an improvement in the models is going to happen. And if you don’t -- if we don’t have an ability to do that, then we or anyone else, I think the companies that don’t do that are not going to be leading labs, then they’re not going to produce leading products. So I think at that like that is a table stakes thing that we are focused on.

Now does that make us a developer tools company? Not necessarily. I mean, I’m not against having an API or coding tools or anything like that. But it’s not our primary focus. But I actually think people conflate coding with self-improvement more than they should. Coding is one ingredient for the model self improving. It’s not the only thing. And we are focused on all of the parts that are going to be necessary for self-improvement in service of the personal super intelligence vision that we have for people and businesses.

So which way do I lean more? The investors who think Meta doesn’t need SOTA to thrive are likely right for the next year or two, but I suspect Zuck is indeed more right over the next 5-10 years timeframe. A self-improving model will be too useful to not have in-house in 5 years and any company who doesn’t have such model may face a high likelihood in NOT being labeled “big tech” in 10 years. As a long-term shareholder of Meta, I concur with Zuckerberg’s approach here even though success is far from guaranteed in getting AND staying at the frontier.

Investors also probably didn’t like the fact that Meta raised capex guide for 2026 from $115 Bn-$135 Bn range to $125 Bn-$145 Bn. However, this increase was primarily due to higher memory prices. Meta has also been building up their capacity through 3P cloud and I thought a particular comment from CFO is worth highlighting here (emphasis mine):

we’re going to continue building out our infrastructure with flexibility in mind. And if we end up not needing as much as we anticipate, we can choose to bring it online more slowly or reduce our spending in future years as we grow into the capacity that we’re building now.

That’s a pretty good position to be in. As long as compute constrained environment continues, Meta will utilize 3P cloud more. But once that’s not the case anymore, they can either lower future capex or utilize less 3P cloud or some combination of both. I suspect they may be contractually bound to use 3P clouds for the next 5-7 years in which case they can lower their own capex if it appears that they have overestimated their compute need.

Meta also highlighted their resilient chip strategy which I have covered before.

Nonetheless, investors seem to have elevated concern for Meta’s capex vs any other hyperscalers at the moment. I will explain the investors’ concerns and what I think behind the paywall.

Subscribers get the daily journal and five+ years of Deep Dives, i.e. full-length analyses with financial models on 65+ companies. The daily is just how I think out loud between the Deep Dives!