Alphabet 1Q'26: Stratospheric Heights in Performance and Expectations

Alphabet’s revenue growth has accelerated for five consecutive quarters. Except for Google Network business which is increasingly irrelevant, every part of the Alphabet business is humming right now.

As mentioned yesterday, despite growing at an incredible ~19% in 1Q’26, Google Search still continued to lose share in digital advertising industry.

While YouTube ads revenue growth appears quite uninspiring in light of Meta and Google Search performance, management highlighted that YouTube subscription is growing faster than YouTube ads which makes me think the overall health of YouTube business remains in good shape. In fact, I actually wonder whether the fact that more and more YouTube users are choosing subscription over ad-supported experience itself is creating some pressure on Meta’s (and TikTok’s) ad auctions (which would increase ad prices) since a lot of valuable impressions are simply going beyond the reach of advertisers on YouTube.

The standout segment from 1Q’26 was, of course, Google Cloud. More on Cloud later.

There also appears to be no end in sight when it comes to margin expansion. Google Services operating margin reached a new peak at 45.3%. Given that incremental margins continue to be 60%+, I wouldn’t be surprised if margin continues to expand here. Google Cloud’s operating income tripled YoY; as a result, a business that was unprofitable as recent as 4Q’22 posted 32.9% operating margin in 1Q’26.

In both these segments, I should highlight that there is a slight wrinkle in comparing current segment margins to historical segment margins. In 2Q’24, Alphabet disclosed that “AI model development teams previously under Google Research in our Google Services segment are included as part of Google DeepMind, reported within Alphabet-level activities, prospectively beginning in the second quarter of 2024”.

As you can see below, there has been a noticeable step up in “Corporate costs” which includes the “Alphabet-level activities”. In any case, the consolidated EBIT margin, which incorporates all the costs, reached the highest ever in Alphabet’s history. Given that its consolidated incremental EBIT margin was still 10 percentage point higher than reported overall operating margin, you can see why margins may continue to expand in the near term.

Let me quickly go through the key segments of Alphabet.

Search

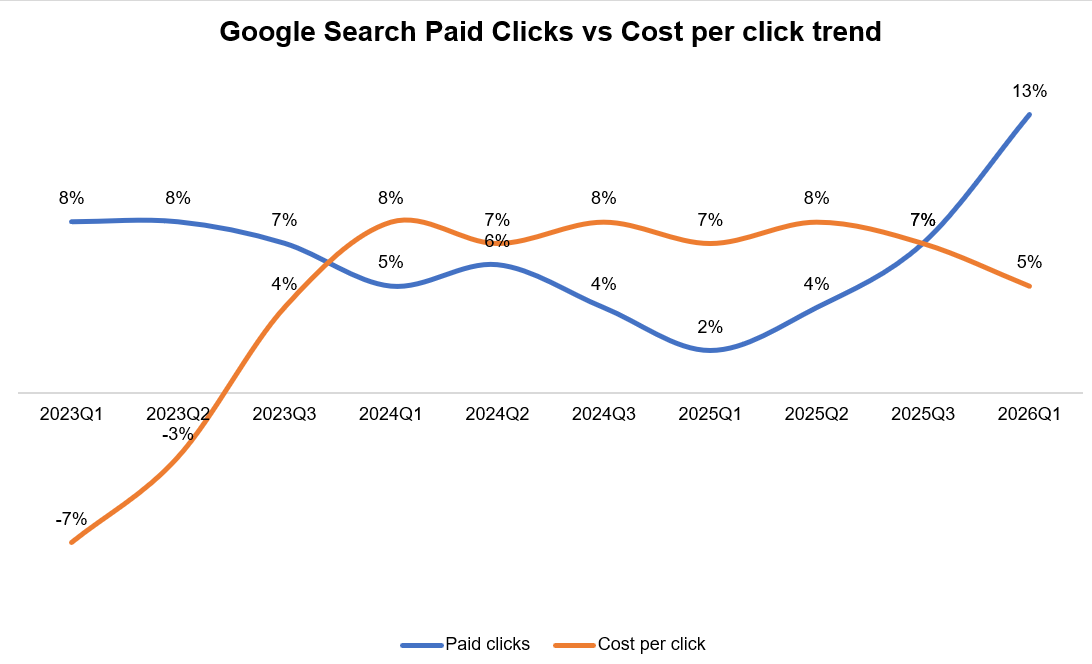

Paid Clicks grew at 13% in 1Q’26, which was the highest since 1Q’22. Google has dismantled so many bear cases (including the ones I worried about) that I have lost count at this point. While the dominant narrative has been that clicks may be under secular pressure due to the rise of zero click answers especially from chat bots, the data does not seem to support at least for paid clicks. In fact, looking at the pricing trajectory for cost per click and some of the commentary during the call, it seems highly likely that cost per click will grow at a healthy rate in the near term. From the call (emphasis mine):

“…more than 30% of our customer search spend now uses AI-enabled campaigns, AI Max or Performance Max. And these advertisers are seeing more conversion for the same spend.”

Management reiterated that AI is driving more search queries and given the nature of queries has been changing in the post-ChatGPT era, Google has found the changing nature of query to be a tailwind for their business. From the call (emphasis mine):

AI is boosting our ability to deeply understand user intent for a given search query and to find the most relevant ad. Even when we don’t have a direct user query, we’re making significant strides in improving relevance.

In Maps, we’re using Gemini to ensure promoted pins are deeply relevant to user surroundings, location of interest, history and intent. This work is improving ads relevance by nearly 10%, leading to significant increase in user engagement. We’re pairing this strengthened prediction-driven relevance with bottom-of-funnel precision.

While another concern was AI will raise the cost per query, looking at the margins you can tell such concerns haven’t quite panned out. Thanks to Google’s “hardware and engineering breakthroughs”, management mentioned they reduced search latency by more than 35% over the last five years and since upgrading AI Overviews and AI Mode to Gemini 3, they have reduced the cost of core AI responses by more than 30%.

Management was asked about whether they will launch ads on Gemini. They didn’t rule it out but also mentioned “we’re not rushing anything here”. I will be a bit surprised if Google launches ads on Gemini in 2026 as I believe they may want to stay focused on keeping the pressure high on ChatGPT by offering a zero-ads experience for free users.

YouTube and Subscriptions

Here’s how Alphabet’s total number of paid subscribers has grown since 1Q’25:

1Q’25: 270 Mn

3Q’25: 300 Mn

4Q’25: 325 Mn

1Q’26: 350 Mn

The recent growth was primarily driven by YouTube and Google One which itself was benefited by Google’s AI subscription plans.

One interesting data point was that management mentioned “YouTube Music and Premium offering saw its largest quarterly increase in the total number of non-trial subscribers, both globally and in the U.S. since YouTube Premium launched in June 2018.” That’s bit of a negative read-through for Spotify which only added 3 million Premium subscribers in 1Q’26 (vs 5 million in 1Q’25). That makes me think Spotify has lost share in the recent quarter.

I will talk about Google Cloud and some interesting read-throughs from the call behind the paywall.

Subscribers get the daily journal and five+ years of Deep Dives, i.e. full-length analyses with financial models on 65+ companies. The daily is just how I think out loud between the Deep Dives!