Defending the Enterprise Castle from the Model Layer

If Microsoft’s lagging stock performance didn’t already cause a tinge of nervousness among its shareholders, Satya Nadella has been writing several pieces on X almost to clarify why Microsoft may be in a spot of bother in a world where model layer eventually becomes utterly dominant in capturing value. A month ago, Nadella elaborated why “A frontier without an ecosystem is not stable”, and then yesterday, he penned another think piece titled “The Reverse Information Paradox”. Just a couple of weeks ago, Alex Karp from Palantir had some feisty takes on frontier models. If it’s not abundantly clear by now, enterprise software CEOs are probably talking to each other and they would all like to defend their castles from the dramatic encroachment of the model layer, namely OpenAI and Anthropic.

Nadella's prescription is for enterprises to build a hard trust boundary around their own learning loop: create private evals, retain ownership of memory and traces, train and tune inside the tenant boundary, and most consequentially, decouple the orchestration layer from any single model, so that if a given "generalist" model is taken away tomorrow, the firm's accumulated "veteran" capability stays home. He is particularly explicit about the asymmetry that perhaps almost offends him. From Nadella’s piece yesterday (emphasis mine):

“While the great innovation that comes from model providers having fair use rights to train models on public data is needed, I find it ironic that the status quo is to then turn around and impose restrictive terms on distillation, and to reserve the right to learn from customer usage and interaction data. If learning flows in only one direction, economic value converges toward the owners of the learning infrastructure rather than the creators of the knowledge itself. Therefore, it’s imperative that we distribute the learning infrastructure to every firm so that they can control their own learning loop.”

Of course, Microsoft is OpenAI's largest outside partner and operates one of the largest AI infrastructure businesses on earth. A world in which every enterprise treats frontier models as swappable commodities behind a model-agnostic orchestration layer is a world in which pricing power drains out of the model layer and pools in the layers Microsoft happens to sell i.e. the infrastructure underneath and the trust boundary around it. Commoditize your complement is one of the oldest playbooks in tech, and while you can legitimately argue Nadella is obviously talking his book, that alone is not quite sufficient to invalidate his arguments. If I were running a large enterprise company, I would certainly find Nadella’s advice closer to my interest and although OpenAI and Anthropic’s products would make my employees more productive today, I would worry a lot more about the future of my IP given the not-so-restrictive data retention policy (for safety reasons, of course) of these AI labs. What I’m still not sure about is whether large enterprises are well equipped to pay heed to Nadella’s suggestions or the force of the current is too high to turn against it now.

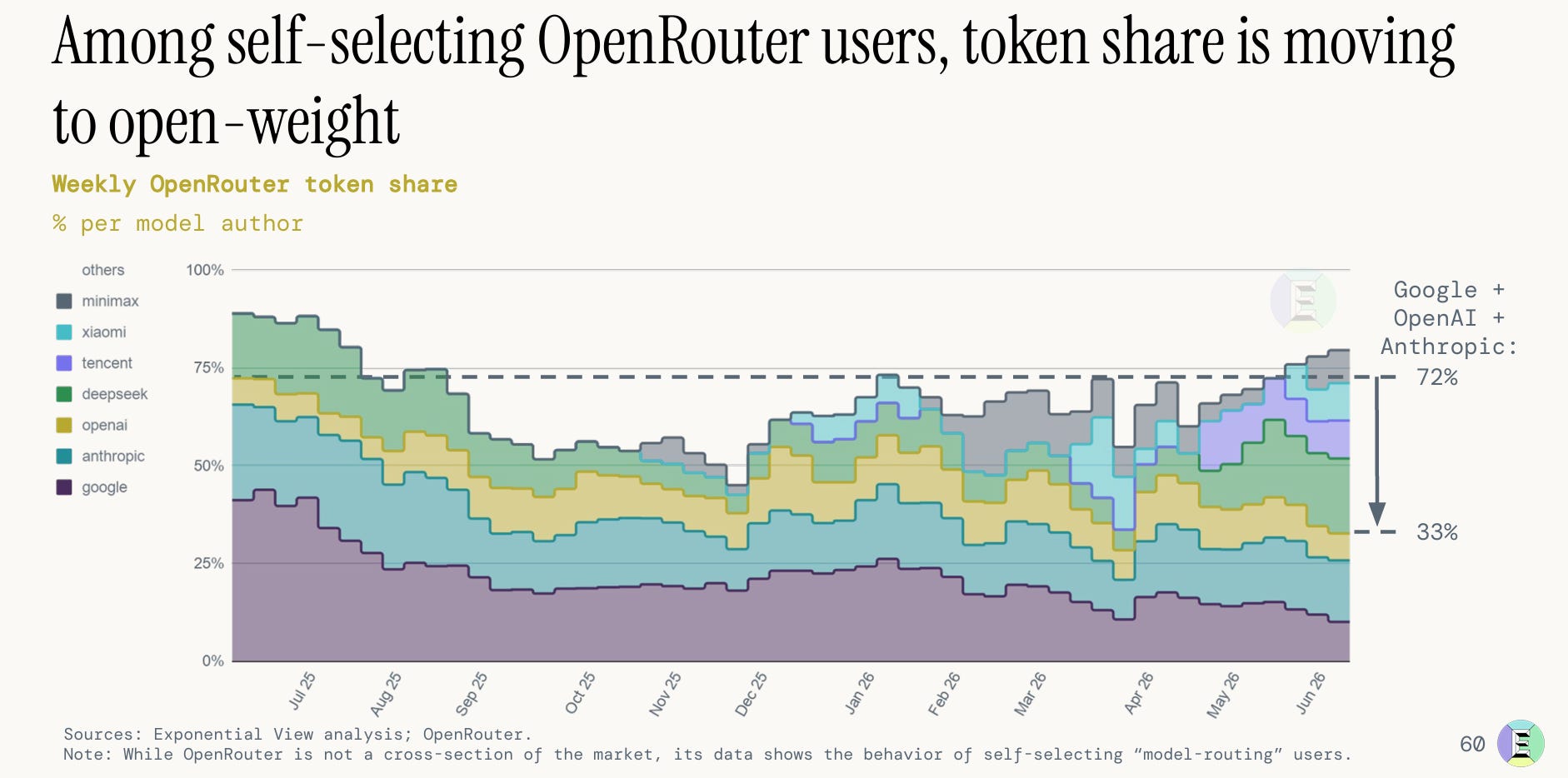

There are indeed indications that companies are trying to resist the temptation of giving into the comfort of just using the frontier models. Last month, Exponential View had a good presentation in summarizing the state of AI market. Their analysis of OpenRouter token data shows Google, OpenAI, and Anthropic falling from 72% of weekly token share a year ago to about 33% today, with the difference absorbed almost entirely by open-weight models. However, since OpenRouter users are self-selecting model-routers and almost certainly not representative of the broader market share in token. Nonetheless, it is likely to be a leading indicator of the most price-elastic workloads. It definitely reveals that if the broader enterprise market gradually start caring deeply about their costs, the token market can potentially bifurcate materially away from the expensive frontier models.

Gavin Baker also alluded yesterday where this leads if it keeps going. The “mega bull case” for AI infrastructure, he argues, is precisely this migration:

The mega bull case for AI infrastructure would be *if* market share shifted away from certain frontier labs with 90%+ inference margins toward cheaper models, whether open-source or closed.

It would increase the ROI on AI spend for end customers by increasing intelligence per dollar, which would drive incremental token demand. Margin dollars would effectively get redistributed from the frontier labs to AI infrastructure providers. The infra winners would be those with the lowest per token cost and the winners at the model layer would be those with the highest token efficiency.

There are many reasons Jensen is so focused on open source, but this is likely the most important one as I think he is probably less worried about a monopsony these days. Lower margin % at the model layer = more margin $ at the infra layer all else equal.

With SpaceX and Meta being vertically integrated and possessing the #3 and #4 models respectively it is more possible than ever. Note that Grok 4.5 is ahead of Fable for some useful tasks at a much lower cost, so ranking them #3 is conservative.

This is not happening yet. Cheap, mostly open source tokens are likely the majority of volume today but the majority of economic value is still accruing to the most intelligent models. Might change though.

We will see.

But Gavin’s caveat is the crux, and it is the same caveat I would attach to the OpenRouter chart: this is not happening yet in the entire token market. Of course, we are so early that just because it hasn’t happened yet doesn’t really tell anything how it may unfold in the future. Token share and dollar share today are almost certainly wildly different charts. The token market is bifurcating into a commodity lane and a premium lane, and how the workload distribution ultimately splits between them may decide where the value gets ultimately captured. I’m not sure anybody quite knows yet, including the labs.

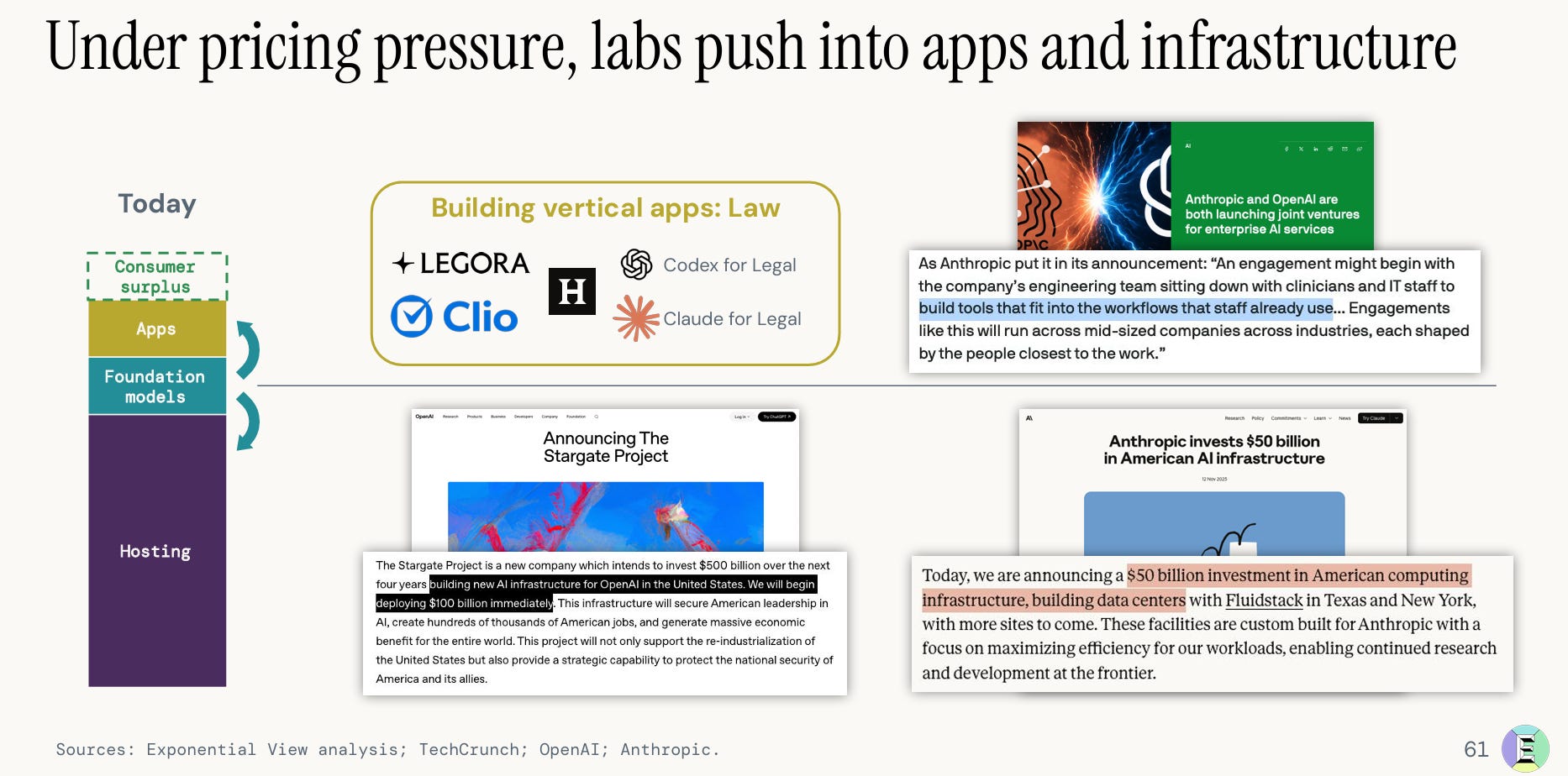

What can the labs do to respond to such pricing pressure? Labs are already pushing up the stack into applications: Claude for Legal and Codex for Legal now squeezing the Harveys, Legoras, and Clios of the world, while Anthropic and OpenAI have both launched enterprise services joint ventures that look basically like consulting, with engagements that begin with the lab’s engineers sitting down alongside a customer’s IT staff. Ultimately, it won’t surprise me at all if AI labs end up releasing plethora of first-party enterprise applications in the next 3-5 years to capture any market that has attractive revenue and profit pool for them to feast on. And they are also pushing down the stack into infrastructure. When your layer’s pricing power is in question, you will obviously integrate toward the adjacent margin pools.

As I hinted in my piece “Meta on the Offense”, don’t be surprised if the most frontier models cost an arm and a leg in not-so-distant future if the duration of the lead remains only a handful of months before other players catch up. In that world, it is quite rational for AI labs to serve your frontier model only to customers who can afford to pay through their nose because the value such customers can capture from frontier models justify the costs. Will that be sufficient to recoup the investment and train the next model? Like I said earlier, I’m afraid only time can perhaps answer that question. One of the reasons my own portfolio has become so concentrated is I am trying to avoid placing bets on anything that require me to answer this question with high level of confidence.

Subscribers get the daily journal and five+ years of Deep Dives, i.e. full-length analyses with financial models on 65+ companies. The daily is just how I think out loud between the Deep Dives!

Current Portfolio

Please note that these are NOT my recommendation to buy/sell these securities, but just disclosure from my end so that you can assess potential biases that I may have because of my own personal portfolio holdings. Always consider my write-up my personal investing journal and never forget my objectives, risk tolerance, and constraints may have no resemblance to yours.

My current portfolio is disclosed below: