ASML 1Q'26 Update

A new earnings season has arrived. If ASML’s earnings is any guide, be prepared to hear another quarter of “demand is outstripping supply” from all the players in the semi value chain.

ASML’s CEO Christophe Fouquet started his prepared remarks with the following which set the tone:

“…for the foreseeable future, demand will continue to outpace supply. This creates constraints across end markets from AI to mobile and PCs, which is driving our customers to aggressively add capacity.”

The last question on the call was about whether ASML may become the bottleneck for supply to get closer to demand. Fouquet does not think that is the case:

I know the question of bottleneck comes back very often. I think we don’t feel at all that we are the bottleneck today. We’re very closely working with our customer. And again, we have many, many, many tools in our hands to make sure we keep it this way.

During the call, ASML management explained how much they are expanding capacity to meet the growing demand (emphasis mine):

last year, we had 44 tools. if you are just looking at 80 tools, we say at least 80, but if you just look at 80 tools, those 80 tools give you double the wafer per hour capacity that we would have shipped in 2025. And on top of that, we’re helping customers upgrade their installed base…we’re really working hand in glove with the customers to look at what is your capacity need, what’s the easiest way and also the most economical way for you to get to the productivity that you need. And we’re executing on all fronts on availability, on productivity, on unit numbers, capacity and then upgrading the installed base.

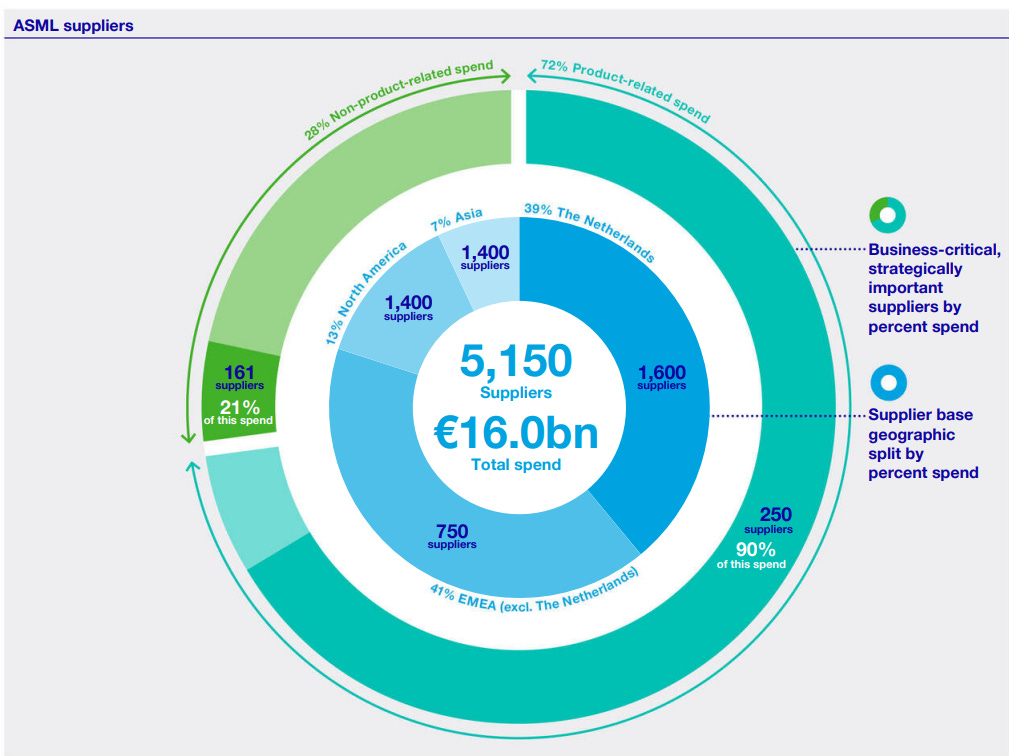

I find it quite remarkable how quickly ASML was able to expand the capacity despite having a maze like supply chain. For context, ASML had 5,150 suppliers in 2024; therefore, ramping up capacity means ASML needs most of these suppliers also step up their game simultaneously to meet ASML’s wish list.

It is, of course, not magic rather ASML’s own meticulous preparedness across their supply chain that helped their ability to expand the capacity in a relatively short time. From the call (emphasis mine):

“I think we have been mostly explaining in the last few years that we were preparing the supply chain basically to be able to go to a capability of 90 on Low NA and to a capability of 600 for deep UV, total deep UV. And I think what we see in these ramps is that a lot of the preparation is paying off. So I think that, of course, you always have challenge with the supply chain. But I will say, so far, our supply chain has been able to support our move rate increase quarter-by-quarter. And that includes, by the way, ZEISS to name them, that include the optic, where I think we had major challenges a few years ago in the previous ramps. I think we are in a much better shape there.”

It also helps that given Samsung and Intel’s ability to attract customers in light of the compute constrained environment as well as potential geopolitical risks for relying solely on TSMC over the long run, TSMC’s monopsony power over ASML is almost certainly not increasing. From the call:

“It’s pretty clear that the demand in the foundry business is huge and is outweighing the supply, right? So that leaves a bit of room for others than the market leader. And I think that’s room that the other players are trying to enter into. We all know about the plans of Samsung in Taylor. So that’s real. And of course, that also requires shipment for us, which is happening. The U.S. player in this business already has quite some capacity, I would say. So we’ve said it before that for this year, we’re not counting on a huge number of shipments in that regard because they already have quite a bit of capacity.

Then you ask about the longer term. Of course, the market that is characterized by multiple players at least will sort of guarantee innovation. And that, I think, is what is important. I think the market leader has been tremendously innovative. So you cannot say that even in the market that was dominated by one player, you would still see a lot of innovation. I think that’s what we’ve seen in the past couple of years. But having 3 players in there will probably guarantee even more innovation. And I ultimately think that, that is good for the ecosystem.”

If there are multiple players and one of them adopts high NA EUV which then yields better results than others who do not, you can see how a oligopoly instead of a monopoly in advanced logic chips can potentially increase the pace of high NA EUV adoption. If it remains just a TSMC monopoly, the pace of adoption of high NA EUV can be dictated by solely on TSMC’s wishes.

Of course, logic chips is only half of ASML’s system sales while the other half comes from memory companies. While listening to the call yesterday, I almost thought ASML management were pitching memory stocks! ASML has seen a major adoption of EUV among memory players and management made the case that the move from low NA to high NA EUV will also play out similarly over time as the customers see the performance and productivity benefits over time. From the call (emphasis mine):

I think DRAM has been a bit the perfect storm for ASML because, of course, we have this capacity buildup. But as we mentioned a few times, we have seen a major adoption of EUV in DRAM in 2025. And you may have noticed that our, I will say, U.S. DRAM customer also made this announcement that they were shifting also pretty strongly on EUV. And the reason for that is, of course, performance, but it’s also capacity because if you are going to use more EUV layers, you are going to need less multi-patterning and multi-patterning takes a lot of space also in the fab.

…Now of course, what’s true for Low NA today, I think we expect to be true for High NA in the future. So it’s, again, not prime time for High NA today. But I can only say that more Low NA EUV adoption today can only help for more High NA adoption in the future because the logic of High NA is the same. It’s going to single expose, simplifying the process, getting more space, et cetera, et cetera. So I think DRAM has been really a good story when it comes to litho intensity in ‘25. And I think it’s translating very strongly into EUV demand this year and most probably in the years to come.

One question investors often wonder whether ASML is leaving too much money on the table in a compute constrained environment by not sufficiently increasing prices. ASML management declined to take advantage of its customers for what could turn out to be a temporary phenomenon. From the call (emphasis mine):

“Now in our model of pricing, as you know, our model of pricing is not based on the squeeze that our customers find ourselves in. That’s not the way we do business. The way we do business is that we look at the value that we provide to our customers, generation on generation, tool on tool, and we take our fair share in that. And you might say in the current climate, can’t you squeeze out a little bit more? I understand that. But it’s also true that when the market is good, it goes down a little bit and the customers are going through more difficult times that it also pays these fees.

So fundamentally, we believe that the model that we have is a fair model. It’s also a model that is fair to all the players because I would find it difficult to explain why we’re charging more in, let’s say, the memory environment versus the logic environment. That’s just not the way we do business. So we’re very, very happy with the business model we have, which is based on the value of our tools, and we would gladly continue with that approach.”

Indeed, while ASML’s customers (TSMC and Micron, for example) have higher gross margins today than ASML, looking at more long-term gross margin trajectory clearly depicts ASML’s more steady gross margin while memory companies’ margin whipsaw from one extreme to another. Even if TSMC’s gross margins were more volatile than ASML’s over the last decade, it is true that TSMC’s gross margin was almost consistently higher than ASML, perhaps a reflection of their monopsony power over ASML.

ASML increased the revenue guidance from EUR 34-39 Billion to EUR 36-40 Billion for 2026. Even in late last year, analysts were expecting only EUR 33 Billion revenue for 2026 which has now increased ~20% over the last 6 months. Even though the stock has gone down a bit following the earnings, the stock is still +25% YTD. My broad takeaway from ASML call was that if you are looking to get a hint of capex peaking or demand-supply gap narrowing during any of the earnings call in semi value chain, you are unlikely to get it during this earnings season.

In addition to “Daily Dose” (yes, DAILY) like this, MBI Deep Dives publishes one Deep Dive on a publicly listed company every month. You can find all the 67 Deep Dives here.

Current Portfolio:

Please note that these are NOT my recommendation to buy/sell these securities, but just disclosure from my end so that you can assess potential biases that I may have because of my own personal portfolio holdings. Always consider my write-up my personal investing journal and never forget my objectives, risk tolerance, and constraints may have no resemblance to yours.

My current portfolio is disclosed below: