TSMC 1Q'26 Update

Yesterday’s TSMC earnings call was yet another confirmation that the AI momentum right now is one-way street: up and to the right! TSMC’s CEO C.C. Wei in his prepared remarks encapsulated the sentiment around AI (emphasis mine):

“AI-related demand continues to be extremely robust. The shift from generative AI and the query mode to agentic AI and command and action mode is leading to another step-up in the amount of tokens being consumed. This is driving the need for more and more computation, which supports the robust demand for leading-edge silicon. Our customers and customers’ customers, who are mainly the cloud service providers, continue to provide us with their very strong signal and positive outlook. Thus, our conviction in the multiyear AI megatrend remains high, and we believe the demand for semiconductors will continue to be very fundamental.”

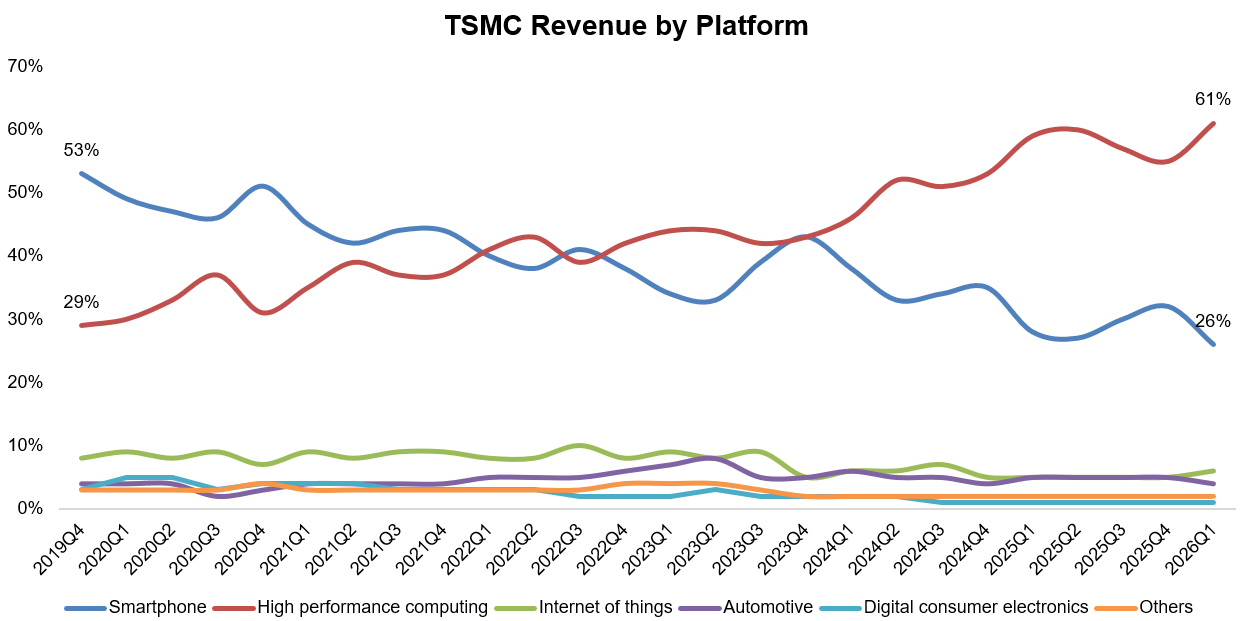

The transformation of AI can be more tangibly gauged just by looking at how the mix of High Performance Computing (HPC) in which AI Accelerators, Data Center GPUs and ASICs are embedded, and smartphone’s contribution to TSMC revenue evolved over the last five years. Back in 4Q’19, HPC was only 29% of TSMC’s revenue whereas 53% of their revenue came from smartphones. Today, their positions have completely flipped as HPC is now 61% of TSMC’s revenue vs Smartphones contributing only 26%.

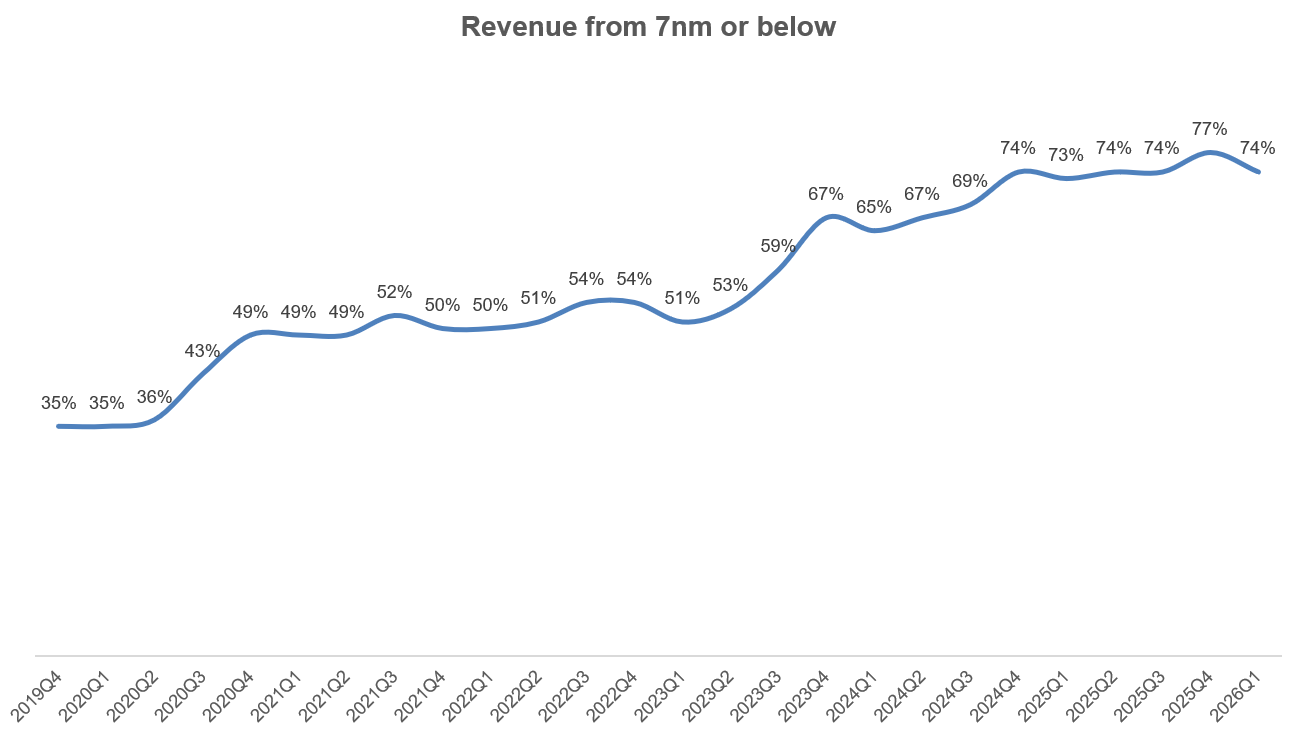

TSMC’s revenue from the most advanced nodes (7 nm or below), where they are a de-facto monopoly, is now almost three-quarter of their revenue.

TSMC was asked about potential competitive intensity rising for the advanced nodes, but management reminded everyone that there is no “short cuts” in this business. From the call (emphasis mine):

“…both Intel and Tesla, they are TSMC’s customers. But again, they are our competitors, and we view Intel as our formidable competitor and do not underestimate them. But having said that, there are no shortcuts. The fundamental rules of the foundry game never change. They need the technology leadership, manufacturing excellence and customer trust, and most of all, the service, which has been mentioned by Jensen; thank you for his wording.

Again, let me say that it takes 2 to 3 years to build a new fab, no shortcuts. And it takes another 1 to 2 years to ramp it up. Again, that’s the fundamental of foundry industry. And whether we try to win them back, actually, they are still our customer. And we are very confident in our technology position, and we work very hard to capture every piece of business possible.

It doesn’t sound like TSMC is losing much sleep over the competition. In fact, given the demand, TSMC confirmed that their capex will likely be closer to high end of capex range of $52-56 Billion provided last quarter. Moreover, management also mentioned they expect revenue growth to outpace capex growth.

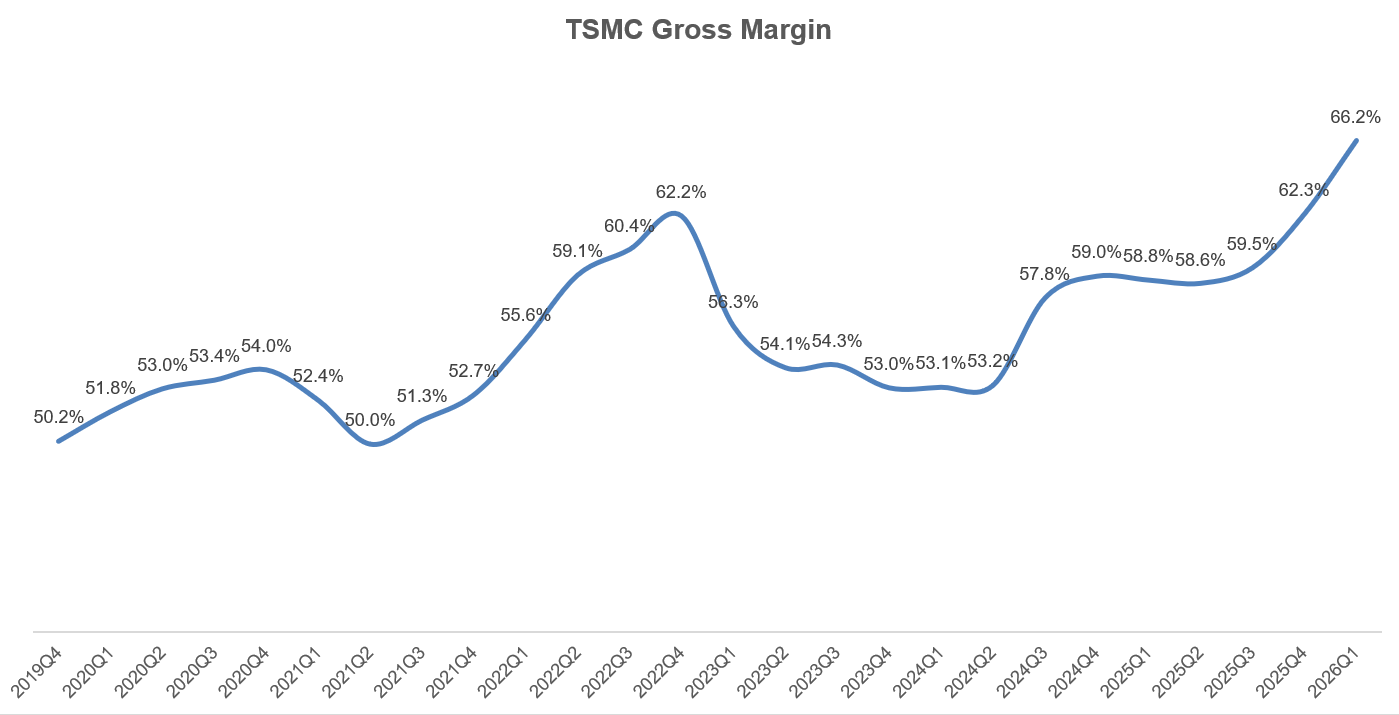

Gross Margin reached a new high: 66.2% in 1Q’26! Given the recent gross margin trends, analysts probed whether their through-the cycle gross margin guidance for long-term (2024-2029) of 56%+ is actually too low, but management was not ready to upgrade it further...yet!

Like ASML, TSMC management was also asked by analysts whether they are pricing appropriately given the compute constrained environment. This is what TSMC management said in response (emphasis mine):

Let me say that we always view our customers as our partners. Of course, we know our value; of course, we know our position, but we also view our partners as very important business partners, so that we don't change our pricing dramatically or something like that. We just try to make sure that our customers can be successful in their market. And at the same time, we grow together, and we also earn our value, so that we can continue to expand our capacity to support them. That fundamentally is, number one, our customer got to be successful. That's our consideration, number one, and we grow together. And again, there's a keyword please pay attention to. Customer is our partner.

Indeed, it makes a lot of sense to gradually take price over time if AI demand remains as insatiable as it is today. If TSMC maintains its monopoly in advanced chips in 5-10 years and AI demand continues to skyrocket unabated, the gross margin is very likely to be much higher than the mid-50s through the cycle.

It should be no surprising that TSMC revenue estimates continues to go higher. Nonetheless, it’s pretty incredible that revenue estimates for 2026 went up by ~25% since September last year! If the business fundamentals are improving so fast, it is less surprising that the stock too went up by ~60% during this period.

In addition to “Daily Dose” (yes, DAILY) like this, MBI Deep Dives publishes one Deep Dive on a publicly listed company every month. You can find all the 67 Deep Dives here.

Current Portfolio:

Please note that these are NOT my recommendation to buy/sell these securities, but just disclosure from my end so that you can assess potential biases that I may have because of my own personal portfolio holdings. Always consider my write-up my personal investing journal and never forget my objectives, risk tolerance, and constraints may have no resemblance to yours.

My current portfolio is disclosed below: