AI Economics in the East: Part 2

Yesterday, Flo Crivello tweeted something that caught my attention:

We've tested new OSS models the moment they're released for a while at Lindy. Inference is our #1 cost by a lot (more than payroll) — cutting it by 2-5x would be transformative.

Last year, OSS models were "not even close."

3 months ago, "almost there." Came close to making Kimi K2.5 our default.

I think we are right now crossing the line to "at the frontier, for most use cases." GLM-5.1 in particular is incredible and will likely be our default soon.

Surprised by this development — OSS caught up.

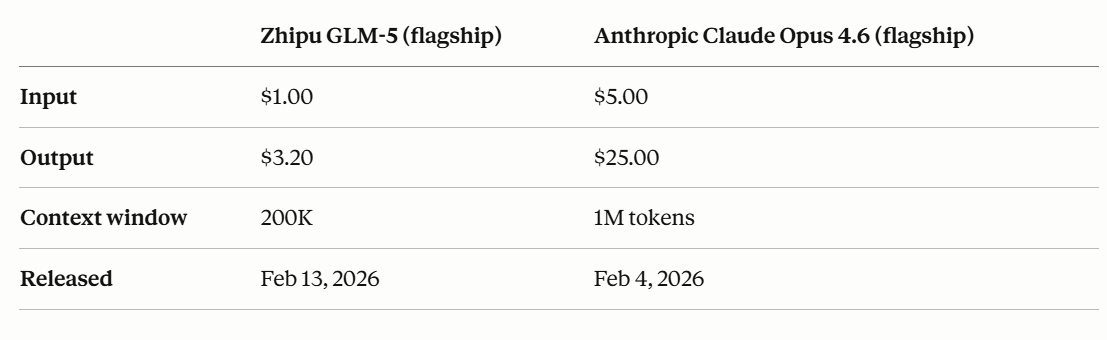

For context, here’s the head-to-head on Anthropic’s Claude Opus 4.6 and Zhipu’s GLM-5.1 flagship model API pricing (per million tokens):

Rohit Krishnan captured how strong open source models can change the economics in AI (emphasis mine):

“I think a most fundamental open question today is this - how much the open to closed source gap will continue to exist. If it does, and it's perpetual per model, we have a concentrated pharma like future for frontier labs. They have 6/13/18/24 months to squeeze the profits before it gets competed away.

The default amount of profit is not zero either, since not everyone can create a model. But it's not going to be 60% gross margin inference if Zhipu can compete for it.

Now, it's possible there are some things where the open-to-close gap is longer. Claude's personality maybe as an example. Not everyone will care, but some will! And for them this is the price vector that matters. So a consumer business here can probably continue to command due to brand and utility.

And if the frontier models truly hit a scale where OS can't reach, say $100B training runs, then they can have more enduring advantage. Revenues can grow, expenses can become more about maintenance and sustainability, and usage changes. You'd use the best possible model to do the thing you want to, or to explore, and for anything that's settled, a workflow, you'd get that done for much cheaper with the lowest cost model possible.

Which means the distribution of future profits are either highly crunched (few years to squeeze) or long tail (for exploration and super smart work). It'd be interesting to see how this plays out, and what it means for how to price the OpenAI/ Anthropic IPO.”

The more I think about it, the less likely it appears that the most advanced models will be available via API in the long-term (see yesterday’s piece for more on this). Given this context, if a company’s product directly competes against frontier model developers’ first-party products in which using the most advanced models would lead to differentiated product experience, multiple for those companies’ earnings should be under pressure.

Considering how the Chinese models remain deeply relevant in the question of long-term economics of AI over the world, I am going to follow closely the two publicly listed AI labs in the East. I have already covered Zhipu a couple of days ago, and today I will discuss MiniMax which also IPO-ed early this year. The stock has nearly tripled since its IPO and is currently worth ~$40 Billion Enterprise Value (EV). Like Zhipu, the stock is richly valued as it trades at ~180x NTM revenue. I will discuss more about their economics behind the paywall.

In addition to “Daily Dose” (yes, DAILY) like this, MBI Deep Dives publishes one Deep Dive on a publicly listed company every month. You can find all the 67 Deep Dives here.