Airbnb's Incentives

On X, I often come across some version of a stock performance chart showing how Airbnb has performed since its IPO which has been largely flat for more than five years now! It looks particularly unflattering when you compare and contrast to its closest peer: Booking Holdings.

Generally speaking, these comparisons lead to a barrage of pile on from people complaining about cleaning fees, or pointing out how the originator of “founder mode” has ironically flailing around to drive his own company forward. It appears Chesky himself is acutely aware of this dynamic as he felt the need to respond to one such tweet a couple of days ago.

Our stock price went up 5x in the run up to the IPO. This is not an excuse for the last 5 years, but we’ve rebuilt the company from the ground up in that time, and we anticipate better times ahead. The story isn’t over.

— Brian Chesky (@bchesky) June 15, 2026

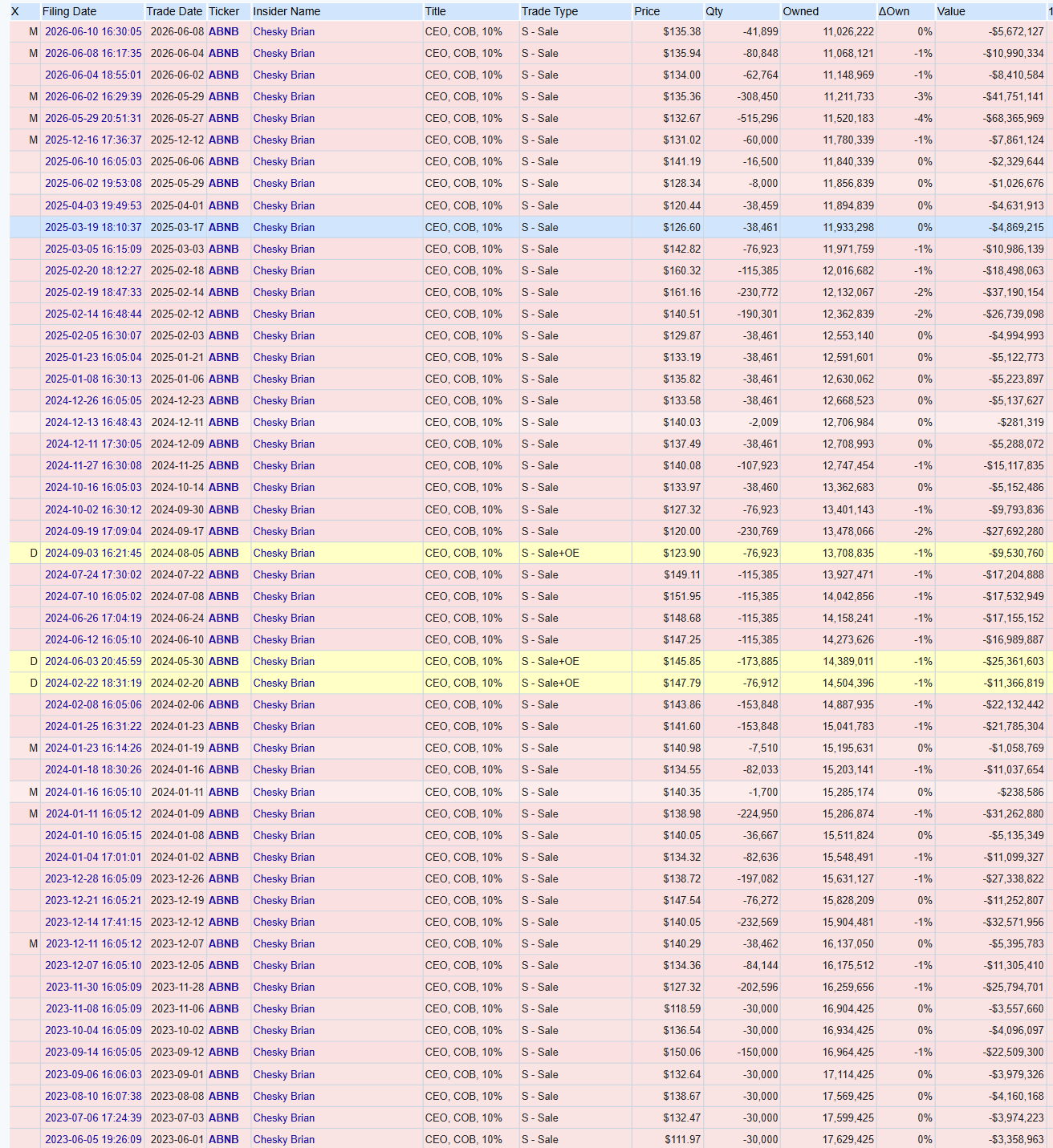

Perhaps one interpretation of Chesky’s tweet is that Airbnb timed the IPO almost perfectly to raise money from the market. However, many were quick to point out that despite Chesky’s message of optimism about Airbnb’s future, he has never ever purchased a single share in the open market and been consistently selling shares since the IPO. If anything, his pace of selling has increased as he sold ~$135 million Airbnb stock in just last three weeks which is more than what he sold in all of 2025. Maybe he’s busy selling Airbnb stocks for funding a new AI company. In any case, such data points may not inspire a lot of confidence for current and prospective shareholders of Airbnb.

While these data points can look far from ideal in isolation, it doesn’t quite give you the full picture. I actually think Airbnb has one of the better CEO incentives I have come across while covering 65+ companies over the last six years.

One of the reasons Chesky is a repeat seller of the stock is that he receives $1 salary and zero cash bonus from Airbnb. Even though Mark Zuckerberg also receives $1 salary from Meta, the expenses related to cover his personal security lead to cost the company ~$25 million per year. Chesky’s personal security related costs are far more banal and his total compensation from Airbnb was below $300k in each of the last three years.

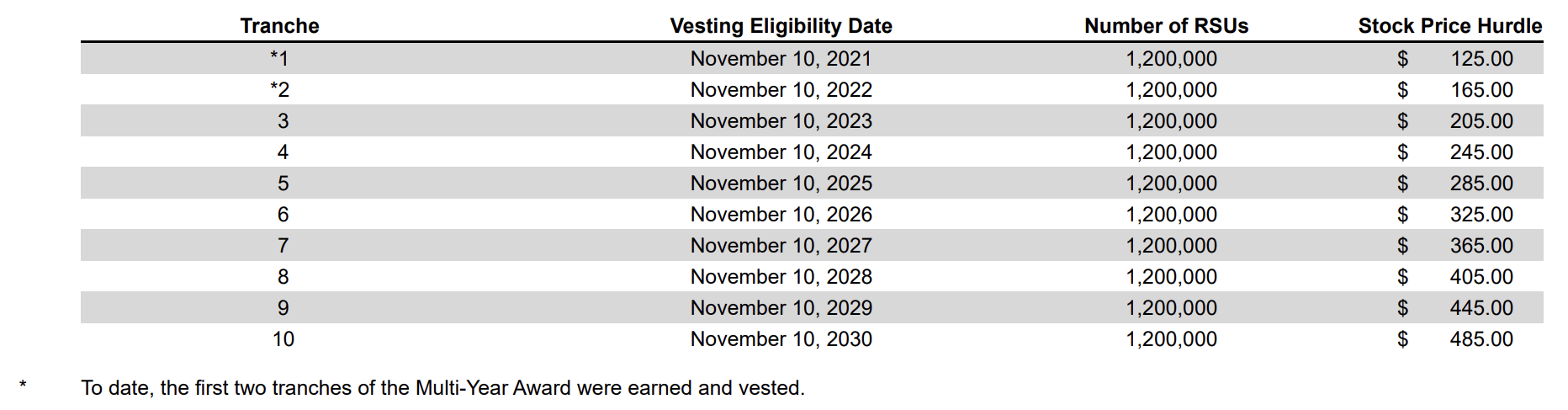

More importantly, Chesky was given a highly ambitious RSU program exactly one month before the IPO which would only fully vest if the stock price became 7x the IPO price. The award was designed in 10 different tranches, and so far only two of the ten tranches have been vested. To the board’s credit, not only did they not revise the ambitious targets down once meeting the stock price targets appears to be increasingly less likely (unfortunately a far more common practice), they also did not award any new options/RSU program for Chesky since the 2020 program. Let me put it this way, if Airbnb stock is at $204 in November 2030 (slightly less than 10% CAGR from today) and Chesky remains CEO of Airbnb then, he will be one of the lowest paying executives in the S&P 500 over the 10-year period. Of course, these RSUs are hardly his primary incentives since he still owns ~$9.3 Billion worth of Airbnb shares. Chesky doesn’t really need any extra incentives for him to want the stock price to go up since he is still the largest shareholder of the company.

Perhaps a more relevant question is how Airbnb’s other Named Executive Officers (NEO) are compensated. When I did my Airbnb Deep Dive back in October 2022, I was slightly put off by the plethora of qualitative metrics to determine management’s annual incentives.

This is what I wrote back then about the annual incentive structure for the rest of the management:

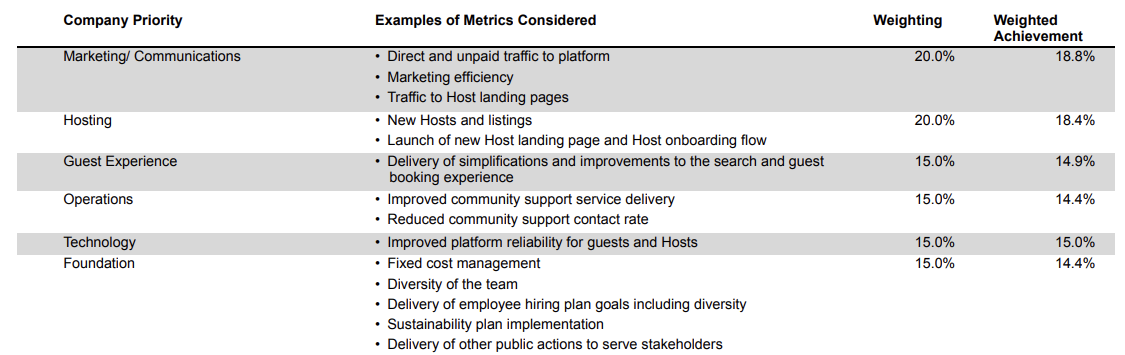

“While the metrics the board look at are revelatory to Airbnb's priorities such as direct and unpaid traffic to platform, new hosts and listings etc, there are also quite a few elements in the incentive structure that appears to be subjective in nature. For example, in the "technology" category, the board looks at "improved platform reliability for guests and hosts" in which the management received 15 out of 15. I am not sure what that means and they don't disclose how they are scoring that. Moreover, while this qualitative-heavy metric system gave the management 96% payout in 2021, the board later decided to award them 100% in 2021 anyway because of "the strength of the organization’s performance and acknowledgement that the performance is capped at target for each priority even where attainment exceeded target". That sounds like compensation committee didn't actually do a good job in devising a sound incentive structure.”

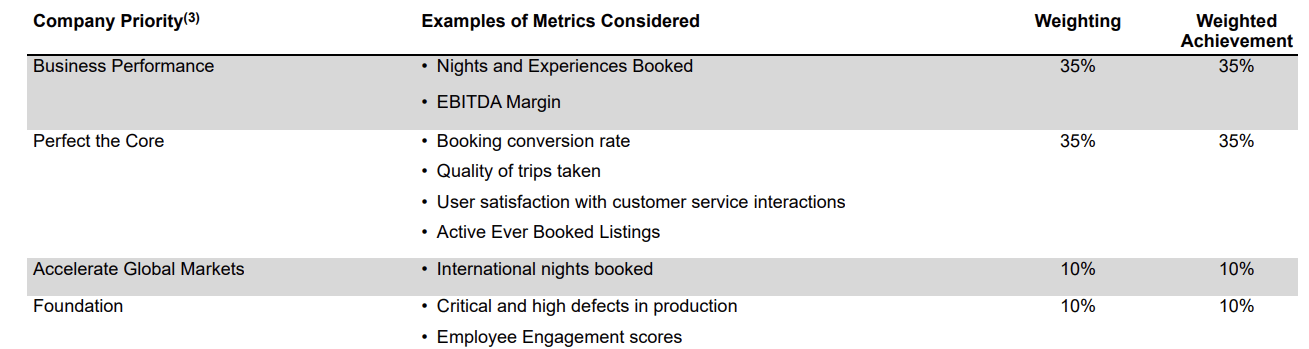

While the metrics related to annual incentive changed over the years, there were still plenty of qualitative factors even in the 2025 annual incentives.

Thankfully, things are changing in 2026. I took note of the following in Airbnb’s 2025 proxy statement (emphasis mine):

“Beginning in 2026, the people and compensation committee determined to simplify the Bonus Plan structure to focus on key financial metrics that are aligned with Airbnb’s business priorities for the year. Payouts will incentivize revenue growth, which accounts for 75% of the target performance weighting, with the remaining 25% based on Adjusted EBITDA Margin performance.”

I am heartened to see the board has eliminated all the qualitative factors which are much easier to game, as evidenced by the fact that management has consistently received full scores in them. For a company that is battling the “mature” label in their core business, revenue growth is the primary weapon to dispel such concern. This incentive system makes it abundantly clear that management too is acutely focused on this metric. The fact that adjusted EBITDA margin still had 25% weight assuages the concern that management won’t necessarily pursue revenue growth with little concern for margin. Of course, you can (rightly) scoff at the idea of “adjusted EBITDA margin” which conveniently adds back stock based compensation. We are looking at a “Silicon Valley” company after all which are increasingly quite “innovative” in financial reporting; so I guess we cannot expect to cure them of all the diseases at once, but Airbnb is certainly on the right track with their incentive tweaks in 2026.

Subscribers get the daily journal and five+ years of Deep Dives, i.e. full-length analyses with financial models on 65+ companies. The daily is just how I think out loud between the Deep Dives!

Current Portfolio

Please note that these are NOT my recommendation to buy/sell these securities, but just disclosure from my end so that you can assess potential biases that I may have because of my own personal portfolio holdings. Always consider my write-up my personal investing journal and never forget my objectives, risk tolerance, and constraints may have no resemblance to yours.

My current portfolio is disclosed below: