Walmart and Target CY 3Q'25 Earnings

It is a bit strange co-incidence, but CY3Q’25 was the last earnings call for both the current CEOs of Walmart and Target. However, the backdrop in which they are passing down the baton to the next person perhaps couldn’t be any more different.

In both cases, the new leadership is coming from internal talent bench. Target’s new CEO Michael Fiddelke joined the company as a finance intern back in 2003 and rose through the ranks to become CFO in 2019, then COO in 2024, and now finally CEO. Walmart’s new CEO John Furner had an even more endearing story. He joined Walmart as a part‑time hourly associate in 1993. As if that were not convincing enough that Furner lives and breathes the Walmart ethos, he even got his degree from Sam Walton College of Business at the University of Arkansas in 1996.

The reason the mood around the leadership change is very different in these two retailers can be encapsulated very quickly if you look at their same store sales (SSS) growth in the last four years. Remarkably, nine out of the last 10 quarters, Target’s SSS growth was negative whereas Walmart just kept cruising along at close to mid-single digit SSS growth during this period.

Their stock performance appropriately reflected this reality. In the last five years, Walmart’s stock was comfortably ahead of S&P 500’s return whereas Target’s stock declined ~44% over the last five years. Given how challenging it is to turn around a retailer, the new CEO at Target will have a much more difficult hand.

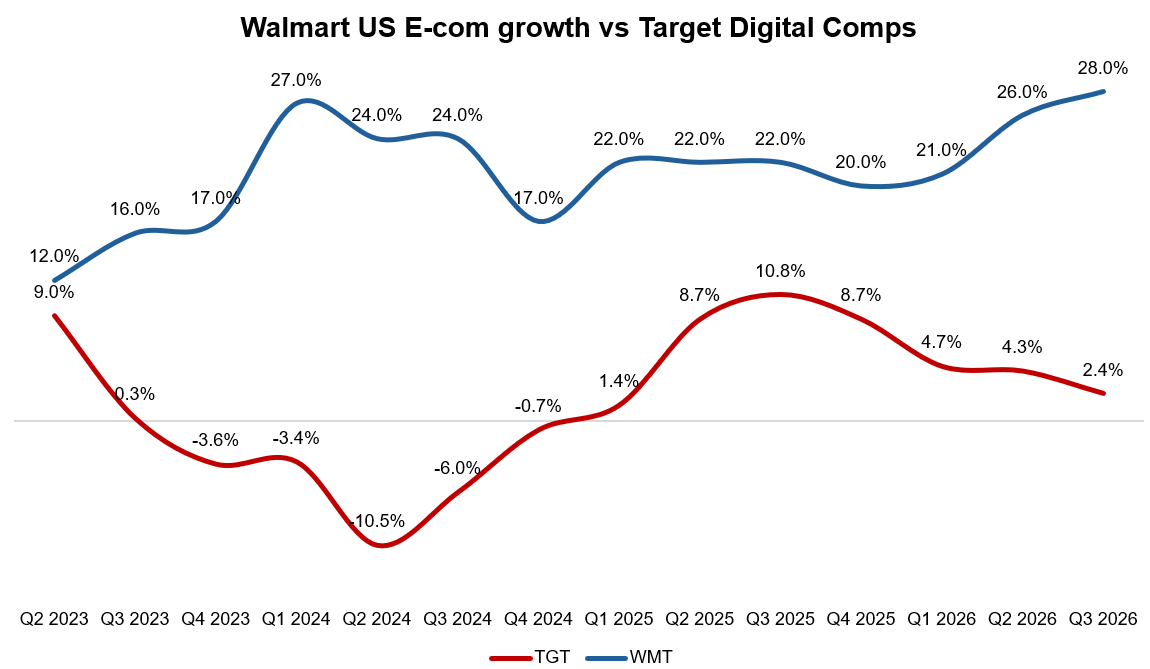

One of the key reasons for such a massive divergence between these two retailers performance is e-commerce. Walmart has been growing their US e-commerce business for 20%+ in the last seven consecutive quarters and growth has, in fact, accelerated in the last two quarters. Target’s digital comp, on the other hand, has limped towards low single digit!

Walmart’s e‑com is tied to high‑frequency, non‑discretionary missions (grocery is ~60% of their US sales), while Target’s digital gains are trying to swim upstream against a discretionary slowdown. That alone explains a big chunk of the growth gap, but perhaps far from the entire story.

While Target painted a picture of a somewhat pressured consumer, citing sentiment at a “3-year low” and that shoppers are “stretching budgets”, Walmart’s commentary hints at much of the pressure is limited to lower income families. Inflation in Walmart is also at LSD. From the call:

As we look at our customers and members here in the U.S., they’re still spending with upper and middle income households driving our growth. We continue to benefit from higher income families choosing to shop with us more often. Middle income households have been steady, and while lower income families have been under additional pressure of late, we’re encouraged by how our teams are meeting them with greater value across necessities and doing what we can to help them stretch their dollars further.

For the quarter, like-for-like inflation in Walmart U.S. was 1.3% with food and general merchandise up low single digits.

Walmart mentioned advertising and membership fees was one-third of their operating income now. While that’s impressive, it still pales in comparison with Amazon. This isn’t quite apple-to-apple comparison since ~10-20% of Amazon’s advertising revenues come outside its marketplace business and its Prime subscription has broader scope than Walmart’s membership, they can still be helpful to gauge the context. Amazon’s LTM advertising and subscription fees was ~$113 Billion which was 3.5x of its LTM operating income ex-AWS!

Nonetheless, Walmart clearly got the memo where the future of retail is heading while Target appears to have been caught sleeping in the last 5 years. Walmart correctly realized that you need 3P sellers and your entire retail infrastructure needs to undergo technological transformation to be able to compete against the 800 pound gorilla named Amazon. In CY 2Q’25 call, Walmart mentioned ~44% of their marketplace flew through Walmart Fulfillment Services (WFS) and in CY 3Q’25 call they mentioned, half of the fulfillment center volume is now automated. Target’s in‑store fulfillment model now looks less scalable and less efficient than the robotics‑heavy systems at Walmart/Amazon, and I’m, frankly speaking, not sure they can ever catch up at this point. One reason for such pessimism is what I discussed in my Instacart Deep Dive last month:

Walmart has been investing in perfecting delivery for the last few years. While they don’t disclose how much of their orders are coming from Instacart compared to demand coming from their own app, my guess is supermajority of their e-commerce sales is coming from their owned and operated app/website. They invested in their own “Spark” platform which is Walmart’s own last-mile delivery service for independent contractors to deliver grocery to Walmart’s customers. Even in 2022, they mentioned ~75% of their deliveries were fulfilled by drivers on Spark platform. Despite such end to end control and order density, Walmart only achieved overall e-commerce profitability for the first time in FY 1Q’26. It is safe to assume that it will take a while for the most of the rest of the retailers to reach profitability, let alone matching the profitability level seen in their own stores.

Walmart’s speed of delivery is really the killer differentiation. ~35% of their digital orders were delivered in under 3 hours in 3Q’25. In their China operation where e-commerce has ~50% penetration (vs ~20% in the US), Walmart delivers ~80% of the orders in under an hour. I don’t quite expect that to replicate anytime soon in the US, but speed of delivery is certainly going to be one-way street.

Walmart mentioned in the call that their fastest growth channel is the orders that get delivered in less than an hour and as the order density grows, fulfillment and shipping cost will decline further and they can afford to invest more aggressively to accelerate delivery speed even more. From the call:

more than 50% of our volume from fulfillment centers is coming from automation. And that translates into lower shipping costs. Our shipping costs have been down consistently for many quarters in the 30% range. This was another quarter where we saw double-digit improvements. And that really helps our e-commerce economics, but also helps the overall SG&A of the company.

The best bet for most of the retailers like Target is to partner with the likes of Instacart/DoorDash to stay competitive in delivery speed. It’s still likely going to be inferior given the lack of end-to-end control over the entire value chain, and perhaps more importantly, having another middleman to share your already thin margin with is not going to be pretty outcome for most retailers.

Walmart’s partnership with ChatGPT was briefly discussed, but we didn’t learn anything new. During the call, management did mention that more than 40% of the new code is either AI-generated or AI-assisted.

Walmart also had a very interesting example about how they are using WhatsApp to drive e-com in Chile. As I have mentioned recently, it can be hard to appreciate the power of WhatsApp unless you live outside North America.

One of the things that’s useful about having an international segment is that we have markets where we can trial new capabilities. And we’ve been trialing something called Carrito Listo down in Chile, where we actually create customers’ orders for them, send them a WhatsApp prompt to ask them if they’re interested in buying that basket. They go into the app, and they can see we’ve created a basket for them that actually has all the brands that they normally buy in the kind of intervals that they like to buy it. And they have full agency over whether they want to accept that basket, whether they want to add to the basket, whether they want to take from the basket. And what we’re seeing is that it’s really attractive, and it’s become up to about 20% of our e-comm business in Chile already.

Bill Gates once described how to identify whether a company is platform or not: “A platform is when the economic value of everybody that uses it, exceeds the value of the company that creates it. Then it’s a platform.”

WhatsApp is so little monetized relative to the value millions of companies likely generate in most international markets in the world, I wonder if it’s the platform that has the highest differential between the value it captures and the value others generate from it. Perhaps Meta will look to narrow this differential in the next 5-10 years!

In addition to “Daily Dose” (yes, DAILY) like this, MBI Deep Dives publishes one Deep Dive on a publicly listed company every month. You can find all the 64 Deep Dives here.

Current Portfolio:

Please note that these are NOT my recommendation to buy/sell these securities, but just disclosure from my end so that you can assess potential biases that I may have because of my own personal portfolio holdings. Always consider my write-up my personal investing journal and never forget my objectives, risk tolerance, and constraints may have no resemblance to yours.

My current portfolio is disclosed below: