Scuttleblurb on Ryan Specialty

It doesn’t happen often, but right after publishing my Deep Dive on Ryan Specialty Group last week, my friend Scuttleblurb also published on the same company. Scuttleblurb’s work is excellent as usual, and there are a couple of things that I want to highlight from Scuttleblurb’s piece which I believe are additive to my Deep Dive.

I have heard this murmur from insurance broker bears that the rise of MGAs may have led to lower underwriting quality since they don’t take the actual underwriting risk on their balance sheets. However, Scuttleblurb shared an interesting data point that showed the loss ratios are broadly similar for MGAs compared to the broader P&C industry. He also highlighted that the popularity of MGAs itself may be cyclical in nature, something I haven’t quite fully appreciated before. From Scuttleblurb (all emphasis mine):

“many MGAs earn substantial contingent commissions tied to the profitability of the business they write, which creates a direct economic incentive for disciplined risk selection. For example, in the 12 months through June 2024, after several years of exceptional underwriting performance, US Assure – an MGA later acquired by Ryan – generated 30% of its revenue, and an even larger share of its EBITDA, from profit commissions.

Overall, the loss ratios of MGA-focused carriers appear to be broadly in line with those of the wider P&C industry

…as with the E&S market more broadly, MGA penetration tends to rise and fall with the underwriting cycle, and a large portion of MGA share gains over the past decade came after 2020, as the market began to harden. MGAs may well represent a secular growth segment, but it is also possible that, after several years of extraordinary expansion, we are closer to a cyclical high-water mark and that future share gains will slow, or even reverse, if the E&S market softens. I’d be wary of extrapolating recent growth rates too far out.”

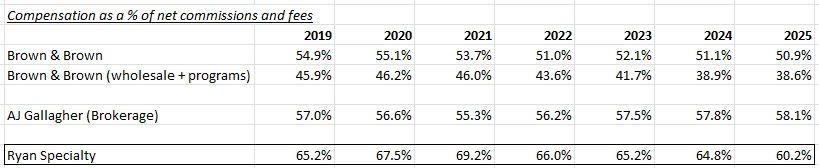

Another tidbit that is worth highlighting from Scuttleblurb’s piece is his benchmarking RYAN’s compensation related costs against Brown & Brown, and Arthur J. Gallagher. From Scuttleblurb (emphasis mine):

“Where Ryan appears to stand out is in how much of that value it is willing to share. In 2025, it paid out 60% of net commissions and fees as compensation (~$295k+ per employee) while Brown & Brown’s combined wholesale and delegated underwriting segments paid out a combined 39% ($116k per employee). In 2022, management disclosed employees other than Pat Ryan owned nearly 20% of the company. As of 2025, around 16% of Ryan’s employees counted themselves shareholders. The firm retains ~97% of its producers, all top 50 of whom own stock.”

I didn’t notice until reading Scuttleblurb’s piece the difference in compensation intensity between Brown & Brown and other brokers such as RYAN and Gallagher. Frankly speaking, when I looked at this data, it quickly reminded me of Brown & Brown’s lawsuit against Howden. I highlighted this lawsuit last month and wrote the following:

I am not a lawyer, but some evidence seems quite damning for these employees who seem to have deliberately siphoned customers away from BRO to Howden. Nonetheless, it doesn’t reflect great on BRO’s culture that a couple hundred employees chose to do such deliberate attempt to hurt the company.

Indeed, looking at the difference in compensation intensity, I wondered whether the employees who left Brown & Brown for Howden are just indicative of much broader problem of stingy compensation culture at Brown & Brown relative to the industry. I will share some additional thoughts behind the paywall on how I decided to incorporate these thoughts in my portfolio.

In addition to “Daily Dose” (yes, DAILY) like this, MBI Deep Dives publishes one Deep Dive on a publicly listed company every month. You can find all the 66 Deep Dives here.

Current Portfolio:

Please note that these are NOT my recommendation to buy/sell these securities, but just disclosure from my end so that you can assess potential biases that I may have because of my own personal portfolio holdings. Always consider my write-up my personal investing journal and never forget my objectives, risk tolerance, and constraints may have no resemblance to yours.