FICO: Deconstructing the Monopoly Margins

Programming Note: This is part-2 of my FICO series. In Part 1, I covered FICO’s history through the 2018-2025 pricing-power era, where the score business finally started capturing the rents it had been giving away to the credit bureaus for three decades. In today’s post, my focus is on understanding the business itself in a bit more granular level.

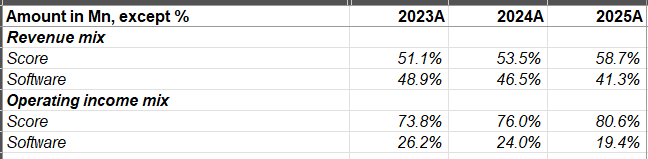

FICO reports its results in two segments: Scores and Software. The Scores segment is, of course, the legendary monopoly i.e. the FICO Score business that drives the stock, and well…the antitrust lawsuits The Software segment is essentially everything else FICO does such as a decision management platform suite built originally on top of the HNC Software acquisition in 2002. Both segments serve overlapping financial institution customers, but the economics are so different that you really should think of FICO as two businesses stapled together.

In FY’25, Scores generated $1.2 Billion in revenue at operating margins of ~88%, while Software generated $822 Million at far more modest operating margin of…30%. Given the margin differential, even though ~40% of FICO’s overall revenue comes from the software segment, only ~20% of its operating income is driven by software segment.

Let’s start with Scores, because that’s clearly where the action is.

The Scores segment splits cleanly into B2B Scores (FICO sells its score wholesale to lenders, via the credit bureaus) and B2C Scores (FICO sells directly to consumers through myFICO.com and a handful of partner channels). B2B is ~80% of segment revenue and effectively all of the profit. Back in 2019, B2B used to be ~70% of Scores revenue. Given B2B is the faster and almost all the profit of Score segment, I’ll focus more on B2B Scores.

Within B2B, FICO breaks the business down by what kind of lending decision the score is being used for. The buckets are mortgage originations, auto originations, and credit card, personal loan, and other originations. Mortgage has become by far the most important, both because the per-score price is highest, and because the strategic conversation about FICO’s pricing power is almost entirely a conversation about mortgage. The rest of this post will be behind the paywall.

Subscribers get the daily journal and five+ years of Deep Dives, i.e. full-length analyses with financial models on 65+ companies. The daily is just how I think out loud between the Deep Dives!