FICO: Pricing the Standard

Programming note: As I have mentioned earlier, I am making some changes in how I publish my Deep Dives. Instead of publishing one big Deep Dive, I will do a series of posts on a particular company over multiple weeks. Today I am publishing first of such multiple posts on FICO series.

Any modern financial system operates on a foundation of trust, but historically, quantifying that trust was a highly subjective and presumably flawed endeavor. Prior to the widespread adoption of statistical credit scoring, lending decisions were governed almost entirely by qualitative judgments. These rudimentary frameworks relied heavily on the personal discretion of local loan officers who evaluated applicants based on isolated knock-out criteria or, more nefariously, subjective character judgments that routinely penalized borrowers based on gender, marital status, race, or geographic location. If a borrower failed to meet a single arbitrary criterion, their application was denied without any holistic consideration of compensating positive factors.

The solution to this systemic flaw had been conceptualized back in 1950s. In 1956, an engineer named William Fair and a mathematician named Earl Isaac pooled a modest investment of $400 to found Fair Isaac Company or FICO . The two founders had previously met at the Stanford Research Institute, where they applied operations research and statistical analysis to complex military problems. Seeking a civilian application for their highly specialized expertise, they pivoted to consumer finance. By 1958, they had developed their first primitive credit scoring algorithm, introducing the “radical” notion that a borrower's past financial behavior could statistically and reliably predict their future likelihood of repayment.

The legal foundation for FICO’s eventual ubiquity was laid in the 1970s. Congress enacted the Equal Credit Opportunity Act (ECOA) in 1974, initially prohibiting credit discrimination on the basis of sex and marital status. A 1976 amendment expanded the protected classes to race, color, religion, national origin, age, and receipt of public assistance. ECOA effectively gave a green light to statistical credit scoring, but only if any such system was “empirically derived” and “demonstrably and statistically sound”.

That single phrase transformed FICO’s quirky math-consulting practice into a legally privileged way of making lending decisions. A properly built statistical model became an affirmative defense against discrimination claims while a loan officer’s gut feel was a liability waiting to happen. With the emergence of credit score, ECOA led to a cascade of improvements in credit access.

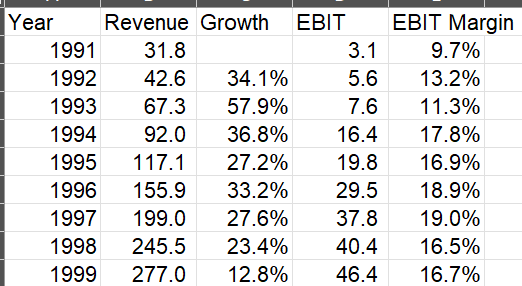

Despite the regulatory tailwind, FICO’s path to scale was rather slow. Through the 1970s and into the early 1980s, FICO’s bread and butter was actually custom, bespoke scoring models built for one client at a time e.g. a department-store scorecard for one retailer, a credit-card scorecard for one bank etc. The economics was lumpy; in 1981 the company posted ~$6 Million of revenue but still booked a loss. By the time of its IPO in 1987, revenue had reached $18 Million with ~$2 Million of profit.

The truly category-defining move came two years after the IPO. In 1989, FICO released the first general-purpose FICO score: a single algorithm any lender could buy off the shelf rather than commissioning a custom-built scorecard. This algorithm synthesized the raw, highly complex data housed within credit-bureau files into a single, easily digestible three-digit number ranging from 300 to 850, providing a standardized measure of default risk across the entire industry. A classic FICO score mathematically weighs five core components of a consumer’s credit profile, prioritizing payment history and total credit utilization heavily above length of credit history, mix of credit types, and recent inquiries. By 1991, FICO had made its credit-bureau risk scores available at all three major U.S. consumer reporting agencies or CRAs (Equifax, Experian, and TransUnion) so that a lender could pull the FICO scores from any bureau.

I went through FICO’s financial statements since 1991 (I couldn’t find their 1989-90 financials on their website). I have noticed many investors tie FICO’s utter dominance in the 90s to be direct consequence of the GSE decision in 1995. Bristlemoon Capital made a compelling argument that FICO’s monopoly didn’t quite derive from the blessings of the US government. From Bristlemoon Capital’s piece on FICO:

“The pivotal moment for the FICO Score came in 1995 when the GSEs Fannie Mae and Freddie Mac directed lenders to use FICO scores for all new residential mortgage applications. Notably, this was when Fannie Mae and Freddie Mac were for-profit enterprises owned by private shareholders; these corporations voluntarily adopted the FICO Score, given that lenders were already using it to evaluate credit risk in mortgage and non-mortgage markets (i.e., FICO’s monopoly in U.S. mortgages was not granted by government decree but rather guided by market forces). This cemented the FICO Score as the industry standard for U.S. residential mortgages, but lender adoption more broadly also saw the FICO Score become dominant in other verticals such as auto loans and credit cards.

The erroneous notion that FICO is only dominant because of its government mandated use in the conforming mortgage loan market is best rebutted when we see that the majority of FICO Scores are used outside of mortgage originations. In a blog post by the President of FICO’s Scores business, Jim Wehmann revealed that 99% of FICO Scores are used outside of mortgage originations.”

Indeed, if you look at FICO’s operating performance before the 1995 GSE decision, it does seem the company didn’t really need a helping hand from the government to utterly dominate their niche. FICO’s revenue was already compounding at almost 40% annually between 1991 and 1995. By the end of the decade, FICO was approaching $300 million revenue and $50 million operating profit even though they started the decade with just ~$30 million revenue.

Multiple structural forces were doing the work. First, U.S. credit-card issuance was booming, and credit-card issuers had neither the time nor the manpower to manually underwrite tens of millions of applications. Automated, score-based underwriting became the only viable workflow. Second, ECOA was now well past its effective date and was being actively enforced, putting any remaining holdouts on legal notice. Third, the 1991 availability of FICO at all three bureaus meant FICO simply was the empirically derived, demonstrably and statistically sound standard the regulators were asking for. By the time the GSEs were debating which credit score to require for mortgages, the industry had already voted with its workflow. By one estimate, ~30% of lenders were using FICO in 1995; that share rose to over 90% by 1999.

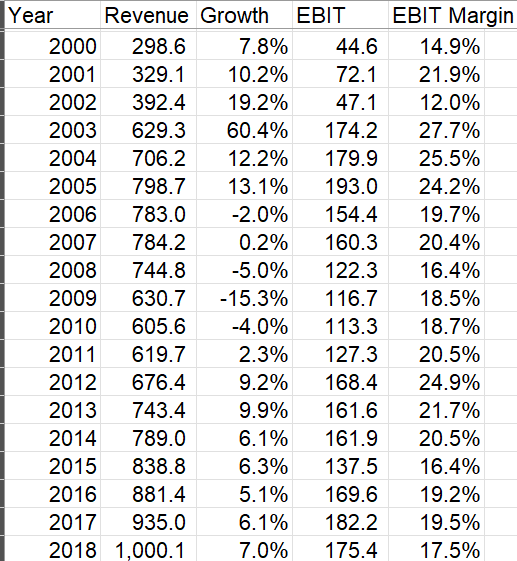

The 1995 GSE adoption, combined with FICO’s already-dominant share in credit cards and autos, set up a glorious early-2000s run for the company. Mortgage origination volumes ballooned through the housing boom, and FICO got paid per score on essentially every mortgage origination. Then in August 2002 acquisition of HNC Software brought in the Falcon Fraud Manager, Capstone Decision Manager, RoamEx, and Blaze Advisor product suites under FICO’s umbrella. The HNC deal essentially built FICO’s software business outside of their traditional Scores business.

However, the structural weakness of the Score business surfaced in painful fashion when the housing cycle turned. Revenue peaked in 2005 at almost $800 million and operating income peaked the same year when it was approaching $200 million. From there, it was a long, grinding round-trip. FICO didn’t exceed its 2005 revenue level FOR ALMOST A DECADE and operating income took even longer!

Why was a company with ~90%+ market share so utterly hostage to the macro cycle? Because price was effectively frozen. FICO’s wholesale royalties on mortgage scores were originally set in 1989 and as FICO CEO Will Lansing not-so-fondly reminisced, “remained at those low amounts for decades due to contractual and technical constraints. As a result, the royalty rates that FICO received from each of the CRAs were essentially flat for nearly 30 years after the FICO Score was introduced in 1989.”

Lansing is, however, determined to correct this historical “wrong”.

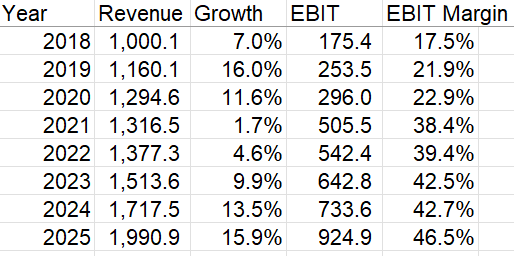

FICO had no contractual right to push prices higher without renegotiation with the credit bureaus/CRAs. In 2012, FICO began the multi-year process of renegotiating those agreements; the new agreements eventually gave FICO “the right to adjust its base royalty rates for FICO Scores once per year, with advance notice to the CRAs”. With the renegotiated contracts finally in hand, FICO began raising mortgage royalties in 2018 and the impact on the income statement is hard to overstate. Revenue went from $1 Billion in 2018 to almost $2 Billion in 2025, but the incremental operating margin on these revenue was eyewatering 75%!! Most of that operating leverage is being generated in the asset-light Scores segment where almost every incremental royalty dollar drops straight to the bottom line.

Predictably, the stock soared as investors woke up to the reality of such an unbelievable incremental economics of a monopoly that is finally able to exercise pricing power. From the end of 2018, the stock became a 10-bagger by the end of 2024!

The only problem is while Lansing was determined to ensure FICO gets to keep what he thinks it truly deserves, the percentage increase in prices ended up being, to say it mildly, a little…obscene.

I can’t stop laughing at the FICO management team. I’ve been thinking about it non-stop since I learned about it

— BuccoCapital Bloke (@buccocapital) July 9, 2025

ChatGPT can’t find any examples of anyone doing something even remotely like what they did. I doubt it exists. pic.twitter.com/7AMMung9nX

As you can imagine, such price increases attracted plenty of attention in DC! Bill Pulte, Director of the Federal Housing Finance Agency (FHFA) which oversees the secondary mortgage market and regulates GSEs, appears to be very eager to introduce some competition to FICO which led to plenty of nervousness among FICO’s shareholders.

For much of FICO’s existence, the Score business had monopoly market share but virtually no monopoly pricing power; the economic rents flowed downstream to the credit bureaus and tri-merge resellers, who marked up the score on the way to the lender. As I alluded before, the 2018–2025 chapter is the story of those rents migrating back upstream to the monopoly itself. I’m only scratching the surface here, but the rest of this series will dig into more granular details. I hope to publish the next part of this series later next week.

Subscribers get the daily journal and five+ years of Deep Dives, i.e. full-length analyses with financial models on 65+ companies. The daily is just how I think out loud between the Deep Dive

Current Portfolio

Please note that these are NOT my recommendation to buy/sell these securities, but just disclosure from my end so that you can assess potential biases that I may have because of my own personal portfolio holdings. Always consider my write-up my personal investing journal and never forget my objectives, risk tolerance, and constraints may have no resemblance to yours.

My current portfolio is disclosed below: