Constellation Software 1Q’26: Leaning In Amidst the SaaSpocalypse

During the current “SaaSpocalypse”, Constellation Software (CSU) delivered a slightly uneven but, in important ways, also encouraging quarter. Organic growth softened and margins took the usual Q1 hit (and a bit more), but capital deployment pace (which is why anyone really owns the stock) remains a key bright spot.

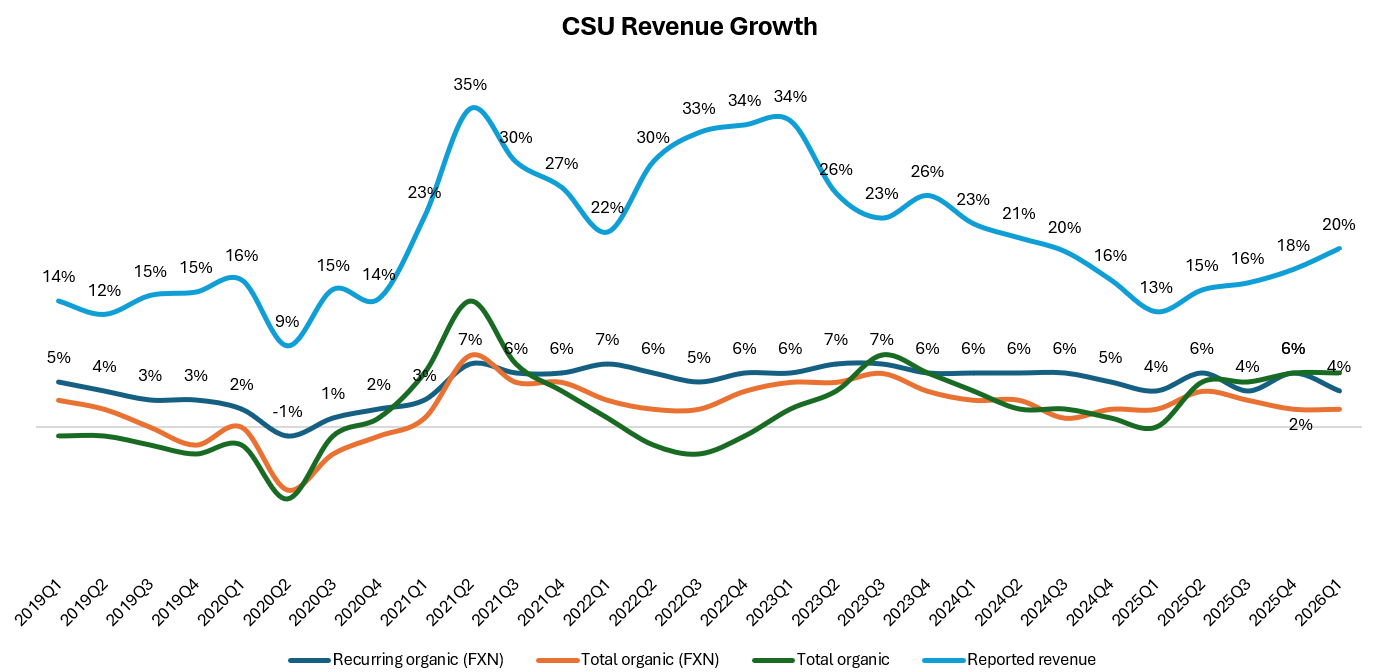

Maintenance and other recurring revenue, which is ~77% of total revenue, decelerated from 6% in in 4Q’25 to 4% (FXN) in 1Q’26. Since 1Q’19, CSU’s average recurring organic growth was 4.8%, so this was a below average quarter for CSU on organic growth front. Excluding Altera, organic growth in recurring revenue was +5% (vs +6% in 4Q’25 but the same as 1Q’25).

This is the part where 5-6 years ago, an investor might shrug. But today when much of the bear case on CSU is some flavor of “AI is going to eat your shitty software,” even a slightly below average number invites scrutiny and discomfort. To be clear, CEO Mark Miller also wants CSU to post better organic growth. From the call:

“I continue to pressure our businesses on organic growth generally…I really would like to see them doing a better job on organic growth across the board, and I think this is an opportunity to push them harder on that with the advent of some tools to allow you to do things a little bit faster and a little bit better.”

CFO Jamal Baksh was more measured and thought the internal AI tooling will eventually show up in revenue, but it will take “some time”. Miller also reminded the typical reasons for how CSU loses customers and Why AI should lead to additional opportunities. From the call (emphasis mine):

“…the way we lose customers is, they get essentially go out of business, which happens, you can’t do much about that. They’re acquired by other customers, particularly larger customers. That’s another way of losing. You can’t do much about that. Other than you hope you -- the other customer that buys them is your customer. Pricing is the third and pricing, rarely, we lose customers on pricing because the switching is painful for customers and it’s working and they’re using it and retraining all their users and adapting the interfaces to make it work and make it harder. Where you lose customers is when the competitor can provide something much different than you can provide that the customer really needs. And that’s where I always worry the most, just generically forgetting about AI. So that’s kind of how I sort of look at it.

Now as far as these tools, we’re all using them internally. And I’ve been fortunate enough to travel around. I think each week, I’ve met with a different group of Constellation in different location and just see what they’re using and what they’re doing, and they’re adapting to these tools, using them internally to help them run their portfolios, their businesses better. But they’re also using -- to try to develop more software to actually expand our presence inside of customers more so than defend our presence is kind of the thinking, but it’s going to depend on our business. So I look at these tools as an opportunity to do more for customers, not do what we currently do more efficiently, although that will happen in some cases..”

These arguments will sound lot more credible if CSU can accelerate their organic growth.

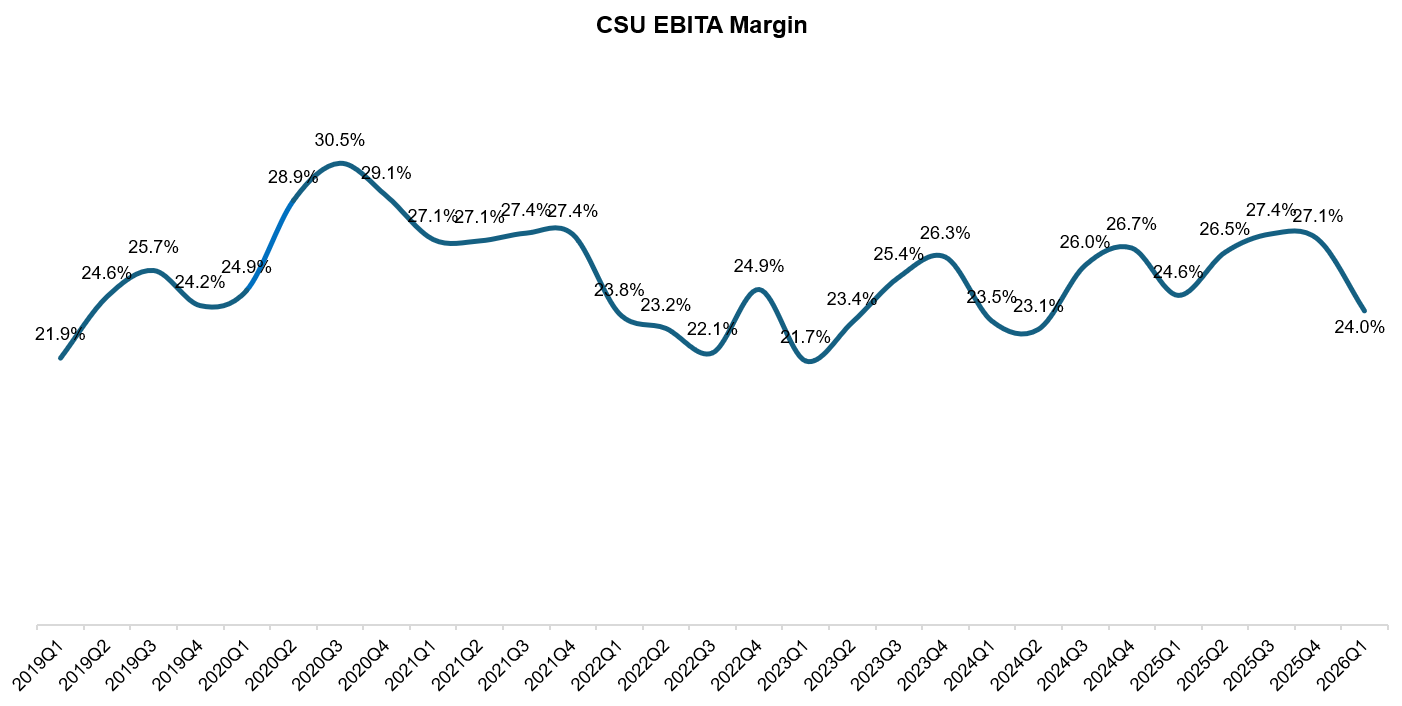

EBITA margin came in at 24.0% for the quarter, ~60 bps below 1Q’25 and the customary ~300 bps below 4Q (the latter is just Q1 seasonality, as payroll taxes reset and you eat the bill in Q1). CFO mentioned CSU had a couple of acquisitions that were drag on margins which was expected and they plan on improving the margins on those acquisitions (typical CSU playbook). So, slight down tick in margins doesn’t seem to be concerning.

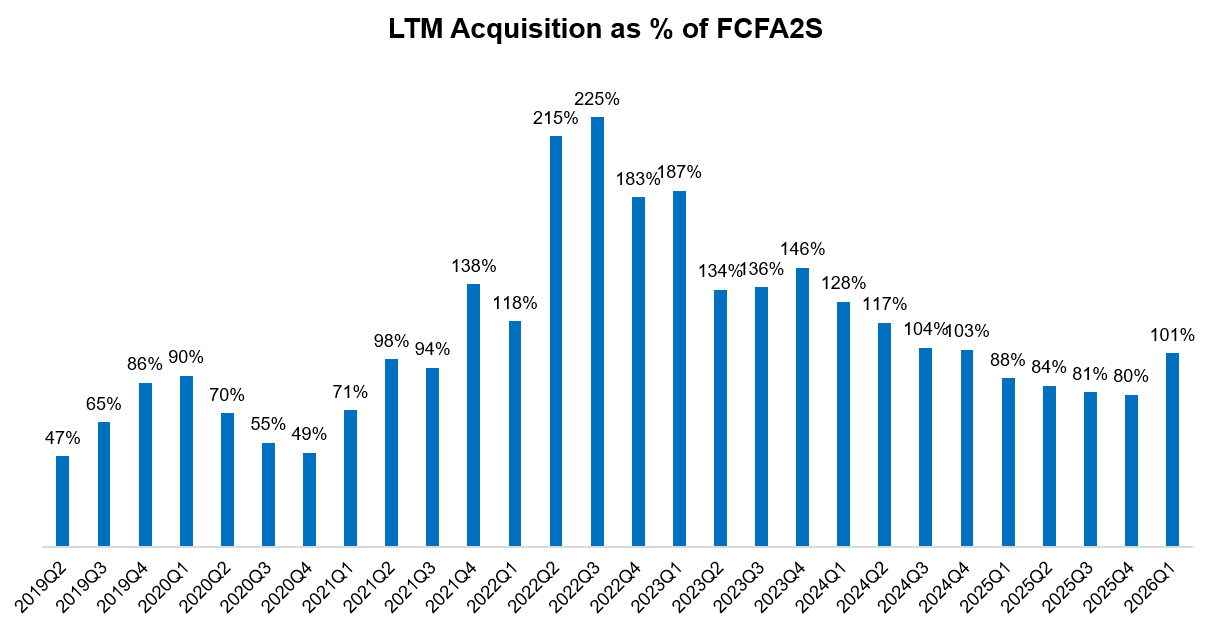

The highlight of this quarter, however, is acquisitions. CSU deployed $809 million in Q1 (cash + estimated deferred). On top of that, the filing disclosed that through the first ~six weeks of Q2 the company has already closed or has open commitments on a further $786 million worth of deals. Combined, that’s ~$1.6 billion in roughly four and a half months, an amount that’s higher than their cash deployment in the entire 2025. In fact, LTM acquisitions as a percentage of FCFA2S has now crossed 100% for the first time since 2024. This is without even considering their recent PEMS deals. Clearly, CSU is leaning in to deploy capital in size which may be getting overshadowed by Saaspocalypse concerns.

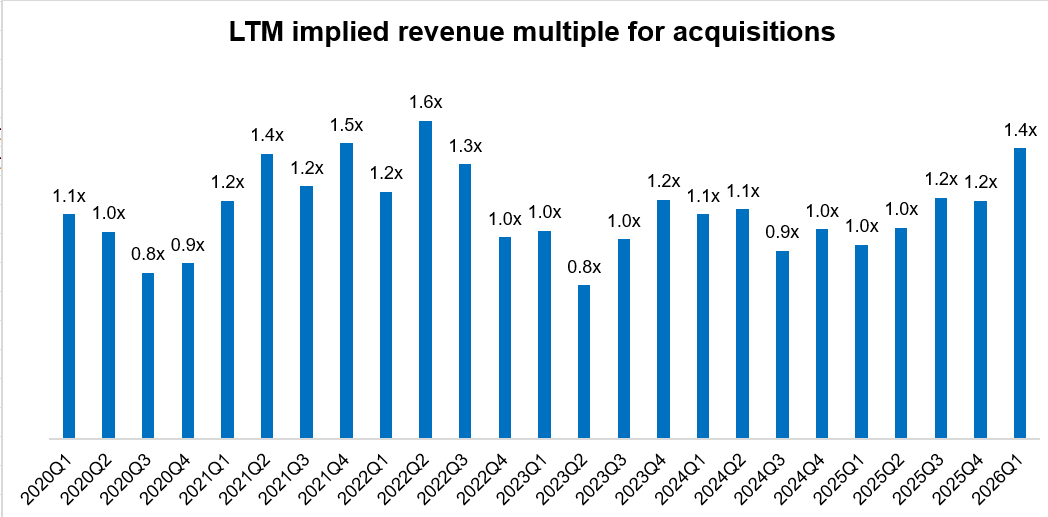

The natural follow-up question is whether the implied price has gone up too. The answer is: yes, a little but it’s pretty much within what we have seen historically. One would imagine CSU would be able to buy assets cheaper than usual amidst the SaaSpocalypse narrative, but management mentioned valuation hasn’t really gone down that much in areas they typically play. Well, when you’re paying ~1-1.5x revenue for acquisitions, the supply of such sellers willing to part with their lifetime work for even lower than 1x revenue is not exactly elastic. Miller also explicitly mentioned “There’s a real disconnect between the SaaSpocalypse publicly traded stuff and private markets” which likely explains why they’re interested in PEMS in the first place.

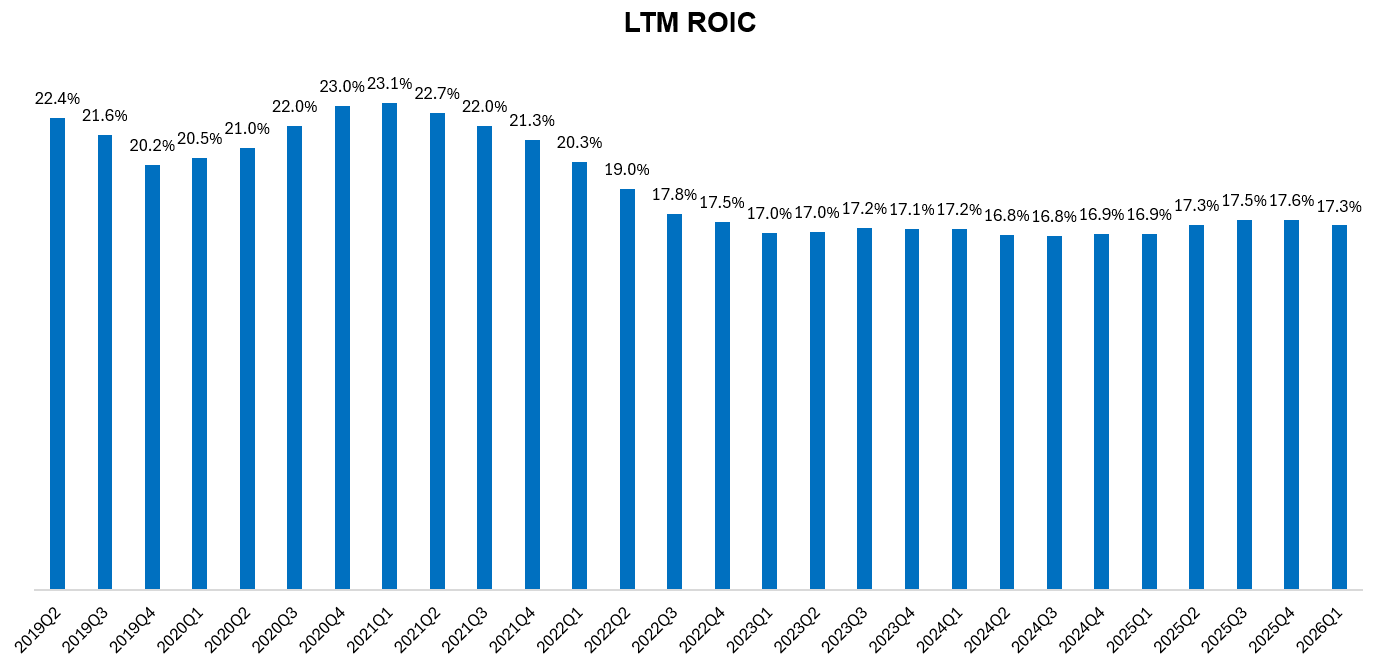

Thanks to their valuation discipline for these acquisitions, CSU’s ROIC remains quite stable. (FYI, read this post to understand how I calculated CSU’s ROIC. Also note that I have excluded PEMS investments from invested capital base since the associated return is not incorporated in numerator. More on this later.)

Three years ago, CSU had ~$8 Billion of invested capital with 17.0% LTM ROIC. If a genie came to you then and told you in the next three years CSU would deploy incremental ~$8 Billion capital while maintaining their overall ROIC, you probably would think that was your lucky day! Well, not quite. The stock is almost flat for the last three years despite delivering results that should be quite satisfactory to most bulls. In case you needed another reminder “investing is hard”, let this be a good example. While investors are often judged based on past 3-5 year performance (if they’re lucky), the reality is even 3-5 year return for a stock can be largely dictated by the narrative around your “exit multiple” year. Unless you experience it first hand yourself, it’s sort of hard to appreciate the punishing nature of being on the wrong side of the narrative. I had that moment back in 2022 with Meta.

To be clear, bears will rightly argue that ROIC is a lagging metric and cannot tell you how the future will pan out. Of course, that’s true and at current prices, market is clearly telling you that the future trajectory of these metrics will likely be decidedly different. I will expand on CSU’s current valuation behind the paywall.

Subscribers get the daily journal and five+ years of Deep Dives, i.e. full-length analyses with financial models on 65+ companies. The daily is just how I think out loud between the Deep Dives!