Airbnb's Fintech Opportunity

Airbnb first launched its guest travel insurance product in 2022. Then in 4Q’22 call, Brian Chesky mentioned that the guest insurance product was available in 8 countries and the product had been “really, really successful”. However, Airbnb didn’t quite provide much detail about the product’s trajectory until 3Q’25 call when they mentioned guest insurance availability expanded to 12 countries and revenue from guest insurance was growing “over 25% year-over-year”. In fact, revenue from this product increased by 40% in full year 2025. Then in the most recent earnings, Airbnb disclosed that growth has accelerated further to 45% in 1Q’26. More interestingly, Airbnb explicitly called out their insurance program for take rate expansion for full-year 2026.

In the recent shareholder letter, Airbnb also clearly hinted that they’re planning to launch more insurance related products (emphasis mine):

“We are excited by the performance of this offering over the past few years and have begun piloting additional forms of insurance products to support both guests and hosts.”

We are starting to see Airbnb graduating some of these pilot programs to public release. For example, early this month Airbnb announced “earnings protection” for hosts. Earnings Protection is an optional, paid insurance product offered in partnership with MIC Global that provides eligible US hosts with supplemental payouts based on historical averages to cover income loss when unexpected external events, like natural disasters or severe property damage, prevent them from hosting.

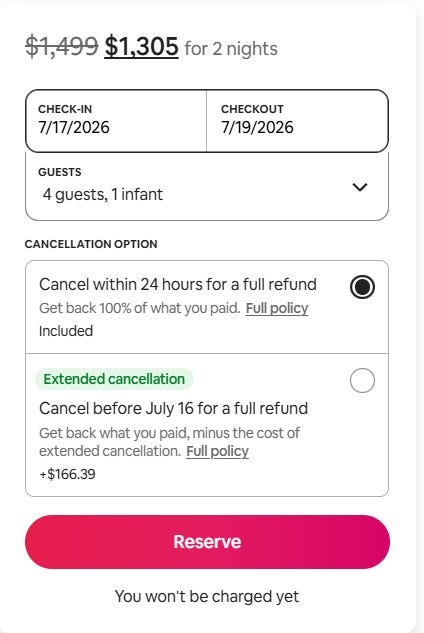

Then yesterday Skift mentioned that Airbnb has started offering “extended cancellation option” for guests recently even though they didn’t publicly announce such product release yet. From Skift:

Airbnb has introduced its first foray into travel fintech with a feature that lets guests pay for the option to cancel a stay for a full refund up to 24 hours before check-in.

The feature, called the extended cancellation option, is currently available in 12 countries including the U.S., Canada, Ireland, the Netherlands, and several others. Eligible hosts need to opt out rather than opt in and most listings with moderate, limited, firm, or strict cancellation policies get automatically enrolled. Airbnb didn’t disclose the amount of the fee, which guests can pay at booking.

Airbnb is working with a third party in powering the feature but wouldn’t identify the partner.

As it turns out, I was actually booking for an Airbnb yesterday for my family’s next month’s trip to Yosemite National Park. I was shown the extended cancellation option which would let me cancel the booking 24 hours before the stay for ~11% of the cost of my entire booking (including tax). Of course, this premium is a contingent liability, so we cannot really think it as a commission on a transaction. The economics are an insurer’s: the fee, collected on every policy, minus the refunds Airbnb must fund when guests do cancel. We also need to consider the servicing and payment costs, and the cut owed to the undisclosed third party “powering” the feature.

If a guest opts for extended cancellation and later indeed cancels the booking, the host is still paid according to their original policy, with Airbnb covering the gap. As you can imagine, the cost of such claim can be lumpy i.e. nothing when a guest cancels early enough that the host was owed nothing, but a large slice of the booking when the cancellation lands deep inside a strict policy’s penalty window.

Of course, this is too early to know what the adoption would be for such a feature and since I don’t know how the economics is going to be divided between Airbnb and the unnamed insurance partner, it’s difficult to estimate the size of the revenue opportunity from Airbnb’s perspective. However, I was a bit surprised how such fintech products seemed to have quite the appeal among travelers when I came to know ~40% of Hopper’s annual revenue in 2022 came from various fintech products. Hopper, a travel booking app, is a private company, so we don’t have detailed updated financials about their business. But I came across this memo from Stack Capital, one of the investors of Hopper, from early 2022. The investment memo also highlighted the range of fintech products Hopper offers to travelers and how that improved their economics. Some excerpt from the memo (emphasis mine):

One of the most successful new initiatives for Hopper has been the introduction of attractive fintech offerings such as “Cancel for any Reason”, “Price Prediction”, “Price Drop Guarantee”, “Price Freeze”, amongst other travel insurance options. These offerings have become increasingly important given the uncertainty surrounding travel during the pandemic, with more consumers now demanding increased flexibility when planning trips.

The Company has also launched its loyalty program, designed to increase engagement through rewards for each booking in the form of “Carrot Cash”, which can net travelers between 1%-5%cash back on every booking, and can instantly be applied to any future flight, hotel, home rental and car rental…The ability for any travel provider to integrate and seamlessly distribute Hopper’s fintech solutions, which have been shown to increase average order value, improve margins, and drive customer satisfaction, represents a significant growth opportunity for the business. Estimated projections indicate that if all travel distribution channels offered travel fintech solutions, it could potentially increase the total consumer spend within the sector by $200 billion annually.

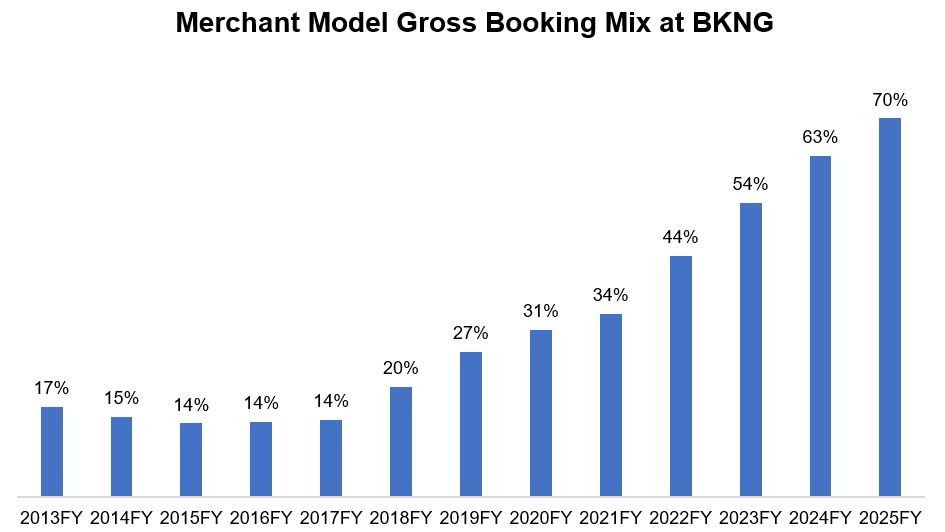

It’s not just Airbnb or Hopper that appreciates the size of the fintech opportunity, I think it’s also one of the reasons Booking Holdings also has been very focused on migrating from agency model (where the hotel collects the guest’s money and Booking merely invoices a commission) to a merchant model, in which Booking takes the payment itself and becomes the merchant of record. While “connected trip” is often mentioned as the primary motivation behind such migration, you can obviously only offer these fintech products if you have full control on the payment. Even in 2019, merchant gross booking was only about a quarter of Booking’s overall gross booking, but it became ~70% of their gross booking by 2025. My guess is a lot of these insurance products will also show up on Booking in not-so-distant future. Of course, Airbnb always was the merchant of record in payment which means they can potentially capitalize on these revenue streams faster than Booking.

While we don’t exactly know how much take rate expansion is possible in the long-term, it seems quite likely that just these plethora of insurance products alone can perhaps expand Airbnb’s take rate by ~50 bps in three to five years. Given Airbnb is approaching $100 Billion Gross Booking Value today, it implies a ~$500 Million very high margin revenue that’s not currently captured in financials today but are likely to show up over time in the next few years. As I highlighted recently, Airbnb management is highly incentivized to accelerate their revenue growth. So perhaps there are lot more potential ancillary revenue streams that will be announced over the next few years.

Subscribers get the daily journal and five+ years of Deep Dives, i.e. full-length analyses with financial models on 65+ companies. The daily is just how I think out loud between the Deep Dives!

Current Portfolio

Please note that these are NOT my recommendation to buy/sell these securities, but just disclosure from my end so that you can assess potential biases that I may have because of my own personal portfolio holdings. Always consider my write-up my personal investing journal and never forget my objectives, risk tolerance, and constraints may have no resemblance to yours.

My current portfolio is disclosed below: