The Shape of Compute Curve

In a recent podcast, Lambda (one of the neoclouds) CTO Stephen Balaban expressed almost bit of a disdain for the critics who wondered whether the hyperscalers or neoclouds are “gaming” the GPU accounting by assuming higher useful lives of the GPUs than warranted. From the podcast:

Matt Turck: You’re running an H100 at a higher rate because why? Because the demand for compute is so rabid that people will take any? Or the technical depreciation of the product is slower than people thought? What drives that?

Stephen Balaban: Well, what’s driving it, I mean, certainly it’s the demand being high increases the price that you’re able to get in the market. There’s no question about that fundamental law. Again, going back to what people didn’t understand about this market. There were people who were saying, “Oh, well, there’s a five-year lifetime, or three-year lifetime,” I even heard some people say three-year lifetime for these GPUs. Completely false. You know, we have GPUs that we commissioned, and we’re one of the earliest neoclouds, in fact, we’re probably the only neocloud that actually has GPUs in our fleet that are fully depreciated from an accounting perspective. Most people are adapting around a six-year accounting depreciation schedule. But that’s not the usable life. The usable life is longer than the accounting depreciation schedule, and what really matters is the economic usable life. And so what we’re starting to see is that the people who were the naysayers—”oh, this is going to be, you’re going to throw these GPUs out in five years”—are completely wrong. They’re completely wrong and they’ve been wrong the entire time.

Given the rental rate even for the older GPUs stayed much higher than most people expected a couple of years ago, I can understand why Balaban is so dismissive of the critics. Nonetheless, I do wonder whether he’s giving too much credit to themselves. Ultimately, whether GPUs have longer useful life or not may depend a lot on whether the demand side of the equation can keep finding compelling and economically useful things to do with such GPUs. If Claude Code or Codex were not a thing in 2026, the demand for GPUs would be lot more sober and the rental rate for older GPUs would be lot lower than it is today. Do the compute sellers have clear idea whether such new capabilities or use cases will keep showing up in a couple of years? Or how confident can you be that the current use cases can carry the day even if novel use cases don’t show up in a year or two?

You see this whole depreciation debate is much more of a technological question than a boring accounting question and I suspect it’s nearly impossible to have a very high conviction long-term view on this topic from the outside. If compute buyers keep finding use cases that far exceed the cost for compute, demand will outweigh supply and compute prices can remain high to the extent that hyperscalers depreciating the GPUs at a 4-5 year timeframe may end up underreporting their earnings power in the next few years. Of course, the opposite could also happen if compute customers struggle to find valuable use cases with their compute. To be precise, not only the investors, but I think even compute sellers are not in a great position to have high conviction view about long-term depreciation schedule for the GPUs. Compute buyers, on the other hand, probably have a marginally better idea given they’re the ones who will have to extract value from these compute but even in this case, I don’t think they quite know the shape of the demand curve with high conviction in 3-5 years.

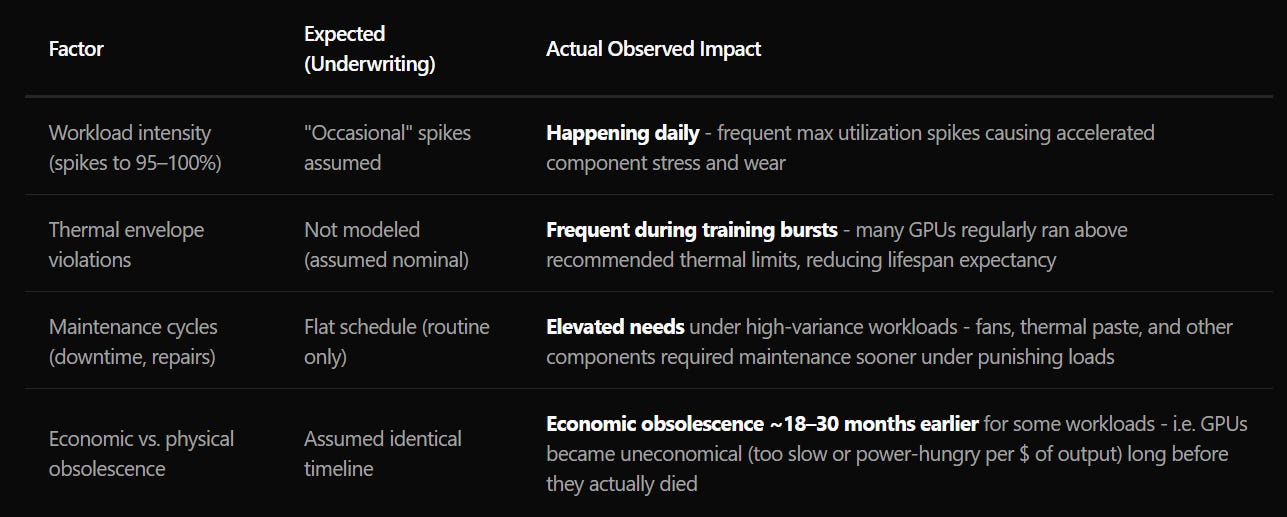

One additional complexity here is that the depreciation of these GPUs may vary a lot in different hyperscalers/neoclouds. While traditional CPU is much more standardized and likely have less variability in depreciation curve among different providers, the use cases in GPUs are still somewhat nascent and different providers can end up with vastly different actual useful lives of these GPUs. For example, this blog points out several factors that can swing the depreciation rate of such GPUs and based on telemetry data, they found the following: “The fleet's effective depreciation curve varied by 30–45% across different end-customers, even though the GPUs were identical model”

Speaking of the shape of compute curve, John Arnold, who sits at Meta’s board, had a bit of a provocative tweet a couple of weeks ago:

Most of the SpaceX neocloud analysis changes dramatically if you understand that there's a backwardated curve for compute today.

— John Arnold (@johnarnold) June 15, 2026

For the uninitiated, a market is backwardated when the spot price sits above forward prices i.e. the thing is scarce and expensive right now, and the curve slopes down because everyone expects it cheaper later. Saying compute is backwardated means a unit of GPU capacity rents at a steep premium today because of the power/chip/packaging crunch, while the forward curve is lower because the market expects supply to catch up and performance-per-dollar to keep improving.

But wait a minute…if that’s what one of the board of directors thinks the shape of the curve for compute to be, why is Mark Zuckerberg buying compute hand over fist today? While that may seem contradictory at first glance, I think there may be less tension between these positions than one may think.

Backwardation is a statement about the price of renting compute, and about the risk to a compute merchant, but not about the value of compute to a compute consumer who turns it into something else. Meta isn’t obviously earning the rental rate on its GPUs and it earns ad dollars, engagement, and model capability with the compute capacity it is building/renting. So, while the curve tells you merchant economics may deteriorate especially if the price falls faster than expected; it says almost nothing about whether a compute consumer should build for its own use. Again, one customer’s failure to utilize compute may not also mean disaster for the entire compute market either. When xAI failed to utilize their compute capacity, they could sell it to Anthropic and Google because those compute buyers can get presumably value from the compute capacity higher than what they’re paying for such capacity. Meta may be forced to do the same if their ambition in staying closer to the frontier model falls apart. Of course, the true disaster in compute prices will happen only when other potential buyers (OpenAI/Anthropic/Google) either run out of ideas to utilize such capacity or already have enough capacity to serve their users or build the next model. While these scenarios feel very unlikely today, I am not sure you can be VERY confident about the shape of the curve in a 3-5 year timeframe.

Arnold made his money in trading energy and at one point, he was actually the youngest Billionaire in the US. In Arnold's own native language: “convenience yield” can also play a huge role in determining whether a compute buyer such as Meta should buy compute today or wait for prices to come down. A curve inverts into backwardation precisely when holding the physical thing now commands a premium. The only question is whether your private convenience yield beats that premium. "Wait and accumulate later" only works if the returns to compute aren't time-sensitive. AI, especially in consumer land, is potentially a winner-take-most race, and ceding two years of ad gains, model quality, and engagement to Google and OpenAI to save on input cost is likely a catastrophic trade. The savings can be completely dwarfed by the returns forgone. Of course, it also doesn’t help that power, land, interconnects, and GPU allocations have multi-year lead times. If you wait, you will just start the queue late.

It is also worth recalling how Arnold made his name. In 2006, Amaranth’s star trader Brian Hunter sat on a massive, highly leveraged position in natural gas calendar spreads. The 2005 hurricanes had made him a hero, and by 2006 he was running a book so large that Amaranth reportedly controlled something like 70% of the open interest in certain contracts. Arnold’s read was different. I dredge this up because it is perhaps the same muscle at work when he’s looking at the compute market today. Hunter bet a scarcity spread would persist; Arnold bet that supply and seasonality would reassert themselves and the curve would mean-revert and indeed, it did. I guess it’s the same instinct sitting behind a throwaway line about compute being backwardated: a man who got rich fading one-sided positioning in an energy curve, now staring at a market where the entire crowd leans the same way on “demand outstrips supply forever.” The only problem here is I think the question about shape of demand-supply curve here is much more of a technological one than it perhaps ever was for natural gas in 2000s and answering that question may be above Arnold’s (or anyone’s) paygrade sitting in mid-2026!

Subscribers get the daily journal and five+ years of Deep Dives, i.e. full-length analyses with financial models on 65+ companies. The daily is just how I think out loud between the Deep Dives!

Disclaimer: All posts on “MBI Deep Dives” are for informational purposes only. This is NOT a recommendation to buy or sell securities discussed. Please do your own work before investing your money.