Some Notes from Spotify's 2026 Investor Day

Spotify held its third Investor Day in May, eight years after the 2018 debut that asked whether it could win against the big tech walled gardens with their own music streaming offerings, and four years after the 2022 edition that asked whether it could ever be a real business with real margins. The answer to both, with the benefit of hindsight, is "yes, and then some."

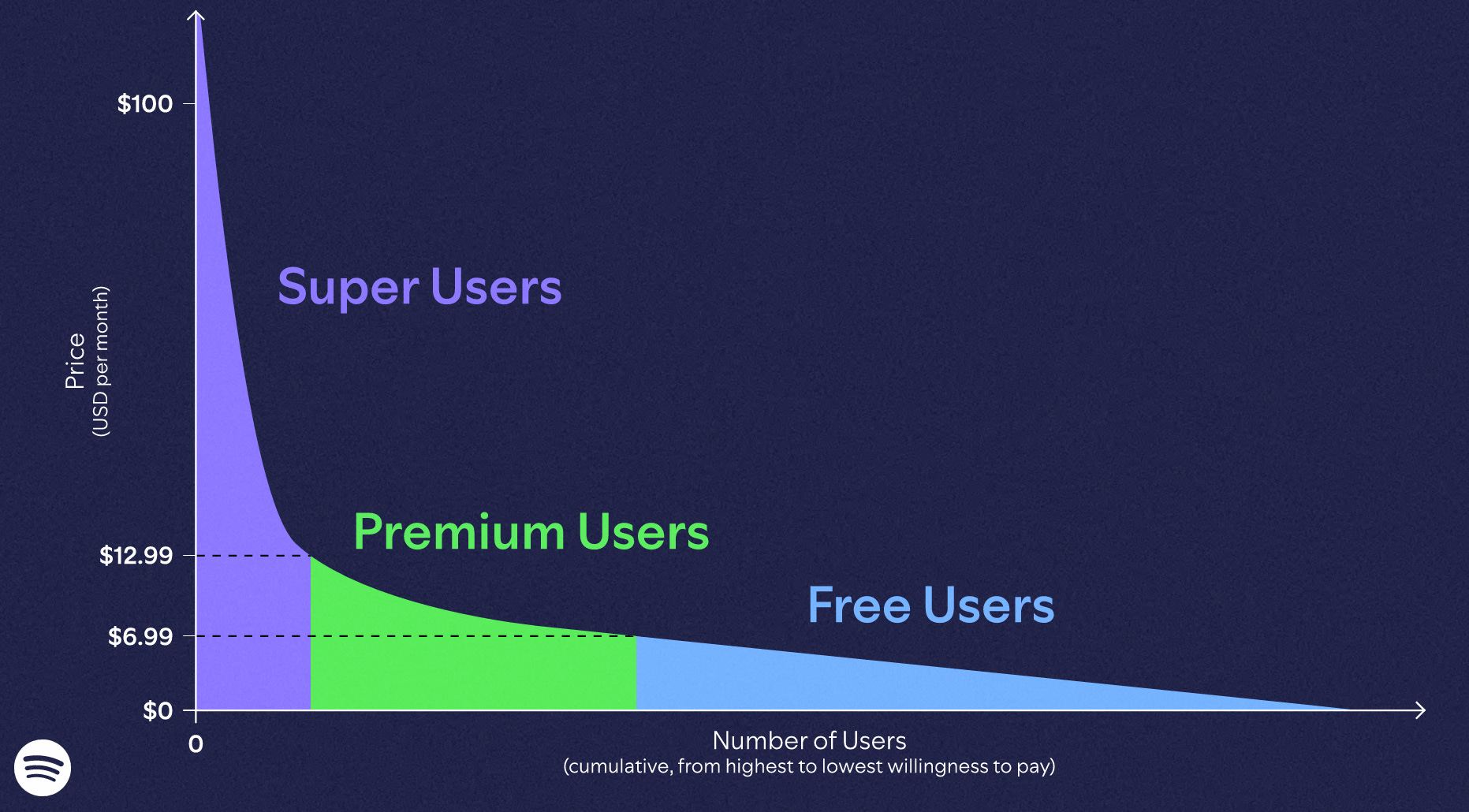

Spotify’s number looks pretty impressive: 761 million monthly users across 184 markets, nearly 300 million of them paying subscribers, and more than half a billion people now streaming audiobooks or podcasts on top of music! Management had an interesting framing that it kept returning to during the investor day: there is no such thing as an average user. Engagement and willingness-to-pay follow a power law, and Spotify has historically monetized only two slices of that curve i.e. the ad-supported long tail and a flat-ARPU Premium tier. Spotify now thinks that the head of the curve, the super-fans, is finally about to get monetized too.

The proof of concept is Audiobooks. When audiobooks rolled into Premium across the first 22 markets, a cohort of heavy listeners kept hitting their monthly hour caps which is a pretty strong demand signal. Spotify sold them more hours as an add-on, and in under a year more than a million users are paying for Audiobooks+ on top of their subscription. Their lifetime value (LTV) runs at multiples of Premium-only subscribers, and the add-on should cross EUR 100 million in annualized recurring revenue this July. For two decades, you could argue one of the concerning bear cases for Spotify was that it has a capped ARPU since there is a limit how much they can raise price, especially when there are competing products available with pretty much the same content as Spotify. What management now describes is a portfolio of higher-ARPU products…each with a smaller TAM but far higher revenue per user, layered on top of 300 million premium subscribers. Audiobooks got there first, but it sounds like they will keep releasing new products/features to monetize the head of the curve.

What gives Spotify’s ambition credibility is the country-by-country evidence Spotify walked through. In Sweden, the oldest market, paid penetration is now approaching 50% of the entire population which gives you an indication where a mature Spotify market can eventually land. In the US and Canada, the share of users paying for Premium has gone from 32% a decade ago to 60% today; MIDiA data has Spotify gaining US premium share every single year for six years “without exception.” Brazil doubled its conversion rate from 22% in 2016 to 44% today, a 27x increase in subscribers and revenue there is set to grow more than 30% this year. India is the long tail of the long tail: the subscriber count is now seven times what it was at the last Investor Day, net adds in 2025 ran three times the 2022 pace, and fewer than 10% of Indian users are on Premium. Across different geographies, Spotify’s playbook is the same: attract, engage, convert, retain, then grow ARPU.

On the supply side, the marketplace story still hasn’t lost steam: the gross-profit contribution from Spotify’s artist promotional tools has grown 4x since 2021, and it is a meaningful part of why music gross margin keeps grinding higher.

Speaking of supply side, the highlight was a landmark licensing agreement with Universal Music Group and Universal Music Publishing Group. Fans will be able to legally create covers and remixes from participating artists’ catalogs, with both the artist and the songwriter sharing in the value created. Most AI music to date has been net-new content that competes with the catalog; this instead monetizes the catalog by letting fans riff on it. Spotify management mentioned that a song that today might inspire three remixes and five covers could become 10,000 or 100,000 fan creations “paying tribute” to the original. Creation will be a Premium add-on but consumption stays free for everyone. How about the economics? This is what Spotify management said (emphasis mine):

“We don't want to go into the economics, but you should expect this to be at least margin neutral to accretive for us. We just don't do deals that are bad for any of us, which is one of the reasons why we spent so much time on getting these deals right.”

I would also note that Spotify did not need every label to launch this product which bodes well for their bargaining power here. I would actually be surprised if other labels didn’t follow suit soon.

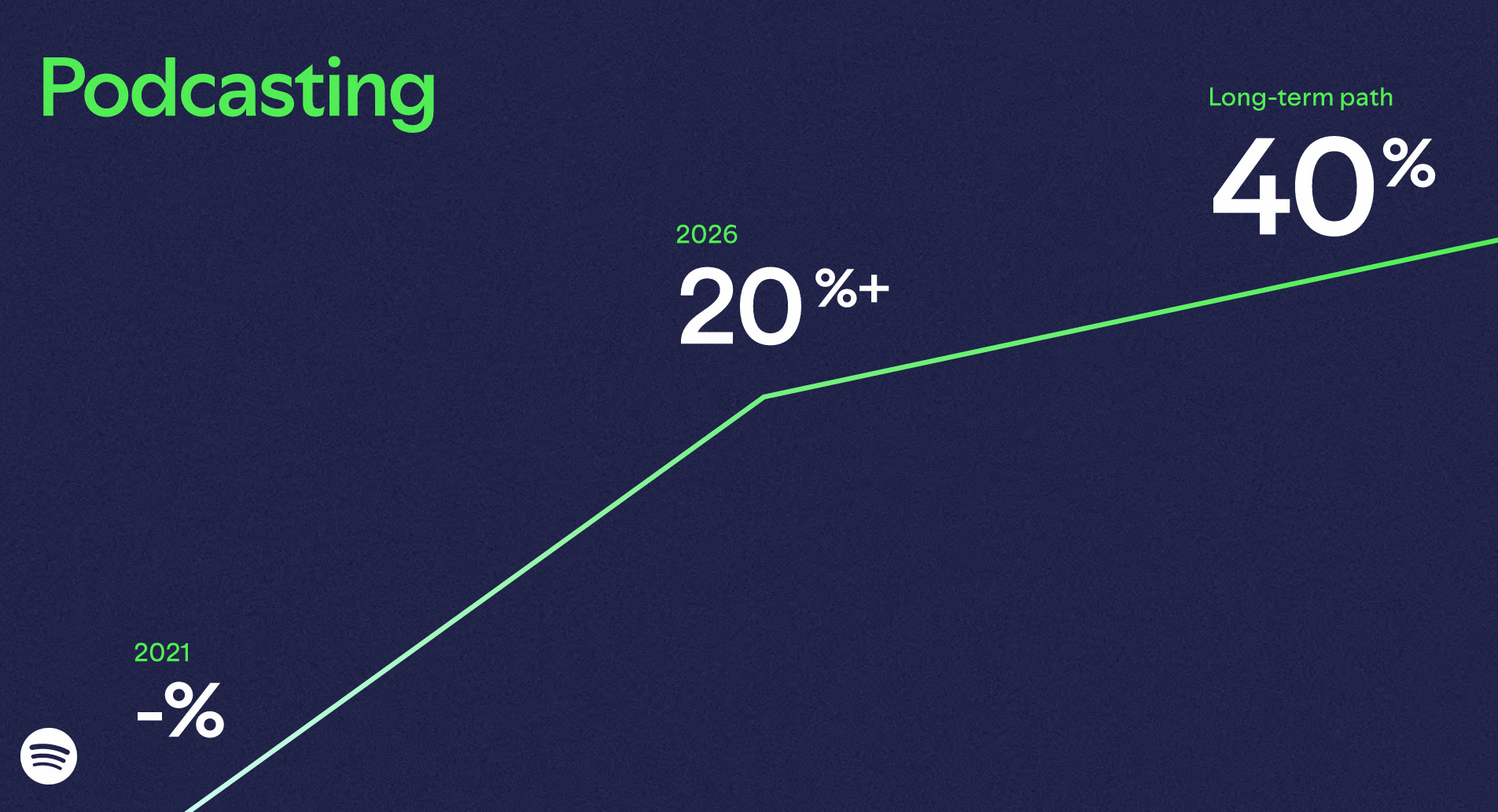

Podcasts are in their second year of gross profitability with engagement doubled since 2022, sponsorships up over 100% YoY, and a potential path to 40% long-term gross margins. Audiobooks, only two years old, grew listening hours 60% from 2024 to 2025, expanded the indie catalog 50%, and now reach a meaningfully younger, roughly 50/50 male-female audience. Page Match, which lets users flip between a print book and the audiobook, is driving up to 55% more listening.

Of course, AI was a recurring topic. Spotify highlighted again that it is building a “Large Taste Model” trained on 3.4 trillion daily data points (behavior, metadata, creator and cultural signals) that no one else can replicate, because taste requires an insanely active user base for years. The payoff is twofold: better personalization and entirely new products.

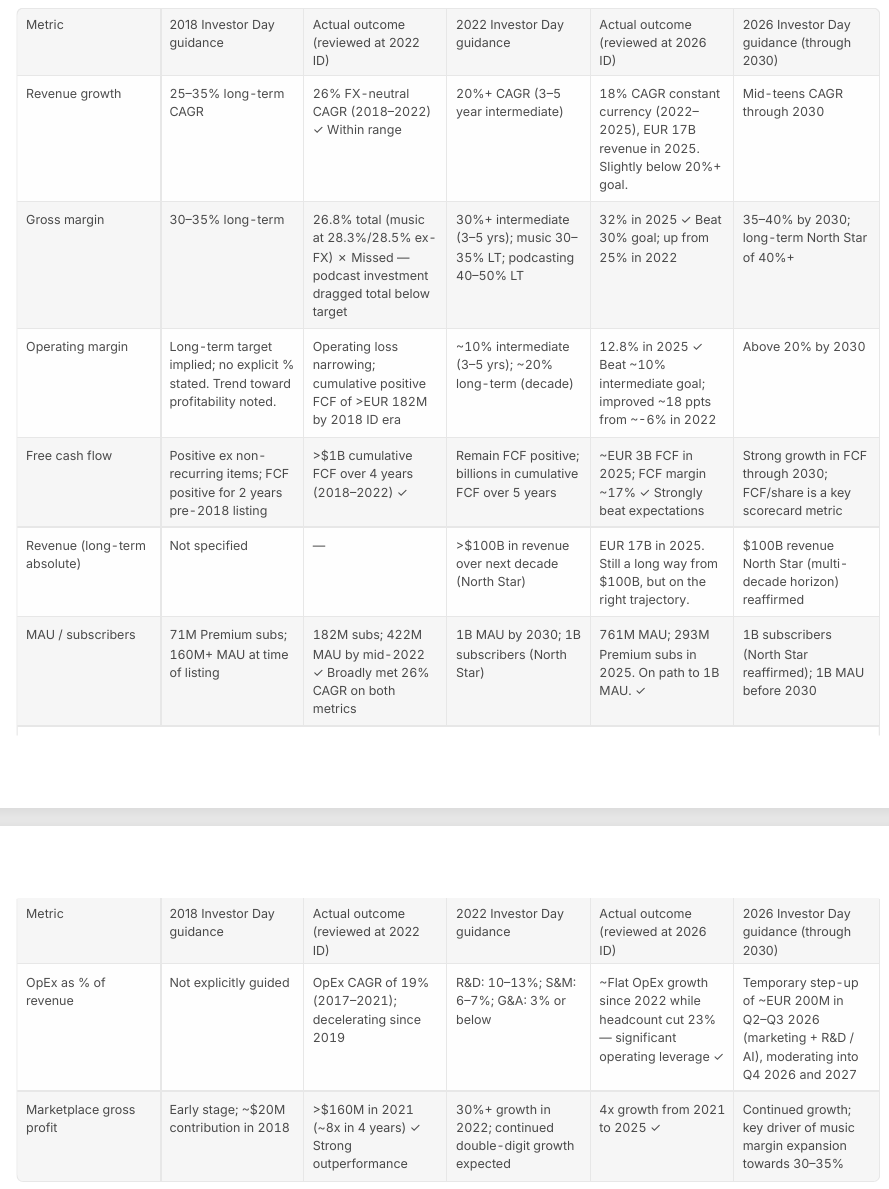

Let’s talk about the outlook now. I thought it would be useful to take a closer look at what Spotify promised in the 2018 and 2022 Investor Day and what they actually delivered.

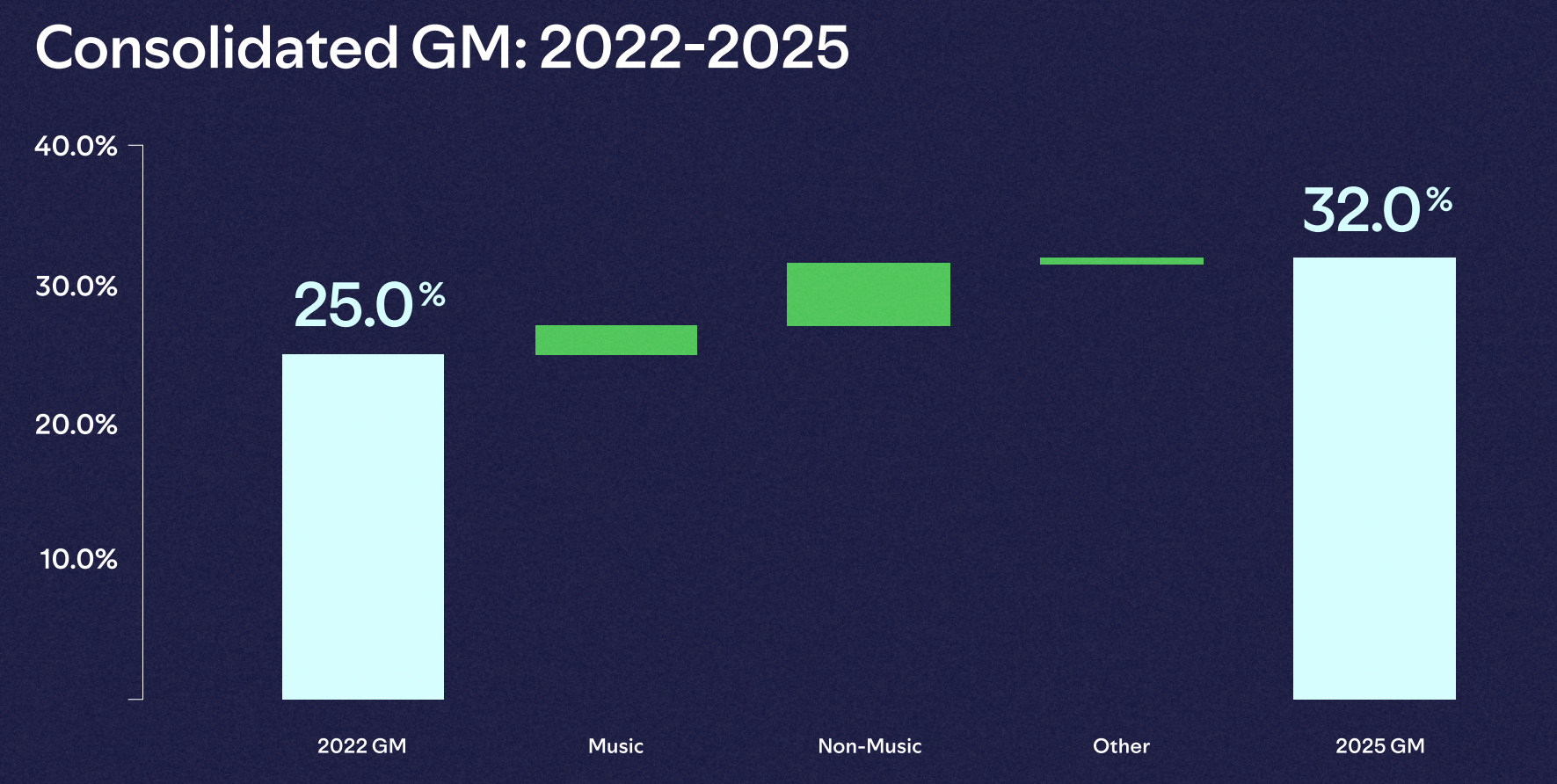

In 2018, Spotify guided to a 25-35% long-term revenue CAGR and a 30-35% gross margin. It largely hit the growth target but missed gross margin as podcast losses dragged the blended number down. In 2022, the bar moved to 20%+ revenue growth, an eventual ~20% operating margin, a $100 billion revenue North Star and a billion users; by 2025 it had delivered an 18% currency-neutral CAGR to EUR 17 billion, 32% gross margin (versus the 30% goal), 12.8% operating margin (versus the ~10% intermediate goal), and ~EUR 3 billion of free cash flow off a 2022 base of roughly zero. As alluded earlier, during the 2022 Investor Day, the dominant concern from investors was that Spotify may be a great product but may be a terrible business given the company was beholden to its suppliers and hardly ever made money. Even the bulls (including me) got deeply annoyed that Daniel Ek mentioned the fables of 100 Billion revenue “over the next decade”. Thankfully, the new co-CEOs seem to be more self-aware and dropped the “over the next decade” framing when it comes to 100 Billion revenue.

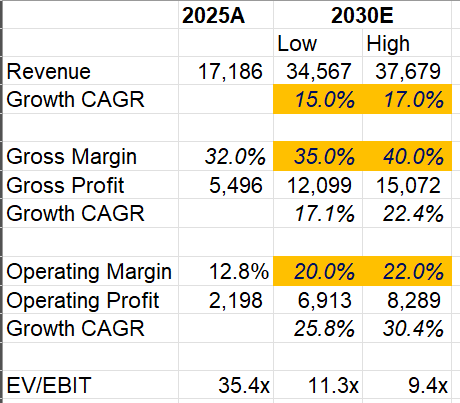

For 2030, the new frame is a mid-teens revenue CAGR, a 35-40% gross margin, an operating margin above 20%, and strong FCF growth, with the $100 billion revenue and 1 billion subscriber North Stars reaffirmed. I have asked Claude to make a table that includes 2018 and 2022 targets and actual results as well as 2026 investor day outlook by different metrics which is shown below:

So what are you paying for it? Take revenue from EUR 17.2 billion to EUR 34.6-37.7 billion by 2030 at a 15-17% CAGR (vs consensus at EUR 31.4 Billion in 2030); hold gross margin at the guided 35-40% and operating margin at 20-22%, and you get 2030 operating profit somewhere between EUR 6.9 billion and EUR 8.3 billion (vs consensus of 6.2 Billion for 2030) which is 26-30% CAGR over five-year period. Against the current enterprise value, the stock trades at about ~35x 2025 EBIT, but looks far more palatable if they can deliver in the next five years what they have guided during the Investor Day.

The numbers looks interesting enough that I will take the time today to update my full Spotify model. I will share the model and some further thoughts on Spotify’s valuation tomorrow.

Subscribers get the daily journal and five+ years of Deep Dives, i.e. full-length analyses with financial models on 65+ companies. The daily is just how I think out loud between the Deep Dives!

Current Portfolio

Please note that these are NOT my recommendation to buy/sell these securities, but just disclosure from my end so that you can assess potential biases that I may have because of my own personal portfolio holdings. Always consider my write-up my personal investing journal and never forget my objectives, risk tolerance, and constraints may have no resemblance to yours.

My current portfolio is disclosed below: