"Serious" Era of Software Investing

A couple of weeks ago, Redpoint published an interesting presentation on the state of software industry. It’s a good recap of what has been going on in both the public and private software market.

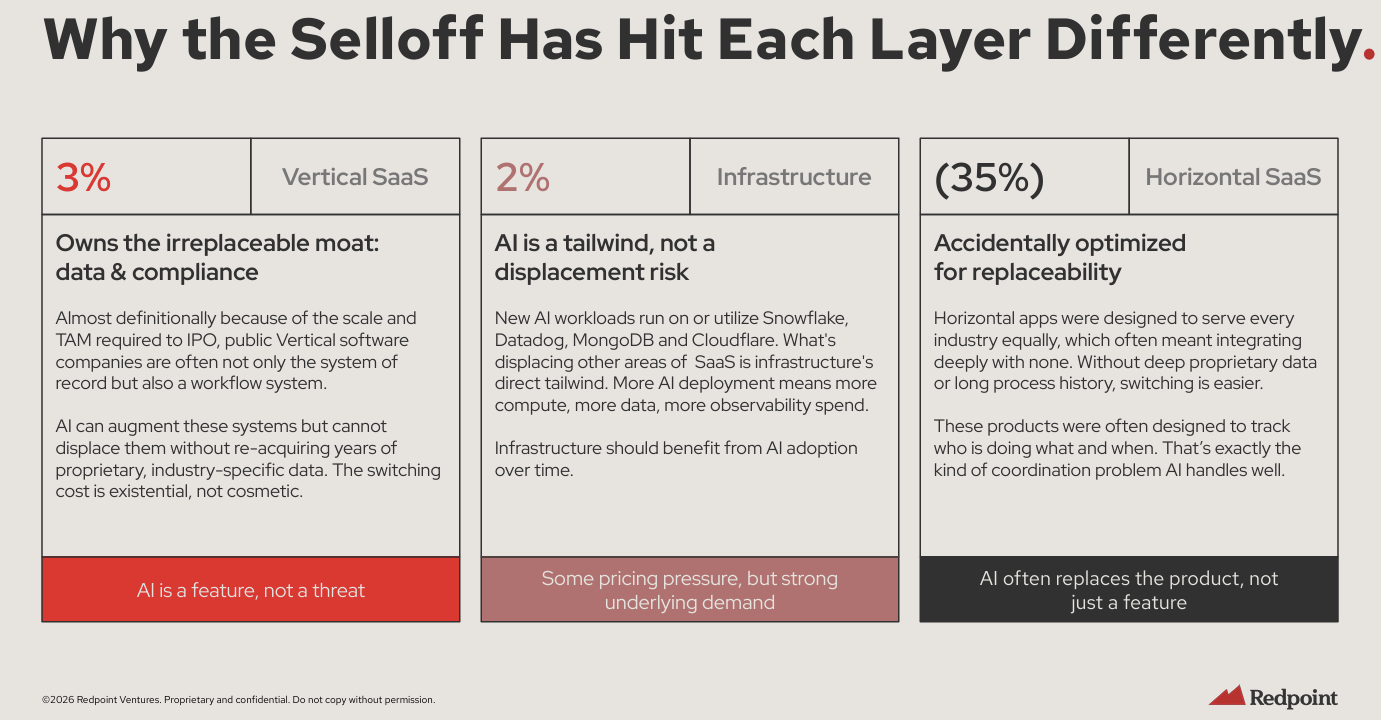

Redpoint pointed out that the SaaS selloff in the last 12 months hasn't been indiscriminate. It's been almost a rational sorting of software by defensibility against AI. Vertical SaaS has held up the best because these companies own irreplaceable moats in proprietary, industry-specific data and compliance workflows; AI can augment them but can't displace decades of accumulated system-of-record data, making the switching cost existential in nature. Infrastructure software also held up just fine because AI is a direct tailwind: more AI deployment means more compute, data, and observability spend flowing to names like Snowflake, Datadog, MongoDB, and Cloudflare. Horizontal SaaS, by contrast, has been crushed because these products were “designed to serve every industry equally, which often meant integrating deeply with none” and their core function of tracking who does what and when is precisely the coordination problem AI handles natively. Market is basically saying today that while in vertical software AI is a feature and in infrastructure it's a demand driver, in horizontal SaaS it's a substitute for the product itself.

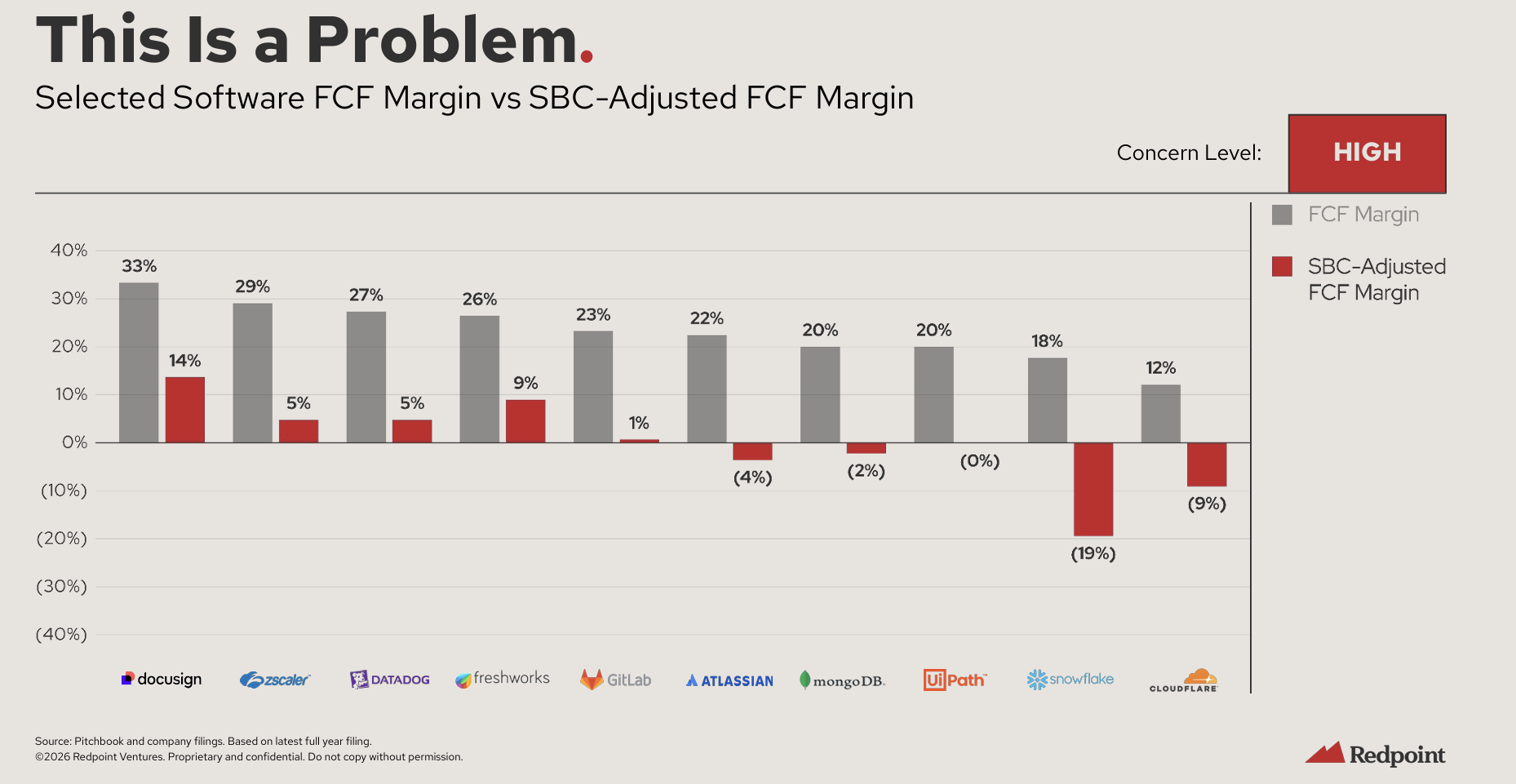

One of the problems Redpoint identified is excessive stock based compensation (SBC) in software industry. As I have often pointed out, SBC itself is hardly a problem. However, it is the deliberate decision of ignoring SBC by investors where lies the key challenge. If investors are okay with valuing a company by ignoring very real costs, management has every incentive to give what investors want. As a result, I have hardly felt any sustained annoyance at tech management for excessive SBC; rather I have been utterly confused why there is a plethora of investors who are overly eager to value companies by ignoring these costs and often seem very willing to propagate inane talking points such as “SBC won’t make or break a company; Accelerate revenue or die”. Of course, a company won’t live or die because of SBC but an investor who wants to compound his or her hard earned savings over years to come cannot possibly ignore these costs while valuing these companies.

I’m not singling out Redpoint; even a16z recently published a think piece outlining their advice for software companies. Notice the following (emphasis mine):

Software companies got very good at talking about free cash flow margins over the last decade. But if we are serious, we should stop excluding stock comp and pretending dilution is not an expense borne by owners. For companies that are not about to reaccelerate growth, I think the right target is 40% or even 50%+ true operating margins, including SBC, within 12-24 months.

“If we are serious”? I guess it makes sense to ignore SBC if you were not being “serious” until the falling stock prices finally forced you to think through some basics. So anytime I hear VCs talk about software’s SBC problem, I cannot help but think about this meme: “we’re all trying to find the guy who did this”. To be clear, public market tech investors also are equally to be blamed. It is still astonishing to me that almost all the data providers ignore SBC for software companies (unless you’re big tech) in their forward estimates which makes much of the forward valuation multiples below Gross Profit completely meaningless.

Given this context, I also cannot help but wonder whether VC investors are still currently in “non-serious” stage of evaluating AI companies and perhaps they will discover the obvious problems of quoting ARR multiples on companies whose revenues are neither necessarily recurring nor are blessed with zero marginal cost. The reason it made at least some sense to look at revenue multiple for loss making software companies in the past is because of the near zero marginal cost which led to somewhere between 70% and 90% gross margin. That is almost certainly not the case in any of the AI native startups and somehow this obvious flaw is currently being largely ignored by VCs who keep quoting ARR multiples. The reality is this is not a VC specific problem; this inertia to update your opinions or ignoring obvious realities is primarily a feature of “zero volatility” nature of these investments. Even in public market, investors are often found to ignore obvious risks until stock price starts going down and then the same investors discover the risks they should have been thinking all along. Yours truly also falls for this classic problem every once in a while and unlike in VC world, public market investors are not afforded to dwell on their cozy, but apocryphal consensus for too long!

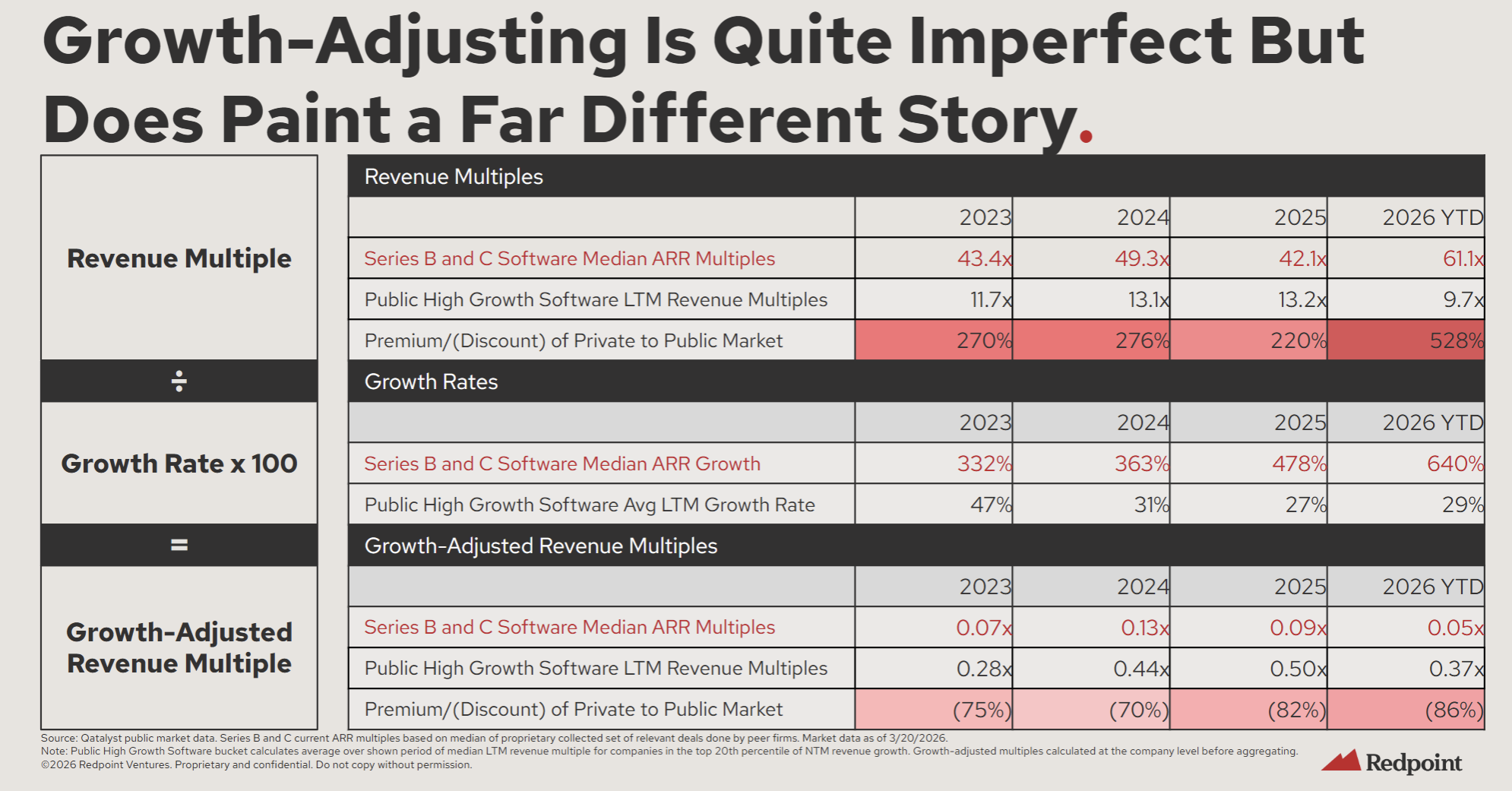

Redpoint mentioned that once you adjust for growth in private companies, the valuation discrepancy between public and private market software companies not only disappear but you can argue private companies are trading at a substantial discount!

To be fair, they did say these adjustments are “quite imperfect”, but apart from the obvious limitations pointed earlier of using ARR multiples for these private software companies, I thought Akram had a very good response why this comparison is largely non-sensical. Some excerpts from Akram’s counter (emphasis mine):

“…no more growth adjusted comp slides to public mature names plz, which is for some reason happening way more. Series B/C companies trading at 61x ARR but growing 640%, giving a growth-adjusted multiple of 0.05x vs. public software at 0.37x is cool but this completely ignores that a Series B company growing 640% off a $3M ARR base faces entirely different scaling physics than a public company growing 29% off a $5B base. The growth rate convexity at small revenue bases is almost free. You close three enterprise deals and you’ve tripled. That 640% growth rate is a description of being small, not evidence of anything beyond that yet really.

The efficiency slide though is where the real debate should be. Cursor at $6.1M ARR/FTE and Lovable at $3.4M are being framed as “unprecedented software efficiency.” But that ARR/FTE ratio is many ways just a description of how thin the product layer is for these companies. If you have 50 people and $300M ARR because you’re reselling Claude with a great IDE wrapper, are you operationally excellent vs atlassian/servicenow or really just a thinner biz? You could argue these metrics are a reflection of how little proprietary value-add sits between the customer and the foundation model API’s. Today, that looks awesome, but can in fact be EVEN WORSE then the very software 1.0’s who have TERMINAL VALUE questions now.”

Indeed, I still haven’t heard a compelling explanation why all the terminal value question for public software companies isn’t doubly applicable for private AI-native software companies. My best explanation is since these private companies are inherently “zero volatility” assets and the investors know much of the potential buyers in the private market agree to the idea of valuing these companies based on ARR, the VCs can leave the terminal value question for later round and “hopefully” for public market investors.

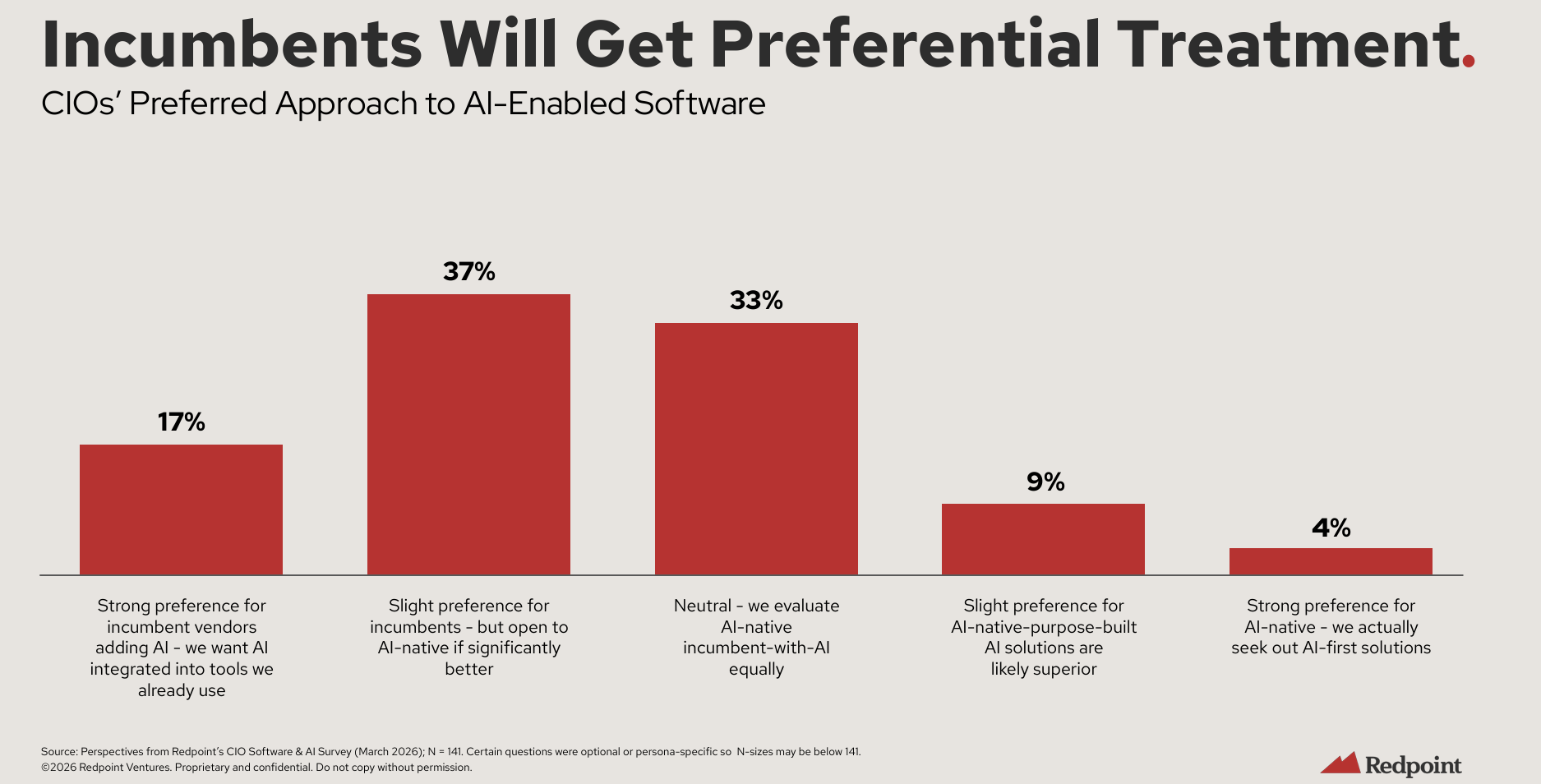

Perhaps one of the more intriguing slides from Redpoint’s presentation is that they pointed out incumbent software companies are likely to get preferential treatment from their customers as these customers start adopting AI in their workflows. Indeed, this is why I believe for many incumbent software companies, they still have a decent shot at controlling their destiny.

Unfortunately, the limit to such optimism is more intangible realities in any large incumbents: culture. I too am quite sympathetic to this argument and suspect this is where indeed the game will be won and lost between incumbents and startups in the next three to five years!

In addition to “Daily Dose” (yes, DAILY) like this, MBI Deep Dives publishes one Deep Dive on a publicly listed company every month. You can find all the 67 Deep Dives here.

Current Portfolio:

Please note that these are NOT my recommendation to buy/sell these securities, but just disclosure from my end so that you can assess potential biases that I may have because of my own personal portfolio holdings. Always consider my write-up my personal investing journal and never forget my objectives, risk tolerance, and constraints may have no resemblance to yours.

My current portfolio is disclosed below: