Survival of the Fastest

More than a decade ago, Peter Thiel wrote:

“Monopolists lie to protect themselves. They know that bragging about their great monopoly invites being audited, scrutinized and attacked. Since they very much want their monopoly profits to continue unmolested, they tend to do whatever they can to conceal their monopoly—usually by exaggerating the power of their (nonexistent) competition.

Non-monopolists tell the opposite lie: "We're in a league of our own."

Nvidia doesn’t quite fit that description. For all intents and purposes, they are indeed a monopoly in general purpose computing, but it is so obvious that the competitors are deeply incentivized to come up with an alternative to GPUs that Jensen Huang doesn’t even bother to “lie” as a monopoly and rather spent much more time in this year’s GTC to establish that Nvidia is in a league of their own. It’s not hard to believe Huang because many of the companies who are trying to offer competing chips are also the same ones ordering tens of billions of chips from Nvidia every quarter!

Investors, however, still feel nervous about Nvidia’s lofty gross and operating margins. Can such margins be sustainable? Huang went gung ho yesterday during analyst Q&A to defend his margins. From the Q&A session yesterday:

“Every CEO of every cloud service provider, I would challenge them all to go and create that chart for themselves. And I’ll help them. And you pick your favorite other configuration, third-party chips, built your own chips, and you put it into that model faithfully and then you can decide would you like to have higher revenues or lower. Would you like to have higher ASPs or lower, would you like higher margins or lower because that’s all it means.

Look, TSMC’s wafers are the highest in the world, but they’re the best value in the world. And I gladly pay for it. And so the idea ASML systems are the most expensive in the world, they’re worth it. There’s no question about it. And so the question is simply, do you want to make more money? Or do you want to buy the lowest cost equipment? Do you want to make more money? Or do you want to buy the lowest cost equipment? That’s the difference. Now what I just said is a new concept, and I think we can all acknowledge that. I just treated a computer system. The way I treat TSMC chip factory, the way I treat ASML manufacturing equipment. And that’s not the way people thought about it in the past if I have 2 CPUs, 1 of them is 256 cores, the other 1 is 256 cores. Tell me which one is the better one. Well, the cheaper one’s the better one because I’m running it by the core anyways. But that’s not the way tokens are created.

You don’t rent by the core, you monetize by the tokens per second. And so it’s a different economic. Does it make sense? You’re not renting cores, you’re not renting nodes. You’re producing tokens, which is the reason why everything changed. It was necessary to make sure that everybody understands the economics of the new world. They’re trying to buy the lowest equipment, lowest cost equipment. My equipment costs 30% cheaper. What does that mean to your factory? What does that mean to your factory? That’s really the question. And so I think people -- anybody who says my chips are 50% cheaper. Put that in the context of the factory, and that person is actually demonstrating to you they don’t understand AI.”

It’s important to internalize Huang’s point of view here. He is well aware of the margins he is making and how emboldened his competitors/customers must feel to get off the Nvidia tax, but he is highlighting the fact that as long as Nvidia’s chips are superior in producing lowest-cost tokens, the math can remain decidedly in Nvidia’s favor, especially since tokens can skyrocket with the rise of agents. From Huang’s prepared remarks:

“…the price of the computer and the cost of the token are only marginally related.

Remember, people are buying these computers to produce tokens. The effectiveness of the production of those tokens matter greatly. They’re not reselling the computer. If you bought a computer and it’s expensive, if you resold it and that’s it, then it’s expensive. But you bought a computer and it’s expensive because the technology is incredible, but it produces tokens at such incredible rates, you have -- simultaneously have purchased the most expensive computer and produce the lowest-cost tokens.

Huang’s point is well taken; however, I think the reason Huang is so happy to pay TSMC and ASML’s margins because he is at least so far able to defend his own margins. His own customers i.e. hyperscalers may be grappling with a different reality. I asked Gemini to show me an illustrative example how $100 sales by ASML used to flow through the compute value chain to hyperscalers ten years ago.

I then asked Gemini to do the same illustrative analysis for the compute value chain today.

As you can see, the economic multiplier from a $100 piece of ASML equipment to a hyperscalers' end revenue shrank by more than half (from ~618x down to ~285x), illustrating how value capture has concentrated upstream. Just a quick look at the evolution of gross margin of the players in the upstream makes it quite apparent of their increased ability to capture value. Hyperscalers also did pretty well over the last decade because given their fragmented customer base and oligopolistic industry structure, they too were able to live in a cozy manner.

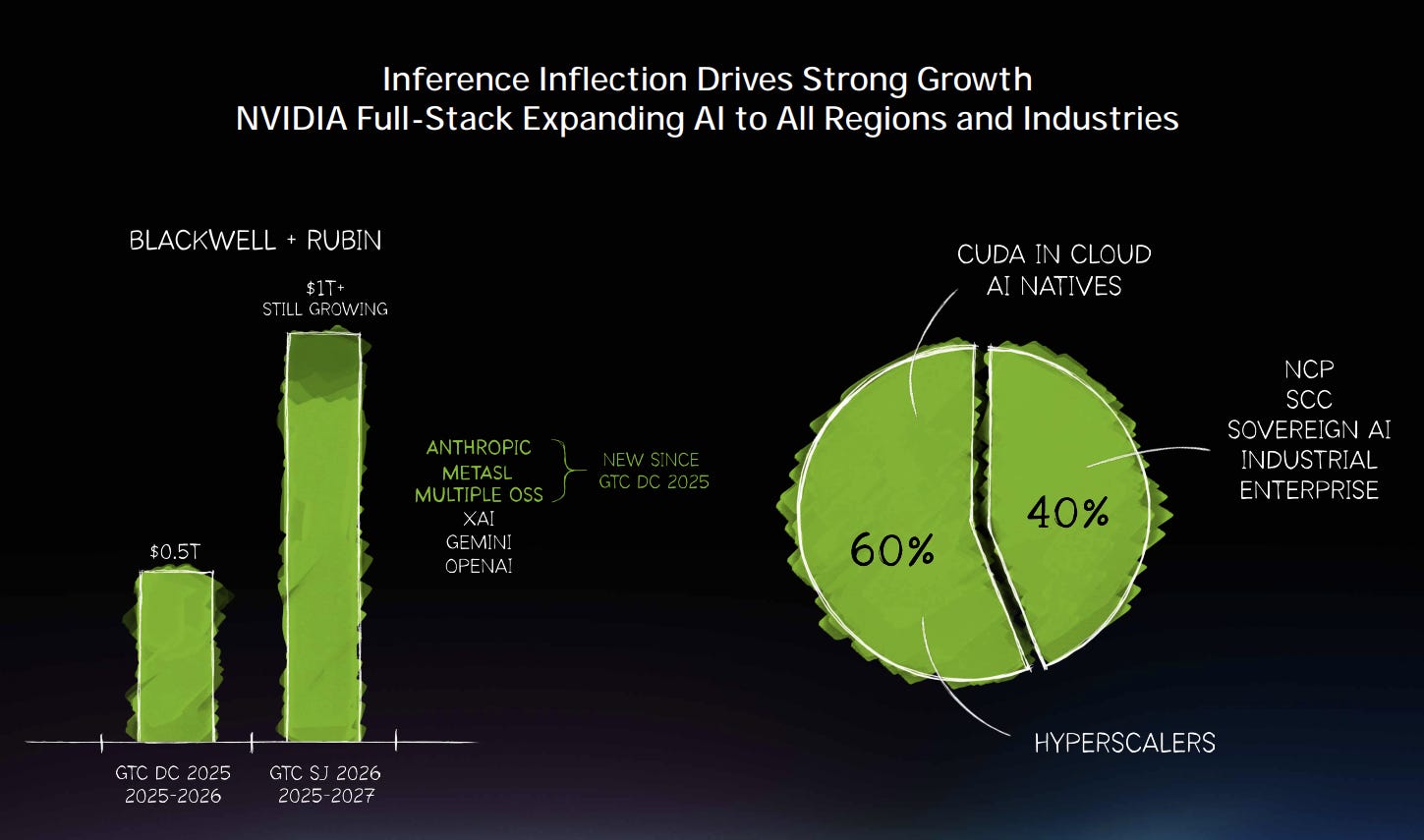

Unfortunately, Huang seems pretty determined to disrupt such coziness of his customers who are also trying to compete against Nvidia. At one point during the Q&A yesterday, one analyst pointed out that while hyperscalers account for 60% of datacenter revenue, these hyperscalers also currently account for majority of neocloud’s revenues. So, in a sense, the hyperscalers may actually account for ~80% of data center revenue. Huang in his response alluded which customers he would like to see thrive more:

“Even in the cloud, we compete with some part, but we also bring customers to the other part. And so some part of that chart of 60%, we have to compete. And our job is just to deliver that chart better than anybody else in the world, and we’re doing very, very well, and we’re actually increasing our position day in and day out. And then the other part, we bring customers to them. They’re just grateful.

…I think if you test against, do they design the -- do we -- does NVIDIA compete with them on chips?…then you got to figure out where are we in our position and what’s our opportunity and so on and so forth. I don’t think OCI will design their own chips. I don’t think it’s sensible for them to do it. Obviously, CoreWeave’s not going to design their own chips. And so there, we -- so where do we compete and where do we bring the cloud service provider customers? And their cloud revenues, a lot of them, a lot -- a big part of it, obviously, I nearly 100% of that is because of NVIDIA”

In fact, Nvidia mentioned they expect to utilize half of their FCF to buyback shares and use the other half to fund their “ecosystem”. Since Huang indicated before at MS TMT conference that they are unlikely to participate in Anthropic and OpenAI’s funding going forward (since they may IPO this year), majority of the rest of its FCF post buyback may go to funding neoclouds to ensure AI workloads become much more fragmented than traditional cloud workloads ever were. Just for context, Nvidia is expected to generate almost $700 Billion cumulative FCF in just the next three years. So even if ~25% of this FCF goes to neocloud, that’s $175 Billion potential funding to neoclouds. Let me also highlight that such circular financing is also what makes valuing Nvidia increasingly challenging for me given this capital allocation policy isn't just one-off, rather structural in nature. How do I capitalize (and at what multiple) Nvidia’s earnings without having an opinion on the future of neoclouds? Nvidia looks cheap in earnings multiples, but half of the earnings goes to funding the ecosystem, you need to have an opinion on the valuation of the ecosystem itself to evaluate Nvidia’s capital allocation. I suspect that’s not an easy job for most investors, certainly not for me.

Nonetheless, I have no problem in admitting that Nvidia is running at a breakneck pace which will probably make it very, very difficult for its competitors to catch up with Nvidia in the near future. Huang with his strategic mind is reshaping the compute value chain to outmaneuver and outcompete everyone to protect his castle. A bet on Nvidia may be largely a bet on Jensen Huang which reminds me the following quote from him more than two decades ago:

Someone said recently that I’m the most tenacious CEO they’ve ever seen. I’m not exactly sure whether that’s a compliment or not, but my will to survive exceeds almost everybody else’s will to kill me.”

Perhaps the most admirable quality of Jensen Huang is his ability to maintain the raw desire for survival even when his company is literally the largest company in the world! 🫡

In addition to “Daily Dose” (yes, DAILY) like this, MBI Deep Dives publishes one Deep Dive on a publicly listed company every month. You can find all the 66 Deep Dives here.

Current Portfolio:

Please note that these are NOT my recommendation to buy/sell these securities, but just disclosure from my end so that you can assess potential biases that I may have because of my own personal portfolio holdings. Always consider my write-up my personal investing journal and never forget my objectives, risk tolerance, and constraints may have no resemblance to yours.

My current portfolio is disclosed below: