Nvidia's Burgeoning Moats, Pichai's Comp

Jensen Huang mentioned at Morgan Stanley (MS) TMT Conference last week that Nvidia just reported “the single best print in the history of humanity”. While such glib comments attracted a lot of attention, I thought Huang’s session was quite instructive in explaining to investors how Huang is busy at work to enhance Nvidia’s moats. I will particularly highlight two comments from the session on this topic.

First, Huang’s point about Nvidia’s full-stack approach and why Nvidia is able to accelerate their launch schedule makes me increasingly pessimistic about most of the ASICs. From Jensen Huang:

“…we’re quite comfortable with this full stack, full system approach. And without being able to do that, it is impossible to stay at the bleeding edge. It is literally impossible to keep up with a company that’s building not just one chip each year, but we’re building an entire infrastructure each year because-- we own the CPU. We revolutionized the new way of designing CPUs, and you’ll see more examples of that. We revolutionized the way we do CPUs, revolutionized the way we obviously do GPUs, connect them together using this thing called NVLink, which revolutionized the way you build computers all together, connected together with a new type of AI Ethernet called Spectrum-X, we connected everything together. Now we own the entire stack. We know all the chips inside.

When you own the entire stack and you own all the chips inside, you could change it every single year. If you don’t own the entire stack and you don’t own all the chips, it’s hard to innovate every year. And the reason for that is because you’re connecting too many cats and dogs, and there’s too much innovation to pull together once a year if you can’t control it because it’s a full stack problem. So that’s how we got here.”

Second, while Nvidia’s moats related to CUDA is well understood by investors now, their procurement advantages is perhaps still underappreciated which I highlighted in my AWS piece a couple of days ago. Huang drove the point home even more clearly:

“I love constraints. And the reason for that is because in a world of constraint, you have no choice but to choose the best. You can't squander your choice. If the data centers -- if the land power and shell is constrained, you're not going to randomly put something in there just to try it out. You're going to put something that you know for certain is going to deliver the tokens per watt, that you know for certain is going to allow you -- from the moment you secure the capacity, we're going to be able to stand up an entire factory for you. We're the only company in the world that can come into your company and help you stand up an entire AI factory.

And this is one of those questions now for all the CEOs that are in the cloud -- they’re cloud service providers or software providers, if they make poor choices, this is no different than me choosing the wrong foundry. This is no different than me choosing the wrong memory, the wrong anything because I have so little -- everything is so constrained. If I choose poorly, my revenues are affected, everything is affected. And so they can’t choose poorly.

The second thing is NVIDIA is, as you mentioned, working at such a large scale. Our supply chain, one of the things that we do with our money, of course, is to secure our supply chain. One of the things that we do with our capital is to secure supply chain so that when Satya asked me to help them stand up a few gigawatts, the answer is no problem. And the reason for that is I got all the memories, I’ve got all the wafers, I got all the CoWoS. I’ve got all the packaging, I’ve got all the systems, I’ve got all the connectors, I got all the cables. Everything from copper to multilayer ceramic capacitors, everything is secured. That’s one of the reasons why NVIDIA’s balance sheet being strong is so strategic.

A strong balance sheet today is not only helpful, it’s strategic. And so you look at the amount of revenues we’re shipping into, just look backwards and look at the amount of supply chain capacity we had to go secure for that they have to believe. If you set up a factory, a plant -- a DRAM plant, and I come in and say, you know what, go ahead and set up the DRAM plant because I’m going to use it. That goes a long ways. You might as well take that to the bank, as many of them have. And so I think the fact that everything is scarce is fantastic for us.”

Indeed, as long as these scarcities continue, Nvidia likely remains very much in the pole position in the compute value chain and continues to rake profits higher than anyone else. The question, however, remains if we ever get to the other side of scarcity since betting on scarcity to last forever doesn’t seem like the most sensible bet. Perhaps by the time we will largely close the gap between demand and supply in compute, Huang with his “strategic” mind will figure out other ways to defend his castle.

In addition to “Daily Dose” (yes, DAILY) like this, MBI Deep Dives publishes one Deep Dive on a publicly listed company every month. You can find all the 66 Deep Dives here.

Sundar Pichai’s Comp

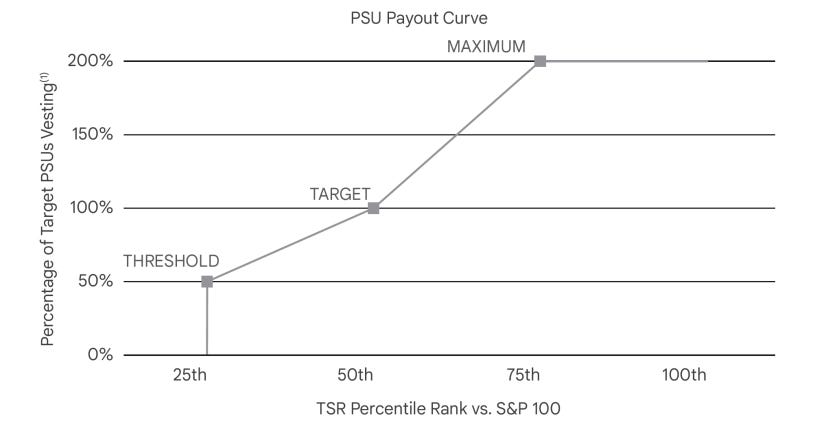

Sundar Pichai was awarded a new incentive comp by Alphabet board last week. Some components of Pichai’s comp is largely similar to what he was awarded before. For example, like his last comp, Pichai’s Performance Stock Units (PSU) will vest based on Alphabet stock’s performance against S&P 100. While they didn’t disclose the exact details of what Total Shareholder Return (TSR) Alphabet needs to hit relative to S&P 100, they will share those details following 1Q’26. For context, in his earlier comp, Pichai needed to hit 75 percentile or above to receive 200% of his target PSUs. My guess is it’s going to be quite similar again this year.

What is actually new this year is that Alphabet tied a big chunk of Pichai’s economics directly to later-stage Other Bets. At target, $175 million of Pichai’s comp package is tied to Waymo ($130 million) and Wing ($45 million); at max, that piece can be worth $350 million. Waymo/Wing awards use internal grant-date fair values for those subsidiaries’ common units which is not publicly disclosed. Given Waymo just raised $16 Billion last month at $126 Billion valuation, we can probably assume this as “fair value” at grant date for the Waymo piece. Wing, as far as I can tell, hasn’t raised external capital which means we don’t quite have much of an idea about the valuation of Wing. In any case, given that most Alphabet shareholders essentially capitalize “other bets” losses in their models, this is a welcome development that the CEO is directly paid for value creation of “Other Bets”. It does appear more and more “other bets” are gradually graduating from their “science experiments” phases and turning into a real standalone businesses.

Current Portfolio:

Please note that these are NOT my recommendation to buy/sell these securities, but just disclosure from my end so that you can assess potential biases that I may have because of my own personal portfolio holdings. Always consider my write-up my personal investing journal and never forget my objectives, risk tolerance, and constraints may have no resemblance to yours.

My current portfolio is disclosed below: