Man and Machine

For a typical company, analysts and investors evaluate a company’s capital allocation by looking at how the company allocates the cash it generates. Ultimately, there are only five things you can do with your cash flow from operations: a) invest in your own business to grow more in the future i.e. capex, b) acquire or invest in a different company, c) pay a cash dividend to shareholders, d) repurchase shares, and/or e) repay any debt.

However, assessing capital allocation is relatively lot easier for companies such as Floor & Decor than a big tech company such as Alphabet. Before AI made all the big tech companies (except Apple and Nvidia) materially capex intensive businesses, a good chunk of their actual capital allocation happened through the income statement rather than the balance sheet. Unfortunately, it is relatively more challenging to not only objectively segment growth opex vs maintenance opex but also evaluate the return on such investments on a regular basis. Nonetheless, for businesses such as Alphabet and Meta, I have long felt a better way to gauge about their capital allocation framework is to think from a gross profit level, rather than cash flow from operations (CFO) level.

For supermajority of the gross profit Meta or Alphabet generates in a typical year, it is unlikely to be driven by the opex associated with the current year. Of course, to compound the gross profit for years (or decades) to come, they must front load the opex investments which gets expensed as incurred but the benefits will likely be reflected in income statement often years after such opex investment. These benefits, however, are far from guaranteed (just look at Meta Reality Labs, for example). So, the variance in return from such opex investments through income statement is likely to be noticeably higher than return variance in capex investments through balance sheet. Nonetheless, that doesn’t invalidate the reality that there is a deep, qualitative difference in how a company such as Alphabet and Meta think capital allocation decisions compared to more plain vanilla businesses such as Floor & Decor.

The qualitative difference in capital allocation framework in companies such as Alphabet vs most other traditional businesses was quite apparent when John Collison asked Sundar Pichai about capital allocation questions in a recent Cheeky Pint episode. See the question from John Collison and excerpts from Sundar Pichai’s answer below (emphasis mine):

John Collison:

Can I ask, I’m curious, how capital allocation actually works at Google? What I mean by that is the idea good capital allocation is about internalizing the opportunity cost for capital and putting the cash that a business generates towards its highest and best use. In the toy example in a business school book, maybe you’re Boeing, and we have this cash that our business generates, and we can either go bid on the next defense contract, and we’ll invest this much in R&D dollars, and we model this much revenue from the contract, or we go develop a clean-sheet commercial airliner, and we’ll put in this money, and we model this thing. It’s like a 16% IRR versus a 19% IRR. I prefer the 19%. In Google’s case, the projects are extremely heterogeneous where it’s like, we can give the YouTube team more funding so they can go improve the recommender algorithm and therefore time on site increases, and so does monetization. Or, we can give the Waymo team more funding so that they can actually get to market faster or scale up faster, or we can invest in this new AI approach that might pay off in five years time. I’m curious, if you are trying to put capital towards the highest and best use, and you’re ultimately comparing, how do you compare initiatives that are so different in nature and so different in payoff curve shape?

Sundar Pichai:

It’s a good question. I feel it today more than ever, ironically, because of TPU allocation. In some ways, I feel it even Waymo needs TPUs. Computers made the question, ironically, much more front of mind. By the way, of all the things I do, I’m really looking forward to how AI, as a companion, at least, gives inputs to this task.

I think once we can actually get all the data connected and flowing through. I think models are already capable. It’s more of getting all the data unlocked, I think it will be helpful…Historically, I think at Google, one of the advantages we have had is sometimes we make these decisions very early in the cycle. It’s almost like going back to that roots as a deep technology orientation.

On a constant basis, look, I’ve always viewed it as you have to assess the long-term value of these things. It’s almost like in some intuitive way, you’re thinking about the option value and the TAM of something 5–10 years down the line, and you assume a crazy growth and think through whether those decisions make sense.

The TPU investments have been great that way. We’ve steadily invested in that. Waymo was a great example where I think we increased our investment two to three years ago when the rest of the world got pessimistic on it. When others, some of the people were backing off.

…if Waymo had reached this point earlier, I think I would have invested the capital earlier. To some extent, I think you were judging it by... You want to be good stewards of capital. To the extent you’re bullish on ROIC, you want to invest every last dollar you can there.

…This is why we’ve invested in other companies…But we always thought about it with the lens of being good stewards of it. We felt our investment in Stripe was being a good steward of our capital. SpaceX, and Anthropic and so on. I think now with the AI shift, there are more opportunities on which we can deploy capital in a good way, and so we are doing that.

…we’ve always had a compute budget, even in classic compute. I would say with ML, and we use both TPUs and GPUs, by the way, extensively. ML compute planning is... We are super thoughtful about headcount planning, too, but we have always had to plan that. ML compute, we’ve gone through phases where they’ve been easy, and then there have been phases where we’ve been constrained as a company.

But now it is really acutely constrained. You spend a lot more time. I at least spend a dedicated hour a week thinking about that question at a pretty granular level. I will know by projects and by teams, the compute units they are using, or at least I have that information, and I’m looking at it and assessing it. In some ways, it’s a really important thing to be doing right now, I feel.

…The scarce resource is compute in a lot of cases, and so you’re ensuring that Google’s precious compute resources are being spent on the most worthwhile”

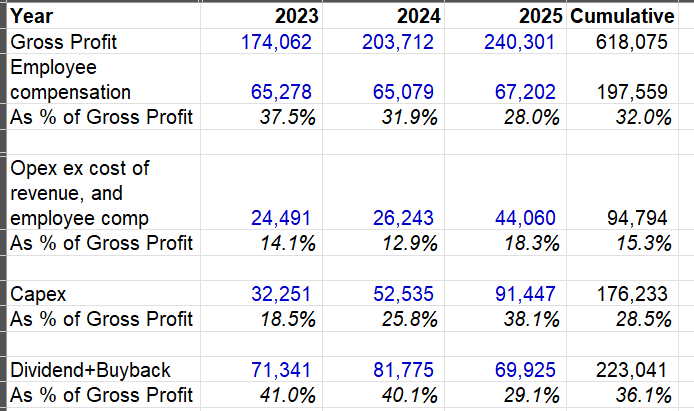

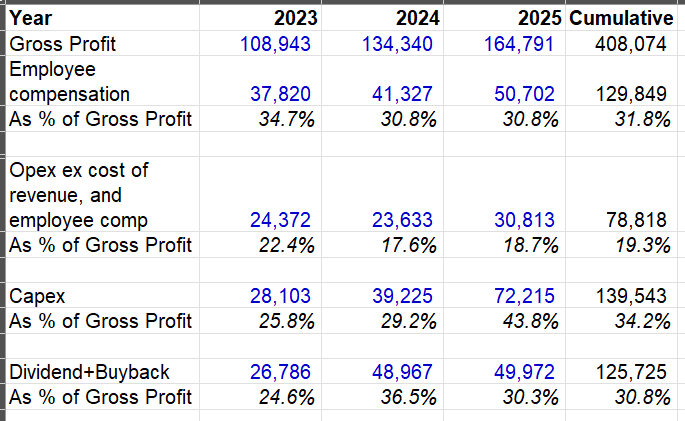

I think Pichai’s response to capital allocation question is pretty revealing how Alphabet thinks through investing their capital both through income statement and balance sheet. Alphabet and Meta actually both started disclosing their employee compensation expenses separately which gives us bit of a peek how they allocate their gross profit in both income statements and balance sheets.

I think it’s quite interesting that while Zuckerberg received quite the limelight to pen “The Year of Efficiency” memo in 2023, you could perhaps argue Sundar Pichai paid closer attention to efficiency mantra than Zuckerberg himself did since then. Alphabet’s employee compensation expense was essentially flat over the last three years whereas Meta’s employee compensation increased by 34% during the same period.

You may wonder about the noticeable jump in Alphabet’s opex ex cost of revenue and employee compensation line item below which increased from ~$26 Billion in 2024 to $44 Billion in 2025. A couple of drivers for this sudden jump is: a) Alphabet has moved its shared AI R&D to “Alphabet-level initiatives” which is embedded here, and b) EU regulatory fines. Similarly, Meta also expenses its non-revenue generating GPU depreciation through R&D line item which also helps explain their noticeable increase as well. I still think it perhaps reveals how much discretionary expenses Meta still harbors in its income statement given the fact that back in 2023 and 2024, both companies had similar opex ex cost of revenue and employee compensation despite Meta generating ~60-70% of Alphabet’s gross profit and Alphabet operating in businesses that are naturally much more opex intensive (think Cloud’s S&M, for example) than Meta’s operations. As long as Meta’s topline continues to grow at a healthy clip, you can perhaps appreciate why shareholders may not need to worry too much about margin sustainability over the medium term. Anytime Zuckerberg re-reads his own efficiency memo, he can probably find more opportunities to sustain or improve Meta’s margins.

One way to look at Meta and Alphabet’s capital allocation over the last three years is that ~30% of their gross profit went to employees, ~30% to machines, and ~30% to shareholders. The mix, however, is changing very rapidly. In both companies, the gross profit share that went to employees and shareholders is dropping noticeably every year and given the capex outlook in both companies, this mix shift will accelerate further in 2026 (and likely beyond 2026).

Alphabet

Meta Platforms

In 2026, ~55-60% of Meta and Alphabet’s gross profits will go to the machines, ~20-25% will be paid to employees, and ~15-20% to shareholders. Of course, shareholders don’t necessarily want the money back from these companies as long as the machines keep producing compelling ROIC. So, this isn’t quite man vs machine, rather man and machine. The machine is still working for the man…for now!

In addition to “Daily Dose” (yes, DAILY) like this, MBI Deep Dives publishes one Deep Dive on a publicly listed company every month. You can find all the 67 Deep Dives here.

Current Portfolio:

Please note that these are NOT my recommendation to buy/sell these securities, but just disclosure from my end so that you can assess potential biases that I may have because of my own personal portfolio holdings. Always consider my write-up my personal investing journal and never forget my objectives, risk tolerance, and constraints may have no resemblance to yours.

My current portfolio is disclosed below: