"Founder Mode" Complacency

Colossus recently published a chapter from Sebastian Mallaby’s new book on Demis Hassabis titled “The Infinity Machine”. I haven’t read the book, but did read this chapter. It was a riveting read. While I knew DeepMind had second thoughts about staying within Alphabet’s umbrella, I didn’t appreciate before how close it got for DeepMind to untangle themselves from Alphabet to become an independent company. Perhaps the man who deserves a lot of credit that Alphabet still has DeepMind in their wing to navigate the ever shifting AI landscape is Sundar Pichai.

While it was almost commonplace to call for Pichai’s resignation during the post-ChatGPT almost embarrassing wobbling “Bard” period, I was more indifferent towards his role. To be clear, my mind was also consumed about Google’s search primacy in the age of AI, but I was worried more about structural concerns that wouldn’t be alleviated by the change of management. Google has so far assuaged such concerns, but this behind-the-scene saga with DeepMind made me update my opinion on Pichai in a much more positive light.

When DeepMind was plotting to extricate themselves from Alphabet almost a decade ago, Pichai was prescient enough to foresee AI’s paramount importance in their core business. Let me share a couple of excerpts from the chapter (emphasis mine):

“In the summer of 2016, Hassabis held his fifth round of talks with Larry Page, and the details of a DeepMind spin‑out were laid down in a formal term sheet. A few months later, to ensure that everyone was on the same page, Hassabis met with the new CEO of Google, Sundar Pichai, who had assumed the top job when Page had moved upstairs to head Alphabet. An engineer with an MBA from Wharton and a background as a management consultant, Pichai had a boyish grin, an affable manner, and a dislike of confrontation. His discussions with Hassabis and Suleyman were cordial but bland. Pichai was not going to rock the boat, the DeepMinders concluded.

…Four days later, the DeepMind duo got on the phone with Pichai. This time the CEO revealed the steelier side of his personality. He said that turning DeepMind into a semi‑independent Alphabet company might not be in Google’s interests, after all. The “bet” option was for moonshots unrelated to Google’s core business, he said—projects such as autonomous cars or the science of life extension. Artificial intelligence did not belong in that bucket. To the contrary, AI was destined to become strategically important to Google’s flagship products, such as search and cloud computing.”

As these negotiations became more tense over time, all the big guns of Alphabet planned to meet to resolve the issue at hand. Alas, some big guns didn’t seem to appreciate what was at stake. From the book:

When the two sides met again, the conversation underscored the gulf between them. Hassabis and Suleyman argued that DeepMind did not fit under Google’s umbrella: Its mission was AGI, not consumer‑internet products. Pichai objected that AI was central to his vision for Google, and that he would not allow his scientific bench to be depleted. Hassabis had hoped that Larry Page would weigh in on his side and push the Alphabet plan to a conclusion. But Page showed up for the meeting two hours late, and Sergey Brin was even later. Their version of what later came to be known as “founder mode” was that they were nowhere to be found, disproving the Silicon Valley mantra that founders deserve the right to control their companies indefinitely. With Page and Brin effectively checked out, Pichai was the man DeepMind had to deal with.

I have been thinking about the aforementioned excerpt for the last couple of days. If you glanced at my portfolio, it’s not difficult to see that I drank my fair share of kool-aid of “founder mode”. Perhaps fittingly the “founder mode” propaganda originated from a founder himself: Brian Chesky. The more I ruminated over “founder mode”, the more I came to the conclusion that there is a glaring missing aspect in “founder mode” mantra: Complacency.

It is telling that Chesky proudly recalls every chance he gets about how he figured out during Covid that Airbnb doesn’t need to do search advertising; as an investor I was actually a bit alarmed that he was running Airbnb pre-pandemic without paying close attention whether his advertising dollars was being deployed with appropriate ROAS guardrail. I can guarantee you that despite operating in “Manager Mode”, Glenn Fogel at Booking was looking at advertising ROI with a microscope and he certainly didn’t need a global pandemic to remind him how to deploy his precious advertising dollars at Booking.

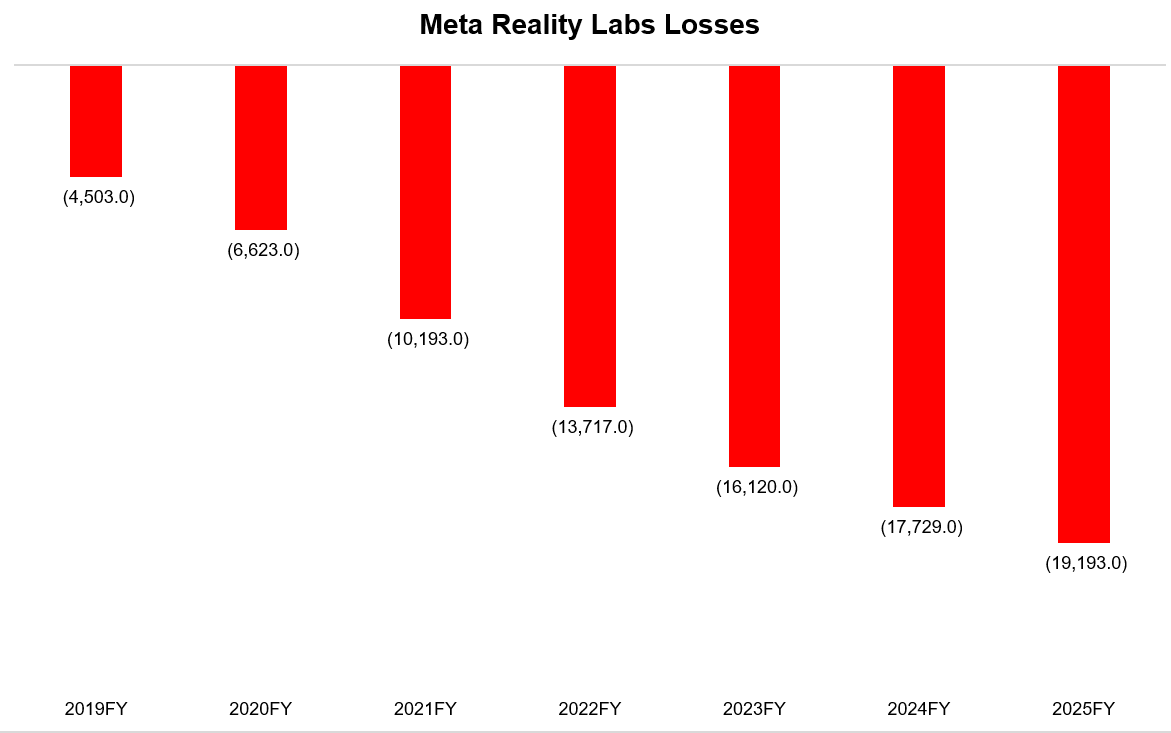

Is there any manager who would survive in any company if one of your segment operating performance looks like Meta’s Reality Labs? It is a tad bit astonishing that a founder who has built one of most generation defining businesses in the last couple of decades also managed to fund one of the ugliest cost structures of a business segment I have ever seen. I don’t think there is any manager out there who would fund a segment whose revenue in 2025 was essentially flat since 2021 despite losses becoming ~5x during this period. The only other business that I can think of with similarly lopsided, ugly cost structure is CoStar’s Homes.com. Of course, Homes.com is also a brain child of “founder mode”.

In fact, for all the effusive praises Daniel Ek at Spotify or Tobi Lutke at Shopify receive these days, I do wonder at times how on earth these founder led companies became so incredibly bloated in the first place. At least, Zuck had his “monopoly” profits to fund science projects at Reality Labs, but Spotify and Shopify both operate in a much lower gross margin and competitive market.

I guess I shouldn’t act too surprised how this happened in those companies if I look inward a bit more closely. I launched MBI Deep Dives in September 2020 and I too was enamored by the rapid growth that followed in 2021. In fact, I was so infatuated with the initial growth that I thought I should hire another analyst to help me with my Deep Dives. Fortunately, the guy I really wanted to hire decided to launch his own startup unrelated to investment research and turned down my offer. By the time I wanted to think about other potential candidates, 2022 arrived and Mr. Market schooled this very founder some lessons about investment research newsletter industry. It turns out my business operates in a much more procyclical fashion than I initially appreciated and it would indeed be a mini-disaster if I had hired someone at the peak of 2021. As you can see, founders don’t have any special or magical power that will insulate themselves from the very human nature of complacency that naturally creeps into your mind following some success. Now imagine building companies such as Alphabet, Meta, Shopify, Airbnb, or Spotify? Given the scale of their success, it would be almost miraculous if these founders didn’t suffer even a more pernicious form of complacency from time to time than I ever did.

Let me be clear: Chesky or Zuckerberg are indeed generational founders. But the “halo effect” of the “founder mode” can go a bit too far, especially during bull markets. I still, however, maintain that all else equal, I would rather have founders at the helm especially when a company’s back is against the wall. During more existential periods, managers can indeed be more susceptible in saving their jobs in the near-term potentially at the expense of saving the company in the long-term. But investors deploying their hard earned savings should be careful in not giving wanton license to founders coasting on past glories.

In addition to “Daily Dose” (yes, DAILY) like this, MBI Deep Dives publishes one Deep Dive on a publicly listed company every month. You can find all the 67 Deep Dives here.

Current Portfolio:

Please note that these are NOT my recommendation to buy/sell these securities, but just disclosure from my end so that you can assess potential biases that I may have because of my own personal portfolio holdings. Always consider my write-up my personal investing journal and never forget my objectives, risk tolerance, and constraints may have no resemblance to yours.

My current portfolio is disclosed below: