Constellation Software 4Q'25 Update

Amidst an unprecedented drawdown relative to its history, Constellation Software (CSU) had a rather reassuring quarter. Things are, at least so far, chugging along just fine.

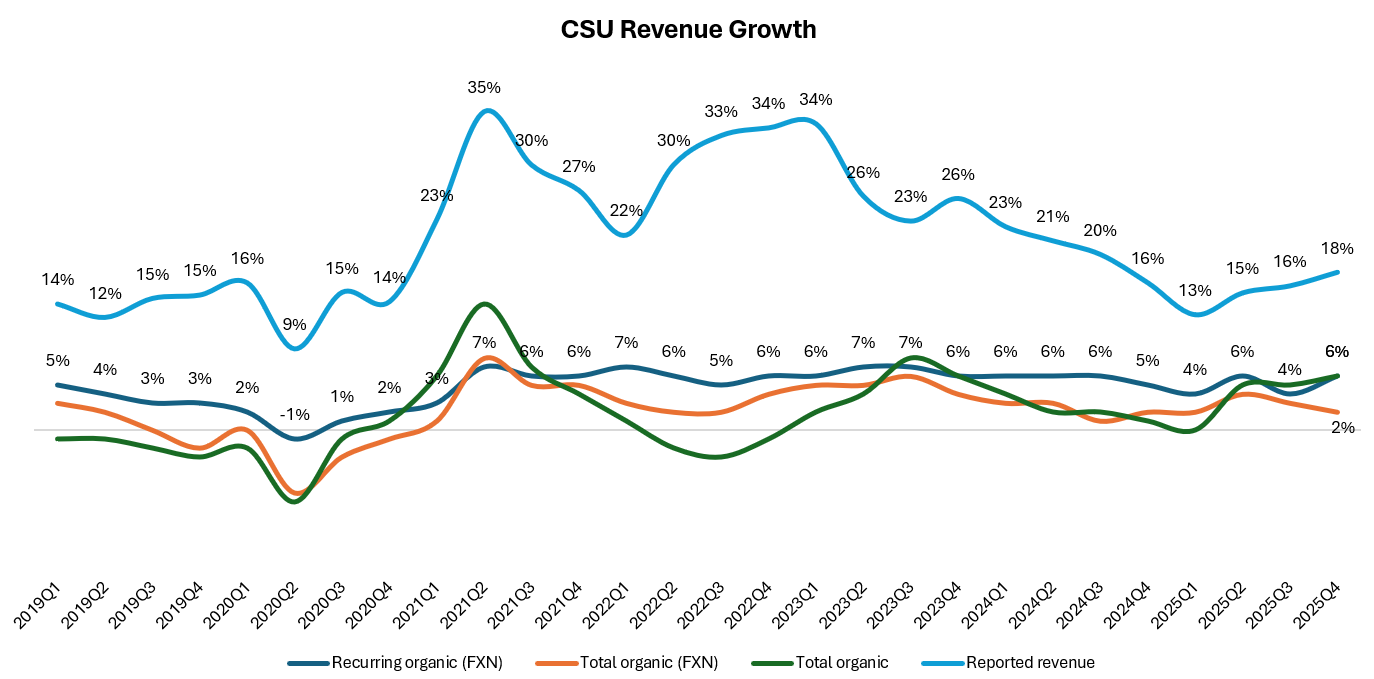

The maintenance or recurring revenue segment, which is ~75% of their revenue, grew by 6% (FX adjusted) YoY in 4Q’25 which is a ~200 bps acceleration from 3Q’25.

Is AI accelerating CSU’s organic revenue growth? Management confirmed during the call that AI has so far neither contributed nor contracted CSU’s organic revenue.

Is AI making price increases harder for CSU? Again, no impact yet.

Of course, CSU management is smart enough to know that just because AI hasn’t made a dent yet doesn’t mean their businesses will remain immune from it in the long-term. As I have mentioned before, given CSU has hundreds of different VMS businesses, CSU management will not be short of evidence if AI is indeed impacting some niches, and they will also have a much better clarity what type of software businesses have more durability. The company is actively encouraging all of their operating groups to share their learnings and findings from the field. From the call:

“Best practice sharing across our operating groups is one of our genuine differentiators. And I’ve seen more cross-portfolio collaboration around AI in the past year than on any topic in recent memory. Over the past 12 to 24 months, we’ve directed our culture of best practice sharing to helping our businesses navigate the AI transition thoughtfully.

…But I want to be direct about something, building products and features faster will not be what differentiates us long term. That capability will become widely available. It’s going to be table stakes. What will matter is what our businesses have spent many years developing, deep vertical knowledge, a genuine understanding of customer workflows and processes, the data inside their solutions and the trusted relationships they’ve built. I believe AI will help us do all of this better. When I look at where this leads, the opportunity I find most interesting is what I described as knowledge networks, connecting our domain expertise, customer process knowledge and data assets in ways AI now makes possible. That’s a long-term build, and we’re in early days, but the foundation is real.

Our customers rely on us for mission-critical software. We believe that the trusted partner position we’ve earned in our verticals is now extending to guiding them on how to safely and effectively bring AI into their own businesses.”

Indeed, writing the code itself was never quite the core differentiator for almost any software business. Listening to the CSU earnings call reminded me of the similar point raised by Benedict Evans in a Stratechery interview last month. From Benedict Evans:

“I never thought that the hard part of building a piece of software that manages the thing for the other thing in the thing deep inside a big company was writing the code.

That’s not the hard part. The hard part is working out that that problem exists and then working out the right way of solving it and then going out and building a go-to-market and working out how to get your customers to buy it. It’s the implementation, the execution, the route to market, the right way of solving the problem.”

Perhaps the most reassuring moment for CSU shareholders was when management explained how they plan to follow essentially a Schumpeterian process in their capital allocation during AI’s potential disruption. From the call:

“…we’re very decentralized, and we trust each of our businesses to sort of have a strategy around this and learn from each other, and our coaches pushed them hard on making sure they’re moving things forward. But we don’t look at it as it’s going to be a situation where, as always, some of our businesses do better than others adapting to disruptions in their markets. And we’ll make sure that we, as a conglomerate, we will put the capital in the hands of the people who we feel will continue to invest at good returns for our shareholders.

….as a good conglomerate, we want to make sure we’re putting the capital behind the people who are winning. And if you’re losing, we’ll take your capital and put it elsewhere, which doesn’t sound very nice, but that’s what we’ll do.”

I will talk more about CSU’s margins, acquisitions, ROIC, and valuation behind the paywall.

In addition to “Daily Dose” (yes, DAILY) like this, MBI Deep Dives publishes one Deep Dive on a publicly listed company every month. You can find all the 66 Deep Dives here.