AWS: Pre and Post-ChatGPT

Back in 2014, Jeff Bezos wrote to Amazon shareholders:

“A dreamy business offering has at least four characteristics. Customers love it, it can grow to very large size, it has strong returns on capital, and it’s durable in time – with the potential to endure for decades. When you find one of these, don’t just swipe right, get married.”

Bezos went onto discuss how promiscuous Amazon has been in finding and marrying such great businesses. One of the key focus areas for Bezos in that letter was Amazon Web Services (AWS) which he labeled as “market size unconstrained”.

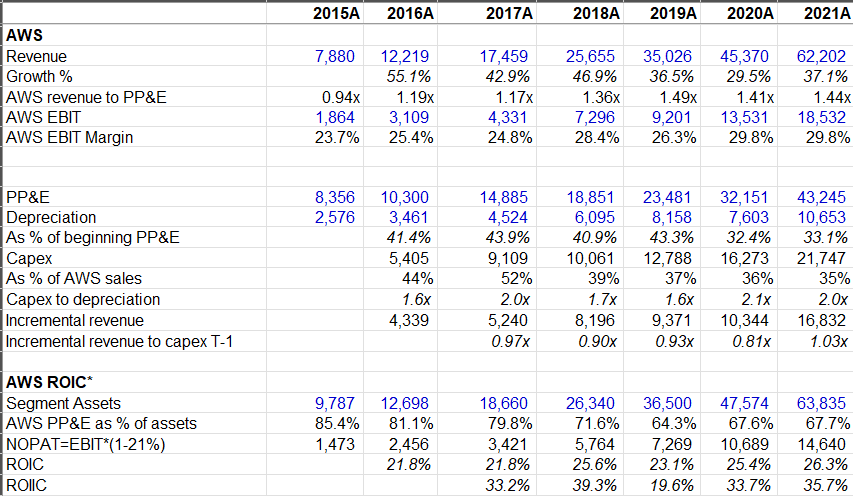

The very next year after Bezos writing that letter, Amazon divulged AWS numbers to the broader public. To most investors’ surprise, AWS turned out to be mid-20s operating margin business with wonderful returns on capital that even some of the best businesses would envy. Before ChatGPT came to the scene, AWS essentially proved to be a “dreamy” business pretty much every year since its numbers were revealed. In fact, despite Azure and GCP frenetically trying to catch up to a business with such envious characteristics, the numbers continued to be better and better with each passing year. By 2021, AWS operating margin became ~30% and ROIC improved to mid-20s. The incremental ROIC looked even more attractive as AWS routinely posted mid-30s ROIIC in the pre-ChatGPT world.

Then the world changed permanently in November 2022 when OpenAI released ChatGPT. I will explore what happened to AWS post-ChatGPT so far and what may happen in the next five years behind the paywall.

In addition to “Daily Dose” (yes, DAILY) like this, MBI Deep Dives publishes one Deep Dive on a publicly listed company every month. You can find all the 66 Deep Dives here.