AI Economics in the East

In the most recent All-in episode, Brad Gerstner from Altimeter (which owns stakes in both OpenAI and Anthropic) pushed back at the gross margin concerns for AI labs. From Brad Gerstner (emphasis mine):

“Their gross margins are exploding higher. Like the fastest increase in gross margins I've probably seen out of any technology company.

…it's gone from meaningfully negative 18 months ago to, you know, very, very positive. I've seen rumored out there 50 to 60 percent”

Given that Gerstner owns these companies, I think he’s highlighting numbers that he knows are at least directionally accurate. Nonetheless, it is frustrating to follow these AI labs while they remain private companies and everyone’s job would be lot easier if both OpenAI and Anthropic became public companies. Since that is yet to be the case, our best bet to gauge the evolving economics of AI labs may be to study the publicly listed Chinese labs more closely. One such company is Knowledge Atlas Technology JSC which is more commonly known as “Zhipu AI” in China. Since going public early this year, the stock is up a cool ~6x in just three months! Despite such a meteoric rise, the Enterprise Value (EV) is still hovering around ~$50 Billion. Don’t be misled thinking Zhipu has an overly conservative shareholder base though; the stock currently trades at ~127x NTM revenue! But to their credit, revenue has become nearly 6x since 2023! Let’s take a bit deeper look into how they’re growing at such a rapid pace.

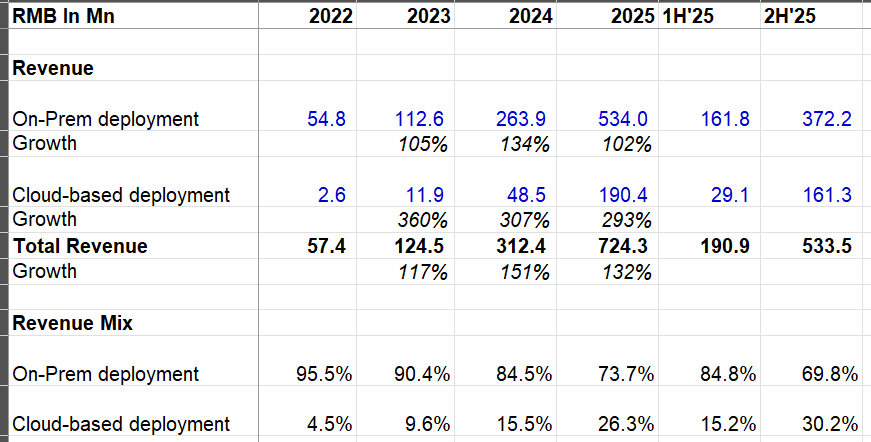

Zhipu discloses revenue in two broad categories: On-premise deployment and Cloud-based deployment.

On-premise deployment means the customer takes Zhipu’s model and runs it inside their own infrastructure. A bank, a telecom operator, a state-owned enterprise, or a government agency signs a contract, Zhipu's engineers show up, install the model weights and the serving stack on the customer's servers (or in the customer's private cloud), tune it for the customer's data and workloads, and hand it over. In China, this channel exists largely because data security, and regulatory comfort make many large customers unwilling to send sensitive data out to someone else's cloud.

In cloud-based deployment, as you can imagine, the customer does not install anything. They get an API key, they call Zhipu’s model over the internet, and Zhipu serves the tokens from its own GPU infrastructure. Revenue is recognized over time, either ratably for subscriptions or based on actual usage for pay-as-you-go. As you can see below, revenue from cloud-based deployment is basically tripling every year in each of the last three years.

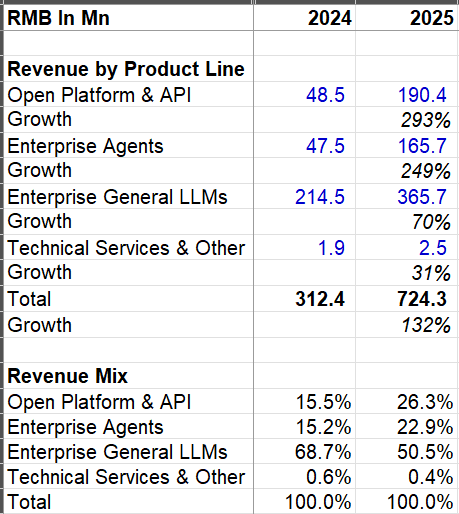

In the most recent earnings, Zhipu also provided a separate segment disclosure of revenue by product line. Zhipu runs what it calls a MaaS platform, short for Model-as-a-Service, which is essentially the Chinese analogue to Anthropic’s or OpenAI’s API business. Customers can either call Zhipu's GLM models over the cloud and pay by usage, or they can have the models deployed on their own infrastructure for security and customization reasons, which Zhipu calls on-premise deployment. As you can see below, the API business is growing the fastest. It’s not just API business, the agents are also in very high demand in China. Notice the “enterprise agents” revenue below which increased by 249% YoY. The underlying offerings in enterprise agents include things like CoCo (their enterprise agent), AutoGLM (the general-purpose mobile agent), and increasingly the productized agent systems built on top of GLM for specific workflows. In practice, this line captures situations where the customer is not buying raw model access but rather a packaged agent that plans, uses tools, and completes tasks end-to-end. While the API business and agents were only ~30% of the overall revenue in 2024, they were almost half of the revenue in 2025.

Coding in particular is where Zhipu has gone from being one of several credible Chinese labs to being a global frontier participant. If you look at Arena’s leaderboard, Zhipu’s model (GLM 5.1) is actually only behind Anthropic’s right now. I asked Claude to translate Zhipu’s press release in English; you can sense the increasing confidence of Zhipu’s differentiation especially in coding as they have been raising price to meet the demand in a “compute panic” market. From the translated press release:

Our GLM Coding Plan, launched in 2025, rapidly gained global coverage on the strength of native high-quality engineering reasoning capabilities, with paid developers exceeding 242,000. With confidence from technical leadership, we proactively raised prices by 30% in February 2026 and removed first-purchase discounts.

MaaS Platform: Through BigModel.cn, our MaaS platform has become the hub connecting foundation models with industry applications. Within 24 hours of GLM-5’s release, ByteDance, Alibaba, Tencent and other top platforms officially integrated it; 9 of China’s top 10 internet companies have deeply integrated GLM. As of March 2026, registered users exceeded 4 million. Even with API pricing increased by 83% from late last year, the market still showed a supply-shortage “compute panic.”

But revenue is one thing; how about the margins? That was indeed where I have seen some interesting developments which I will elaborate behind the paywall.

In addition to “Daily Dose” (yes, DAILY) like this, MBI Deep Dives publishes one Deep Dive on a publicly listed company every month. You can find all the 67 Deep Dives here.