Airbnb's Soul Search Beyond Homes

Programming Note: I am going to take a Summer Break for a couple of weeks. I am actually traveling to Bangladesh to spend some time with family after three and half years. I expect to start posting daily on June 8th onward.

Yesterday, Booking CEO Glenn Fogel appeared on JP Morgan Annual TMT Conference. On the same day, Brian Chesky from Airbnb released their annual summer release. Both companies are increasingly encroaching into each other’s territories, so it was interesting to hear them both on the same day.

Both CEOs wanted to establish the long-term resilience of travel demand. It is a common observation among investors that travel demand is highly discretionary in nature, and hence can be vulnerable to near-term macro uncertainties. It kind of reminds me of the common trap many investors find themselves in for companies which generate revenue from advertising. Haven’t we all heard how Google and Meta’s advertising revenues are “cyclical” even though it can be really, really hard to see “cycle” if you take a look their financials? Never mind that the very nature of direct response advertising is fundamentally different than brand advertising from our grandparents days. Similarly, while travel demand can indeed be deeply affected near term by multitude of macro factors (war, recession, oil price, pandemic…take your pick), one of the higher conviction predictions you can perhaps make about the next couple of decades is that the average number of trips per thousand people globally will keep increasing. Fogel reminded that such secular tailwind is still very much in place:

“…long term, travel has always in the past, and I absolutely believe always in the future, will be a growth industry. No matter how you want to measure it, you can look back over a number of implements, you can go back and just look at any statistics about total spend on travel. It has exceeded global GDP by 1% to 2% for a very, very, very long time.

And it’s obvious to see why. As people get wealthier, they generally want to travel more. You have the basics of people who are too poor to travel, enter a lower middle class and now can afford to travel. About half the people on this earth. So you’re talking about 4 billion people cannot afford to travel. Those people are slowly becoming wealthier, becoming able to travel. So that’s an absolute tailwind for travel.

Then you get into our business where we do stuff digitally. And it’s hard to measure, but we’ll pick round numbers. Maybe 1/3 of the people do not buy their travel digitally. So that’s another tailwind. Those people who do it non-digitally, they will die, and then the younger people will come in, and they will be able to -- they’ll do their travel, and that will be digital. So that’s another tailwind for our business.

I absolutely believe and once you have established your basic needs, what are the things that give you the most enjoyment in life? How many people say, “Well, I’m sick of traveling, I don’t want to go anywhere. I just want to stick at home.” Nobody practically does that. Everybody wants to travel more. So definite tailwind for us. For us, the bigger issue is not the secular industry, which I know, it’s how do we continue to gain share, how do we continue to get more than other ways people can do their travel digitally. And that is where we are focused on.

While very few people are skeptical about travel’s long-term appeal, there is usually more debate around which companies within travel can remain relevant for decades to come. OTAs are particularly under the scanner with AI potentially re-writing demand routing system. Fogel emphasized the core tenet of Booking: “in God we trust, everybody else brings data”; he will try everything under the sun and just double down on whatever the data tells him works the best.

Chesky, on the other hand, seems to trust someone else other than just “God”: himself! It’s hard to blame someone who built a generational consumer internet company such as Airbnb in his 20s to trust his intuitions. But unlike Fogel, Chesky basically needs to be slapped by data to force him to change his mind which at times makes Airbnb look a bit sluggish for a founder led company. During the summer release, Chesky revealed quite a few things on which he perhaps begrudgingly needed to change his mind. One of them is “Landmarks”.

Back in 2020 right after going public, Chesky had this to say about “landmarks”

Take his comments about Landmarks on Airbnb Experiences from 4Q’20 call:

“I think as the world starts opening back up, I think we're very bullish on experiences over the coming years. Because when people travel, they're going to want to do something interesting. And I don't think they're all going to desire to go back to getting on double decker buses and waiting in line in crowded lobbies or landmarks.”

Given this intuition, Airbnb focused on original and more quirky experiences rather than landmarks experiences such as Eiffel tower in Paris or Taj mahal in India. Thankfully, over time, he changed his tone and realized someone who’s visiting Paris for the first time will certainly want to “experience” Eiffel tower no matter how banal it may seem to someone who went to Paris a dozen times. So, yesterday Airbnb revealed that based on their survey they came to know that more than 75% of travelers want to visit a landmark when they travel to a new city. My guess is Airbnb needed to do that survey to convince Chesky that Airbnb must scale their supply in landmarks if they ever hope to scale that business. Airbnb now has more than 3,000 landmark experiences on their platform.

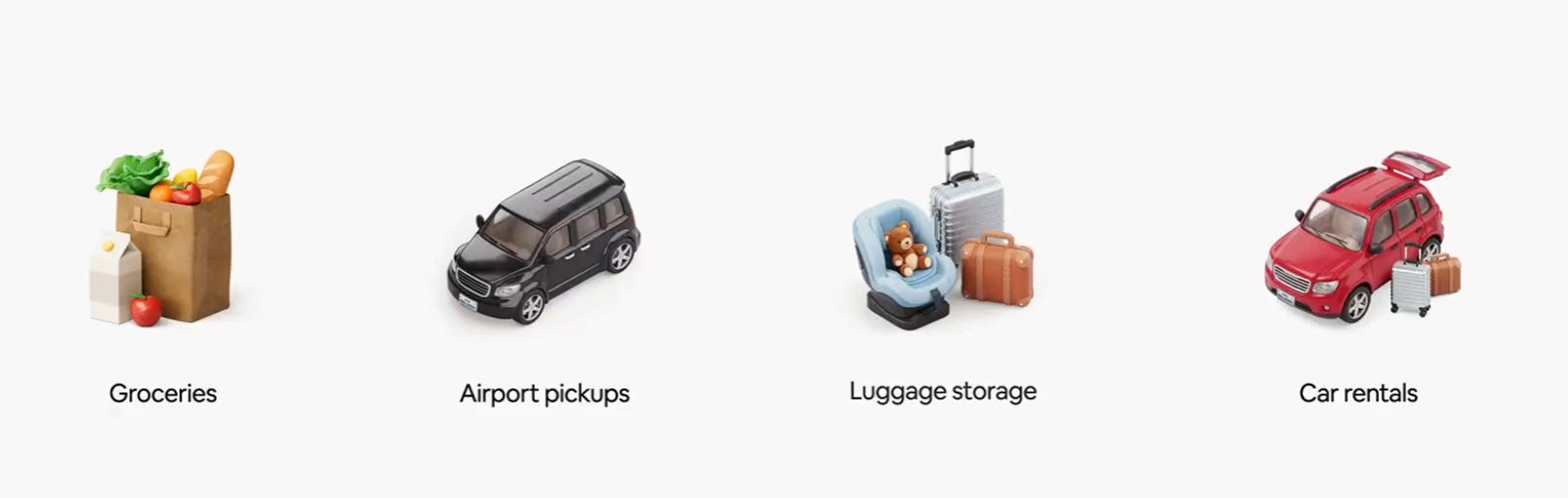

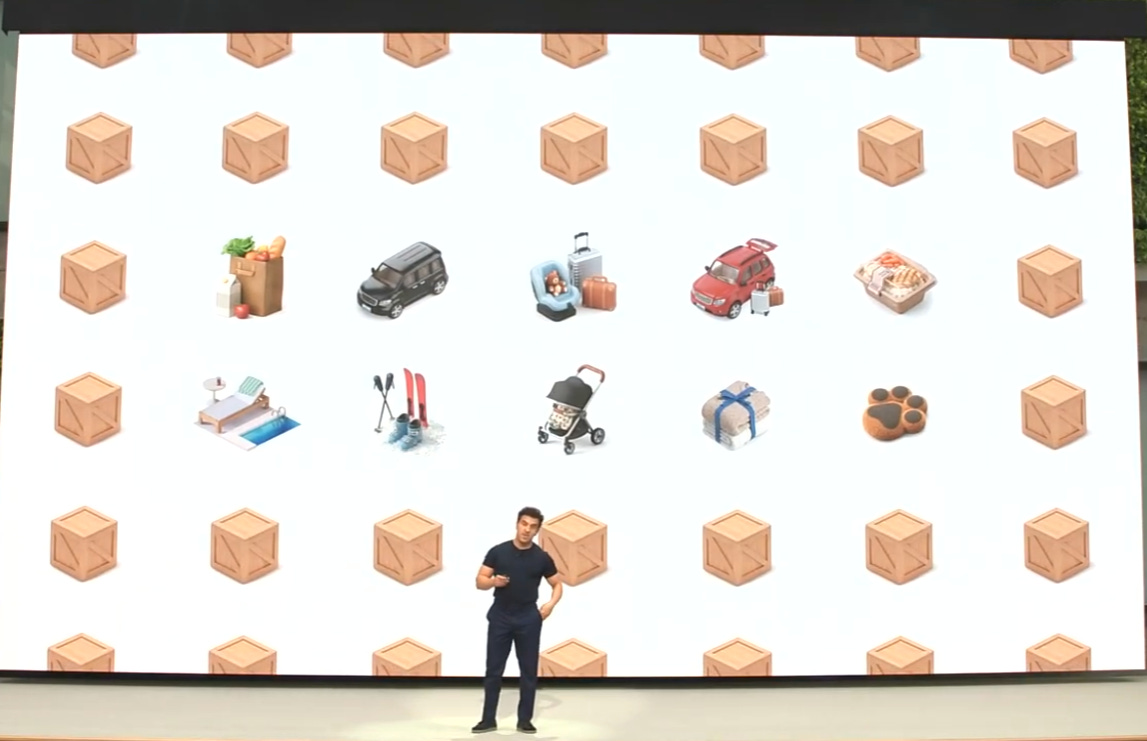

Airbnb also launched several new categories of “Services” yesterday: groceries, airport pickups, luggage storage, and car rentals.

Airbnb typically does two product release per year. Chesky mentioned that later in 2026, Airbnb expects to launch services such as Day passes at local gyms, at-home pet services etc. Interestingly, instead of building their own supply (an approach they have taken in experiences), they’re launching these services by partnering with existing players in those categories: “Instacart” for groceries, “Welcome Pickups” for airport pickups, and “Bounce” for luggage storage. So this is a classic asset-light, take-rate aggregation model Chesky is layering a services marketplace on top of the core stays business rather than building vertical supply. If Airbnb ever hopes to scale these businesses, I do think that is the right approach.

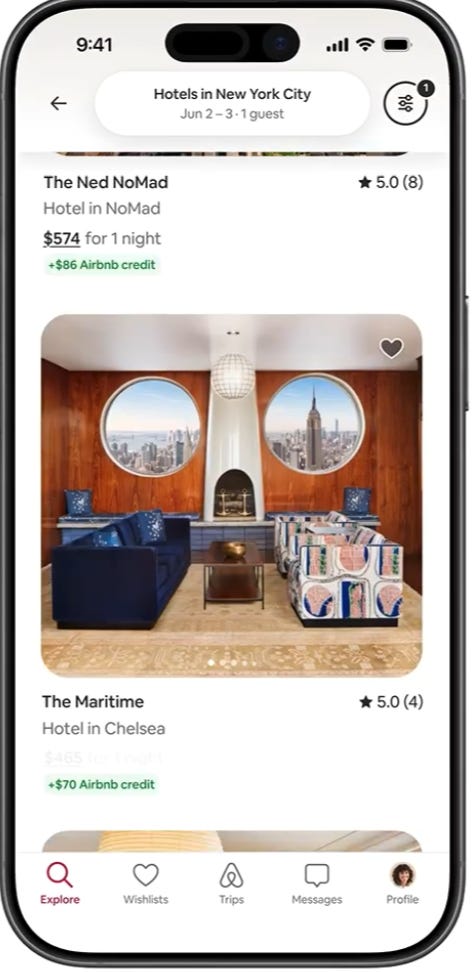

While Airbnb didn’t launch any loyalty program yet, the sketch of such a potential program is gradually starting to take shape. When Airbnb discussed their ramp up in getting more boutique hotels on Airbnb, the screenshot showed guests booking hotels will receive “Airbnb credit”.

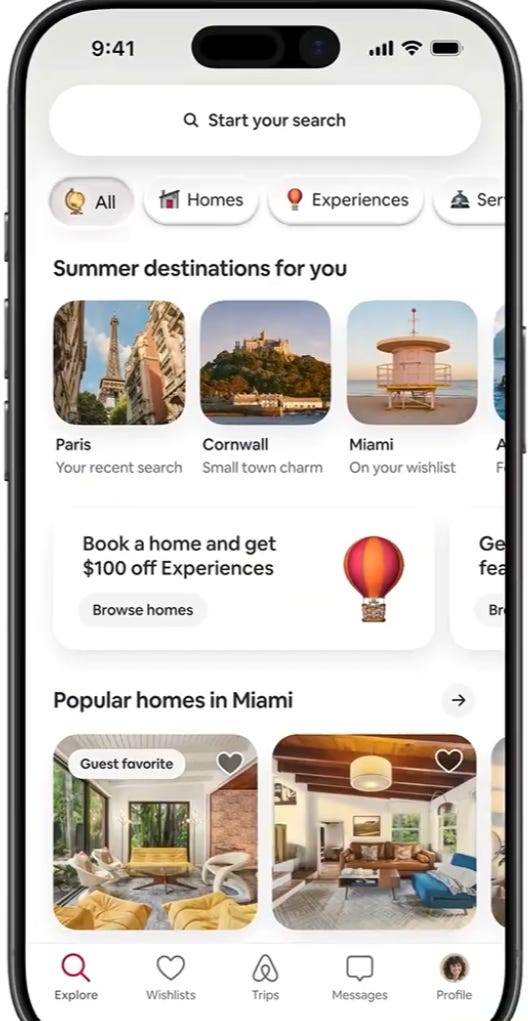

Similarly, when they were showing their newly re-designed home page, it included things like “Book a home and get $100 off Experiences”

Chesky really wants “Airbnb” brand to mean something much more than homes. In an interview with WSJ yesterday, Chesky was quite explicit about it. From the interview:

“I want the atomic unit of Airbnb, the center of Airbnb, not to be homes, but to be people.

I want us to be a community, and around the community, I’d like you to be able to get a home, an experience, a service, a hotel, and then 10 or 20 other things that you can offer. And our app will become an agent.”

His focus on “people” i.e. guests/customers and looking at all the services and cross-discounts across categories makes me think Airbnb is likely to launch a subscription tier perhaps next year once they aggregate a good chunk of services categories. Chesky has been waxing praises on Amazon Prime for a while now, especially how there is no such thing as Amazon Prime for services.

Airbnb's structural vulnerability is that travel is a low-frequency, high-deliberation purchase where the median Airbnb guest in the future may be willing to search across Google, direct sites, or AI chatbots and Airbnb has no mechanism today to collapse that consideration set in its favor unless the trip itself makes Airbnb more of an obvious choice (e.g. group travel, longer stay, areas where there is no hotel available etc.) . A paid membership is perhaps the most effective tool for solving this problem and the Services layer may be the lynchpin to make this work. Imagine something like “Airbnb One”, priced at $99/year (or whatever), which gives a $50 stay credit applied automatically to the subscriber's first booking of the year. On top of this, the subscriber can get an unlimited 15% discount on Services and Experiences (chefs, cleanings, photographers, training sessions, local experiences etc), capped at $20 per transaction but uncapped in frequency, structured to nudge subscribers toward many small redemptions across the year rather than one large one. Airbnb’s goal shouldn’t be to make money on that subscription program, rather create a platform by aggregating demand and integrating numerous services so that Airbnb can graduate from being a low frequency, high deliberation app to higher frequency, lower deliberation app. If they can build something like that, it may be much more valuable over time even if the unit economics of subscription program itself merely break evens (or incurs losses in initial years).

To be clear, as of today, Airbnb Experiences and Services “fair value” is likely closer to zero since Airbnb hasn’t quite delivered on being something beyond the core homes business yet. The stock also appropriately values the company on the core accommodation business, but it is an option intriguing enough to keep in mind if Airbnb ever gets closer to product market fir beyond homes.

Subscribers get the daily journal and five+ years of Deep Dives, i.e. full-length analyses with financial models on 65+ companies. The daily is just how I think out loud between the Deep Dives!

Current Portfolio

Please note that these are NOT my recommendation to buy/sell these securities, but just disclosure from my end so that you can assess potential biases that I may have because of my own personal portfolio holdings. Always consider my write-up my personal investing journal and never forget my objectives, risk tolerance, and constraints may have no resemblance to yours.

My current portfolio is disclosed below: