The Best Yardstick

After a very good 2023 and 2024, I wrote the following in my 2024 annual letter:

“given the somewhat elevated valuation multiples among stocks I have looked at, I think I wouldn't be too upset if I underperform the S&P 500 next year in case we see another >25% performance year for the index in 2025. There are times when it may make sense to underperform the index for you to be able to outperform over a longer period of time.”

Since then, MBI portfolio has been basically flat whereas index has generated +30% return in the meantime. So, I certainly got my wish granted even though I don’t seem to feel great about it today! If Buffett read this earlier sentence, I’m not sure he would be pleased about such sentiment. Back in 1997 shareholder letter:, he actually took a dig at such a strange behavior among investors:

“A short quiz: If you plan to eat hamburgers throughout your life and are not a cattle producer, should you wish for higher or lower prices for beef? Likewise, if you are going to buy a car from time to time but are not an auto manufacturer, should you prefer higher or lower car prices? These questions, of course, answer themselves.

But now for the final exam: If you expect to be a net saver during the next five years, should you hope for a higher or lower stock market during that period? Many investors get this one wrong. Even though they are going to be net buyers of stocks for many years to come, they are elated when stock prices rise and depressed when they fall. In effect, they rejoice because prices have risen for the “hamburgers” they will soon be buying. This reaction makes no sense. Only those who will be sellers of equities in the near future should be happy at seeing stocks rise. Prospective purchasers should much prefer sinking prices.”

Berkshire did just fine in 1998, but started materially underperforming the index in 1999 just when the internet mania went overdrive.

After such underperformance in 1999, Buffett himself was not as zen as he sounded in his 1997 shareholder letter. I went back to his 1999 shareholder letter and found Buffett was admonishing himself for trailing the benchmark. From the 1999 letter (emphasis mine):

“The numbers on the facing page show just how poor our 1999 record was. We had the worst absolute performance of my tenure and, compared to the S&P, the worst relative performance as well. Relative results are what concern us: Over time, bad relative numbers will produce unsatisfactory absolute results.

Even Inspector Clouseau could find last year’s guilty party: your Chairman. My performance reminds me of the quarterback whose report card showed four Fs and a D but who nonetheless had an understanding coach. “Son,” he drawled, “I think you’re spending too much time on that one subject.”

My “one subject” is capital allocation, and my grade for 1999 most assuredly is a D. What most hurt us during the year was the inferior performance of Berkshire’s equity portfolio -- and responsibility for that portfolio, leaving aside the small piece of it run by Lou Simpson of GEICO, is entirely mine. Several of our largest investees badly lagged the market in 1999 because they’ve had disappointing operating results. We still like these businesses and are content to have major investments in them. But their stumbles damaged our performance last year, and it’s no sure thing that they will quickly regain their stride.”

Reading such letters is a good reminder why Buffett is a special investor. The more mere mortals would take 1999 as an opportunity to point out the general excesses in the market and explain away their underperformance. Buffett, of course, also thought the investors went a little crazy with the internet stocks, but he started the letter not by pointing fingers at fellow investors, rather at himself.

Anyways, what was particularly interesting is that even the GOAT himself couldn’t be as self-reassuring at the face of trailing benchmark return! It turns out the pressure of the benchmark comes even for the very best. So, I guess I shouldn’t be surprised that I don’t feel great about trailing S&P 500 in the last year and half even though I am hoping to be net buyer of stocks for years to come.

In the stock market, there may be a lot of random walk along the way, but having a benchmark is indeed a decent barometer of how you are doing. As an investor who is not managing other people’s money, you could argue I have the luxury of being rather nonchalant even if I underperform the index for a few years. However, I suspect too much nonchalance is not healthy for anyone’s long-term track record either. One perhaps needs a healthy balance of nonchalance and self-introspection by looking at the mirror every once in a while to assess whether something needs to change. But when should such serious introspection begin?

While going through Buffett’s writing during the late 90s yesterday, I noticed that in his nearly six decades at the helm of Berkshire, Buffett had to endure three consecutive years of underperformance only once: 2003-2005 period. I’ll take that as a yardstick and if MBI portfolio happens to lag the index for three consecutive years, I should probably get out of my cocoon of nonchalance.

A reader recently messaged me: “how do you maintain such a highly concentrated portfolio when so many names seem to be going parabolic just outside your core holdings?”

One of the challenges of fintwit is you can constantly feel you’re not doing as well as others even when you’re outperforming the index. The reality is, in fact, decidedly the opposite. If you happen to be outperforming the index over 5-10 year period, you are almost certainly ahead of SUPERMAJORITY of investors. Supermajority, not just majority.

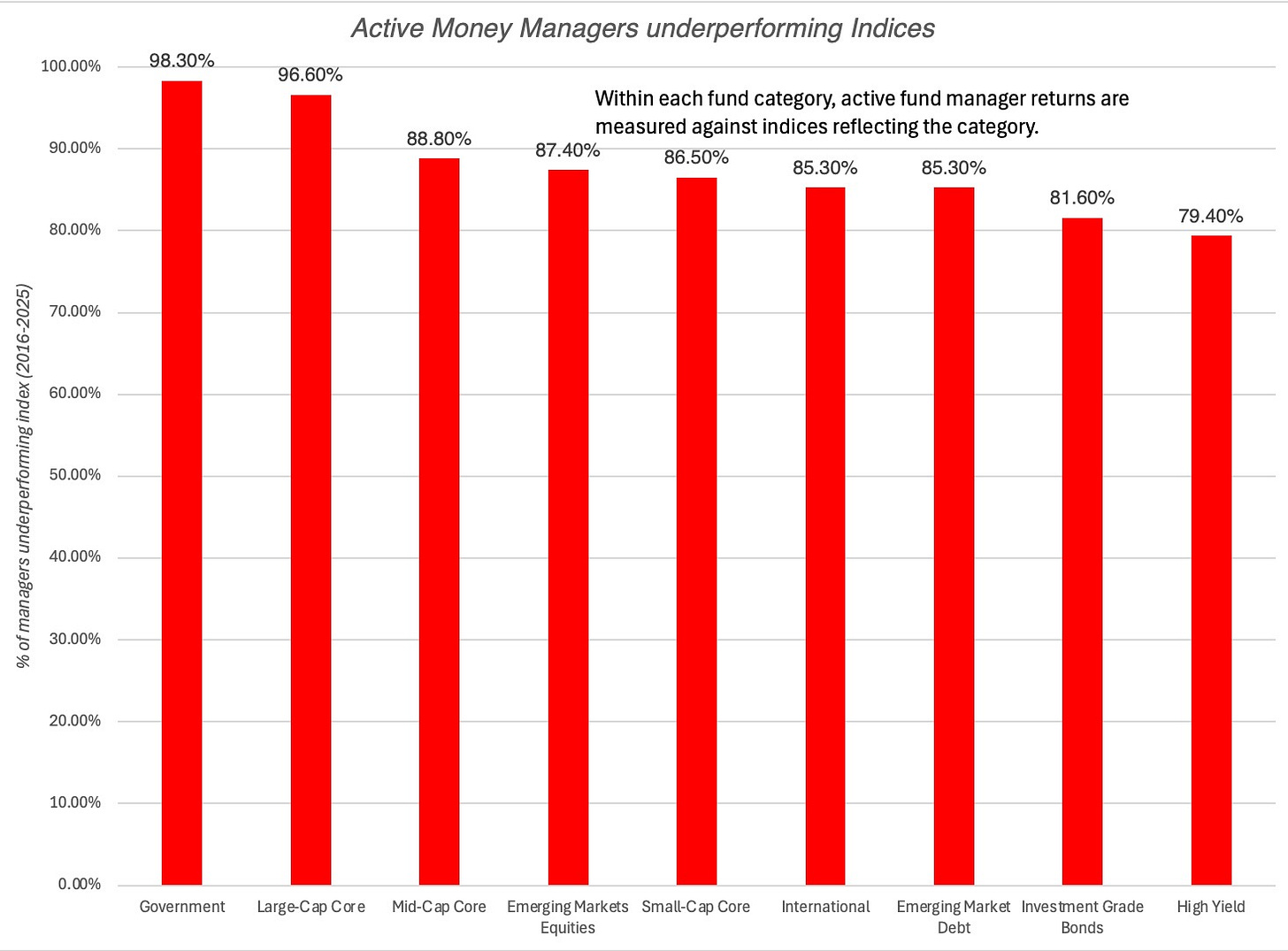

A great disservice that the benchmark’s performance does is it makes almost everyone feel that it is the “average” performance among active investors. Of course, you can never know what the twitter anons actually generate in return over any long period of time (since they’ll just go silent whenever they have a terrible year or even worse, they’ll simply lie through their teeth and claim how they sold at the peak…sure!), but we do have high quality audited data how professional investors do over the long term and such audited data should humble any active investor out there. However, many investors look at these data, and there is a strong urge to “explain” away professional investors’ sustained underperformance over any long period: “oh, these guys are index huggers”, “oh, these guys cannot structurally fish at the right areas”, “oh, these guys are dumb” etc etc.

As you can perhaps tell, I do not think any of those are good explanations. In fact, it is “by design” that supermajority of professional investors fail to beat the benchmark. Let me mention a story Howard Marks shared to make my point here:

“My memos got their start in October 1990, inspired by an interesting juxtaposition between two events. One was a dinner in Minneapolis with David VanBenschoten, who was the head of the General Mills pension fund. Dave told me that, in his 14 years in the job, the fund’s equity return had never ranked above the 27th percentile of the pension fund universe or below the 47th percentile. And where did those solidly second-quartile annual returns place the fund for the 14 years overall? Fourth percentile! I was wowed. It turns out that most investors aiming for top-decile performance eventually shoot themselves in the foot, but Dave never did.”

I actually shared this story before on twitter and I received a DM from a reader telling me that they do not believe such a thing is mathematically possible. In case I receive similar response again, I have preemptively asked Claude to create a visualization to explain this point. Claude even gave it a name “The Steady Eddie Paradox”. Play with it if you’re incredulous too!

The Steady Eddie Paradox

30 pension funds. 14 years. Watch what happens to the one that's never above the 27th percentile or below the 47th in any single year.

— Howard Marks, recalling David VanBenschoten of General Mills

I understand the difficulty of active investing well enough to know that supermajority of investors will not beat the index, including potentially yours truly. If you want to see whether you’re doing well enough, you just need to pay attention to the index. What you definitely don’t want to pay too much attention is the random people on the internet who are somehow posting market beating returns year after year. If you happen to be ahead of the index after 5-10 years of investing, good for you as you’re almost certainly ahead of supermajority of active investors and you may want to stay focused to remain ahead. If you’re lagging the index for years, perhaps it’s time for some introspection and do some soul searching.

Subscribers get the daily journal and five+ years of Deep Dives, i.e. full-length analyses with financial models on 65+ companies. The daily is just how I think out loud between the Deep Dives!

Current Portfolio

Please note that these are NOT my recommendation to buy/sell these securities, but just disclosure from my end so that you can assess potential biases that I may have because of my own personal portfolio holdings. Always consider my write-up my personal investing journal and never forget my objectives, risk tolerance, and constraints may have no resemblance to yours.

My current portfolio is disclosed below: