Unprecedented Lock-in

Apollo recently published their US housing outlook which is an interesting read to get up to speed on how the housing market is faring. Let me highlight a couple of things from their piece that stood out to me.

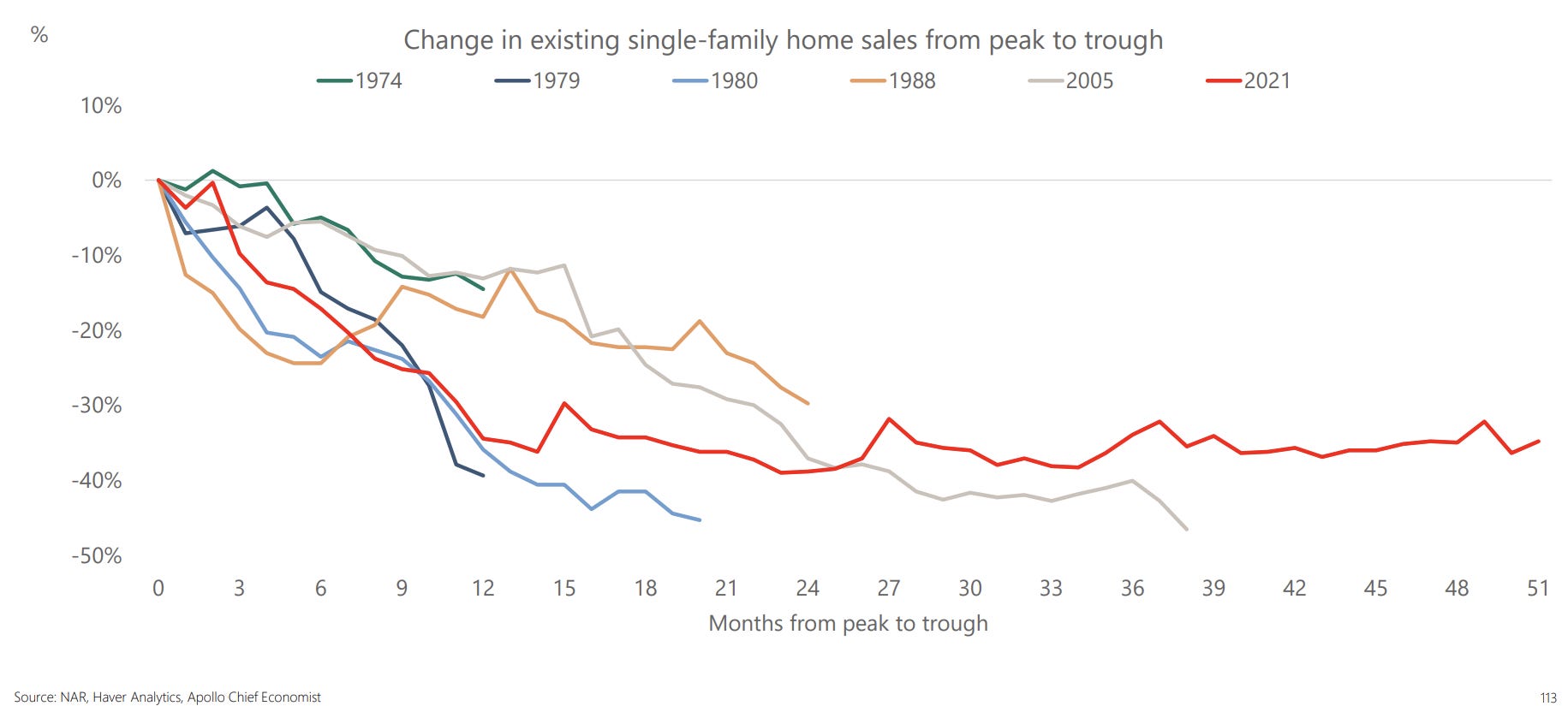

One of the things that jumped out to me is just how unusual the current housing cycle is compared to almost any period of history. Historical cycles typically followed a sharper, shorter trajectory. The downturns of 1974 and 1979 essentially played out and bottomed within 12 months. The 1980 cycle, triggered by the Volcker disinflation, found its floor around month 18. Even the catastrophic 2005 housing bubble, which saw a deeper plunge of roughly 45% in existing home sales, largely ran its course within 36 months before establishing a new equilibrium. The 2021 cycle, by contrast, has been strikingly different. It was shallower in its initial decline, but rather than bouncing back, the market has flatlined at a depressed level with no meaningful recovery.

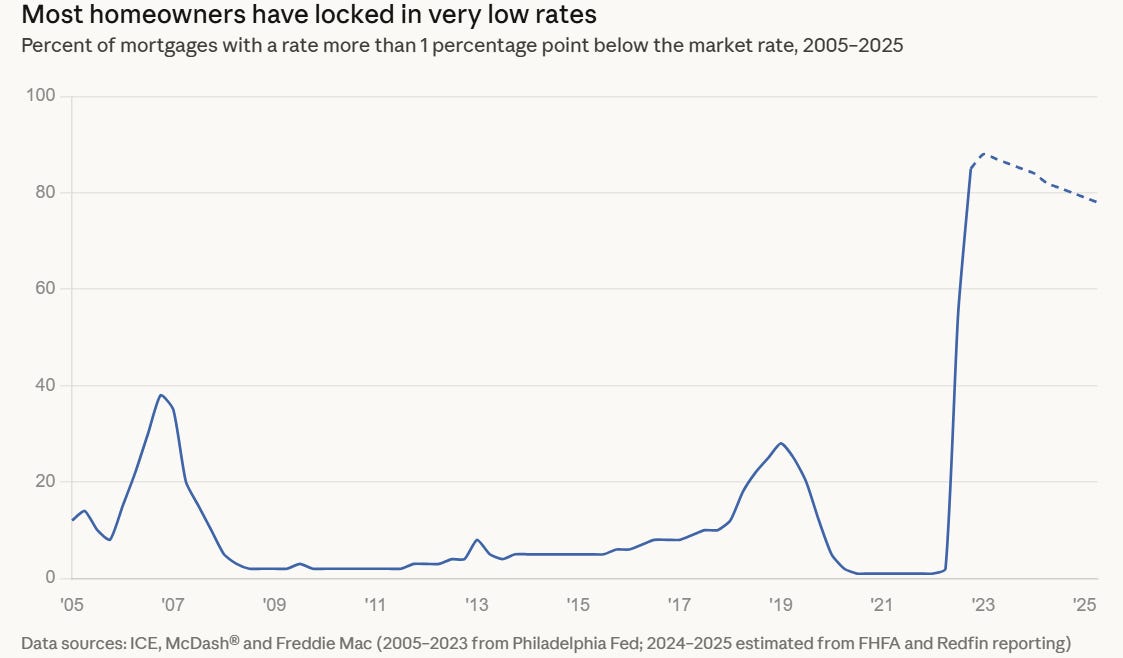

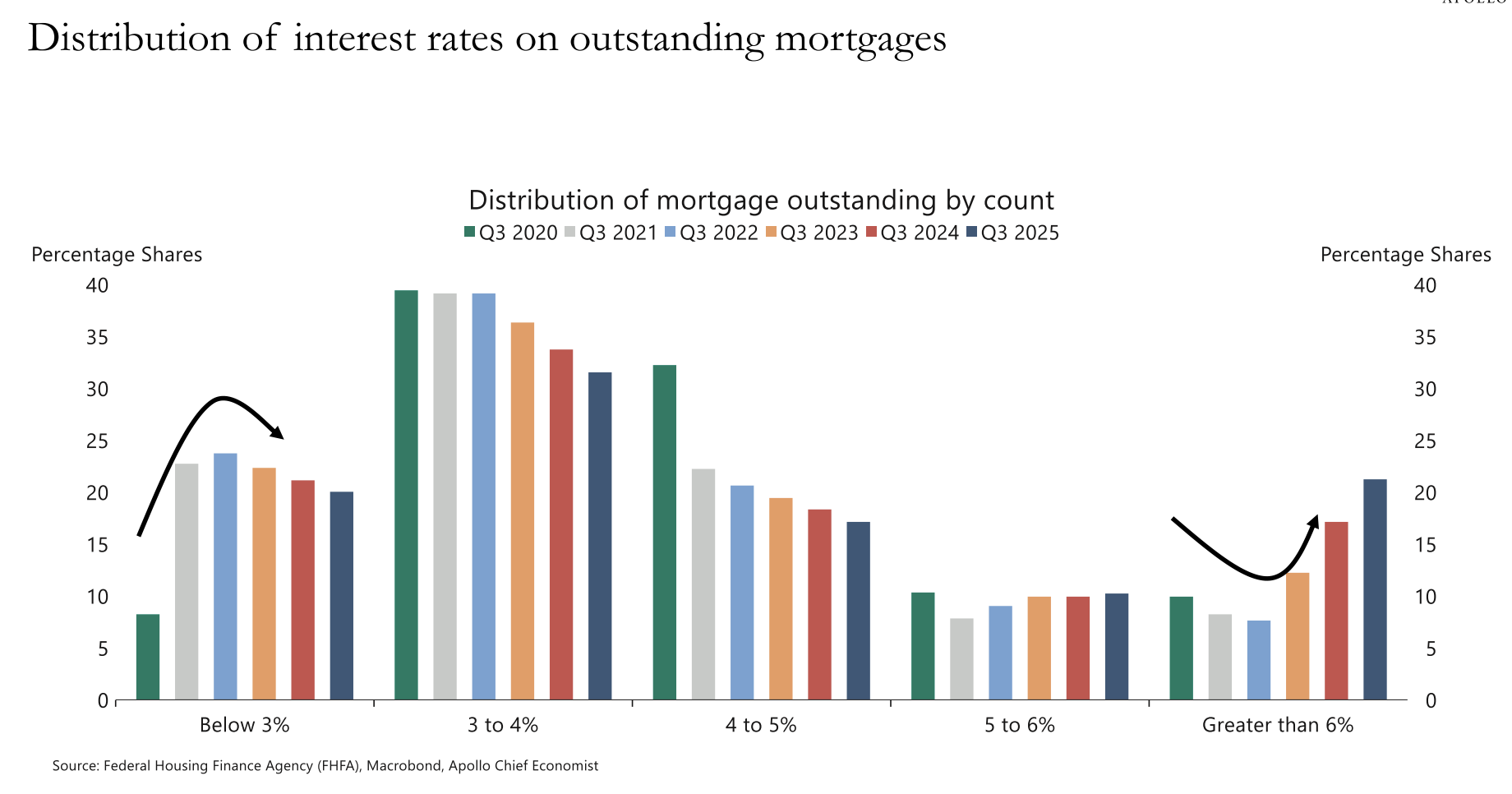

That pattern is, of course, consistent with the “lock-in effect” story: homeowners who locked in 3-4% mortgages in 2020–2021 have very little incentive to sell and take on a 6–7% rate, so existing home inventory stays suppressed and transaction volumes remain depressed. Nonetheless, I was still surprised just how unprecedented this dynamic is compared to the last two decades. The percent of outstanding mortgages with rate more than 100 bps below the existing market rate peaked at 88% in 1Q’23 which has been very gradually coming down over time.

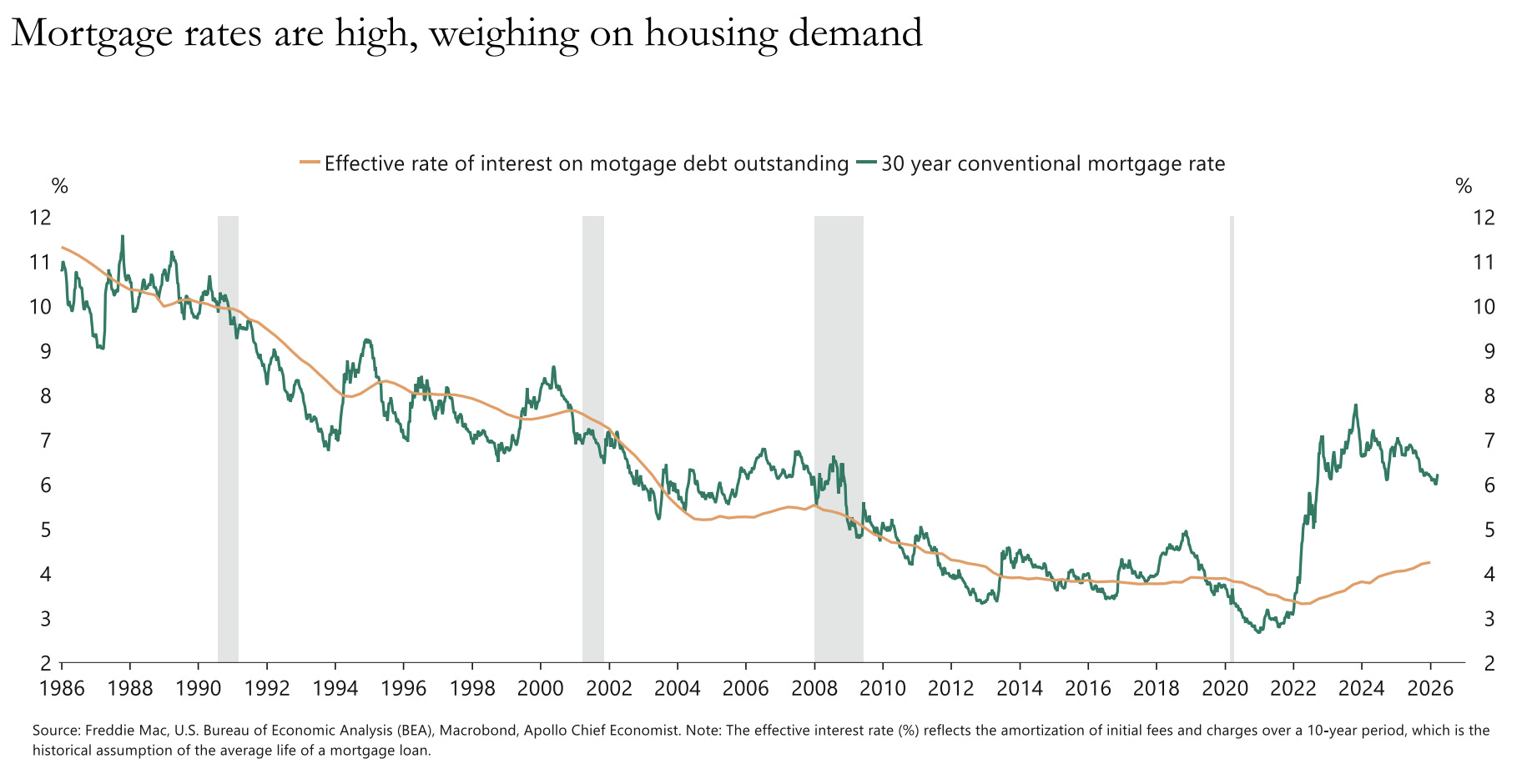

The gap between effective rate of interest on mortgage and the current 30-year fixed mortgage rate is unusually wide which is the primary culprit for the lock-in effect.

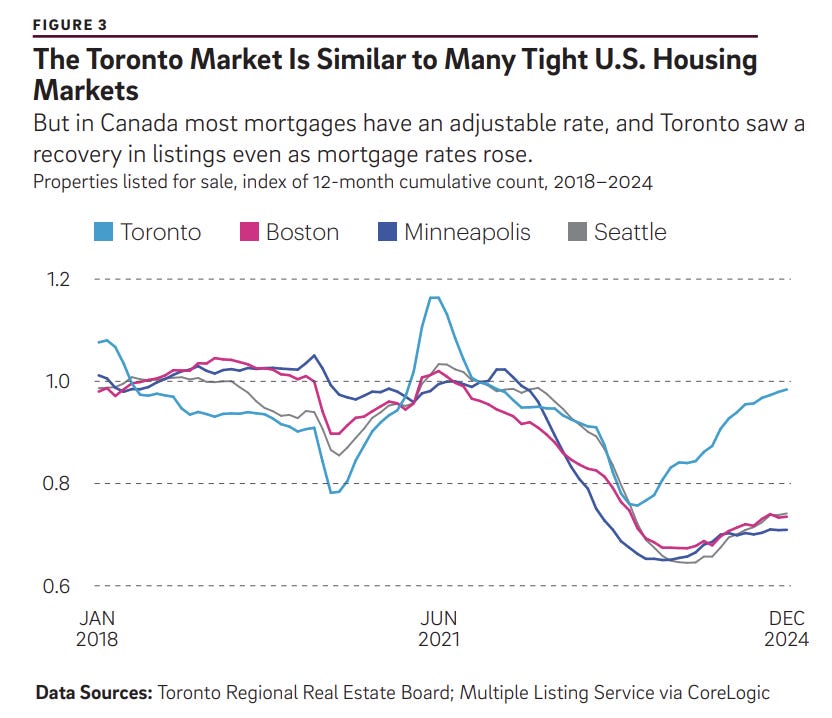

Indeed, when you look at housing markets such as Toronto which isn’t blessed with 30-year fixed mortgage rates, it becomes abundantly clear that lock-in effect is the dominant force in keeping the housing turnover low in the US.

In fact, this piece by a Senior Economist at the Federal Reserve Bank of Philadelphia highlights the pernicious impact of lock-in effect as it also tends to increase housing price. From the piece (emphasis mine):

Indeed, the very language and logic of “lock-in” presupposes that potential sellers are reluctant to re-enter the market as buyers because they are unwilling to reset the terms of their mortgage. Hence, lock-in of sellers is also “locking out” potential buyers, meaning demand has shifted with supply. If lock-out suppresses demand enough, the buyer/seller ratio could remain steady or even decrease.

The effect of lock-in on moving propensity is directly measured from mortgage and transaction data. But since we cannot see the housing market in a counterfactual world with only seller lock-in and not buyer lock-out, researchers have turned to models of the housing market. Using these models, they can estimate the net effects of the rate increase on the buyer/seller ratio and prices. The findings to date show that, on balance, lock-in is making markets slightly tighter, with a modest to moderate effect on prices. Using their estimates of sale probability and a model of housing tenure choice, Batzer, Coste, Doerner, and Seiler find that lock-in has prevented 1.7 million transactions and increased home prices by 7 percent.

Unfortunately, this lock-in effect so far can only be eroded through the typical 5 D’s of real estate (Divorce, Downsizing, Diapers, Diamonds, and Death). We are already seeing some of that as the percent of loans over 6% bottomed in Q2 2022 at 7.3% and has increased to 21.2% in Q3 2025. But relying on 5Ds will likely take us much longer than history to normalize the housing market.

Given this context, I will share some thoughts on Floor & Decor behind the paywall.

In addition to “Daily Dose” (yes, DAILY) like this, MBI Deep Dives publishes one Deep Dive on a publicly listed company every month. You can find all the 67 Deep Dives here.