How Elephants May Die

Hendrik Bessembinder's research indicates that ~4% of companies account for virtually all the excess return over the one-month Treasury bill rate in the US stock market since 1926. You have probably already come across this study before, but one of my inferences from this study was we may not fully internalize just how deeply challenging compounding is over the long term. As investor time horizon has shortened over time, we want to see signs of disruption right here and now even though in the real world a business may appear to chug along just fine quarter after quarter before starting its final phase towards obsolescence.

By now, you have likely consumed plenty of back and forth on SaaS debate and why one side is being obtuse or making the wrong arguments. However, this Benedict Evans’ thread is worth highlighting:

“One of my memories of the dotcom crash and the telecoms crash was every month or so, people said something that was really obviously stupid, both at the time and now looking back, and the stocks would go down 10-15%

But also, the stocks were way too expensive.

So really, what was happening was that these stories catalysed much more well-founded nervousness about valuation”

There may be plenty of stupid arguments the other side is making, but high valuation multiples can make stocks particularly amenable to even naive arguments, but can often later be backfilled with real, cogent case why a multiple de-rating makes much more sense.

But how about SaaS stocks that are objectively trading at a low multiple on actual GAAP earnings? Perhaps there is no better example than Adobe which is currently trading at ~12x LTM EV/EBIT multiple. At this point, it’s hard to argue anymore that the valuation multiple is not incorporating a lot of the AI risk in their valuation.

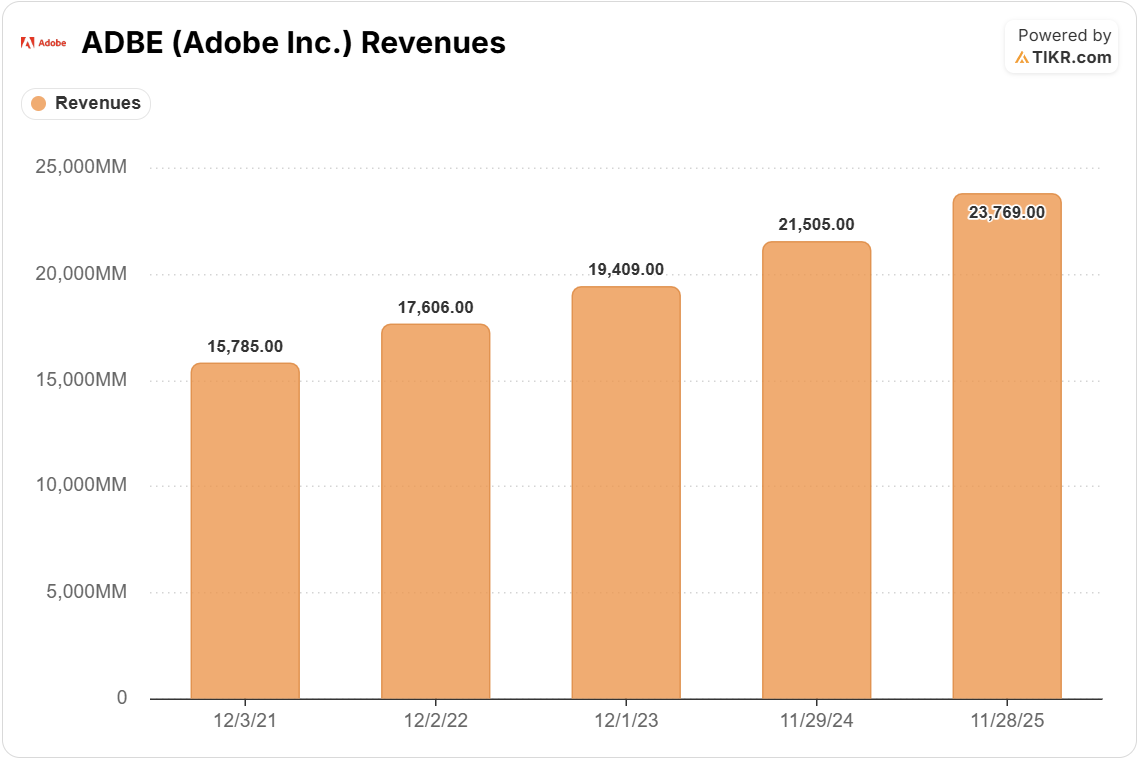

In fact, many Adobe shareholders often like to point out their revenue charts and ask rhetorically, “where is the AI disruption?” I wouldn’t, however, want to caricature all Adobe shareholders in a similar way. Bristlemoon Capital, despite owning Adobe, recently wrote perhaps one of the most thoughtful pieces on the Adobe debate in which they steel manned the other side. Once they have done that, they came away without high conviction that Adobe will be immune from AI risk.

The reality is AI model companies essentially run a psychological assault on current and potential Adobe shareholders almost on a weekly basis now. Just see Google’s recent blog posts related to Flow, Nano Banana 2, and Pomelli. Notice what Pomelli says in its tagline: “Easily generate on-brand content for your business”.

But isn’t 12x LTM EBIT enough to price these risks at this point? I will explore that question behind the paywall.

In addition to “Daily Dose” (yes, DAILY) like this, MBI Deep Dives publishes one Deep Dive on a publicly listed company every month. You can find all the 66 Deep Dives here.