Floor & Decor 1Q'26: Persistent Macro Challenges, but Pro Growth Encouraging

Floor & Decor (FND) posted an ugly quarter and provided an uninspiring outlook for the rest of 2026. In fact, given that FY25 was guided down at every revision i.e. three consecutive cuts across the four reports and that’s exactly also how 2026 started, I am a bit surprised that they haven’t given up on providing annual guidance yet. Ultimately, I don’t quite think FND management is in a position to provide an accurate outlook 12 months from now given macro is the primary driving force for their business in the near term. Despite somewhat easy comp, US existing home sales (EHS) went down in each of the first three months in 2026. There’s really not much FND management can do in the near term if EHS trend continues to deteriorate.

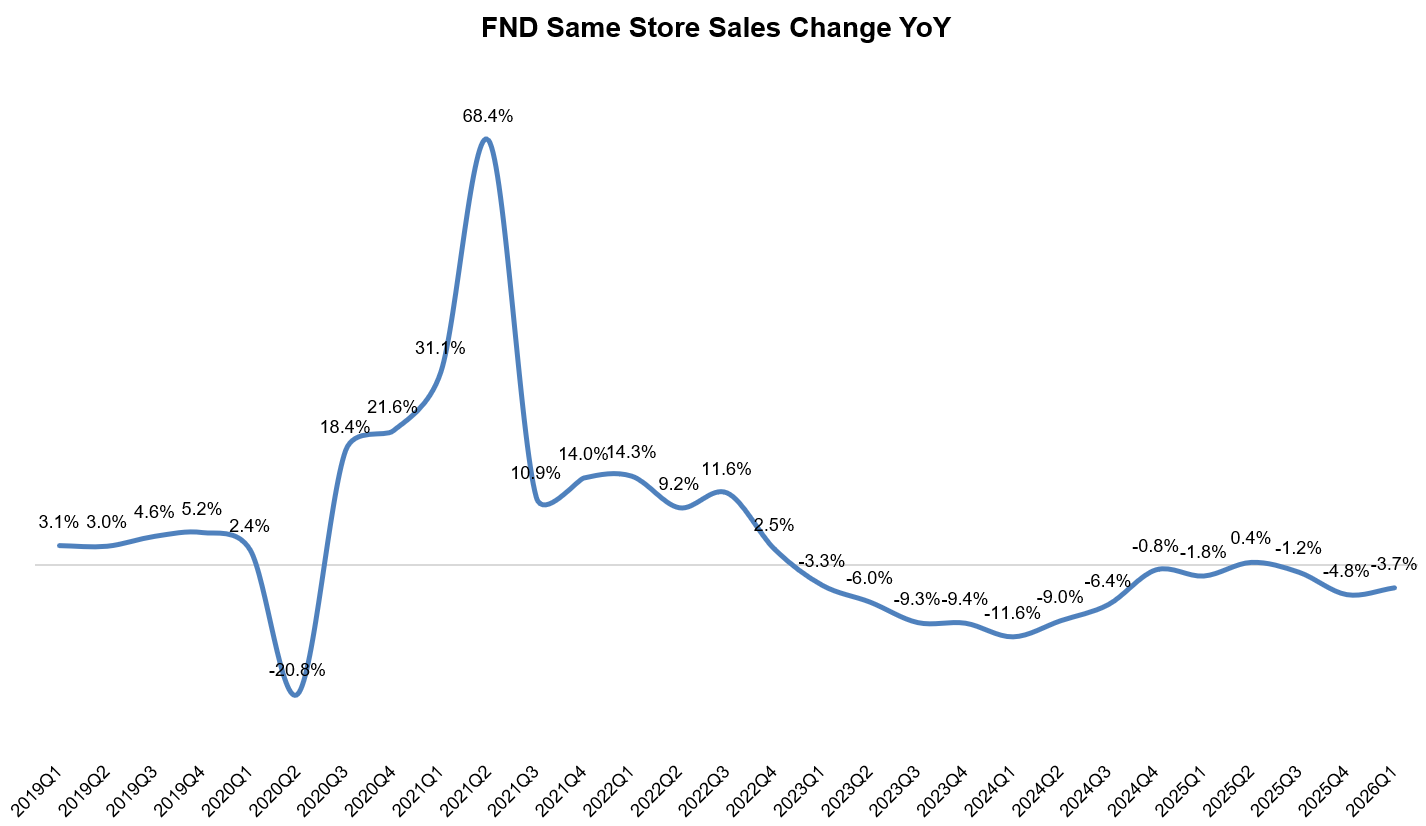

The fact that FND stock is largely flat after last week’s earnings is an indication how much pessimism was already embedded in FND’s stock price these days. Most investors suspected FND would have to navigate tough comp following the pandemic era EHS boost, but the length of the cycle perhaps surprised almost everyone. FND’s same store sales (SSS) was negative in 12 of the last 13 quarters! The only quarter that was positive in last three years was actually 2Q’25. Given such “touch comp”, you can be near certain that 2Q’26 SSS will also be negative. In fact, management mentioned April so far was -4.5%. Overall 2026 comp range outlook was guided down to flat to down 4% vs the initial guide range of -2.0% to +1.0%. We will see if they need to update it again next quarter!

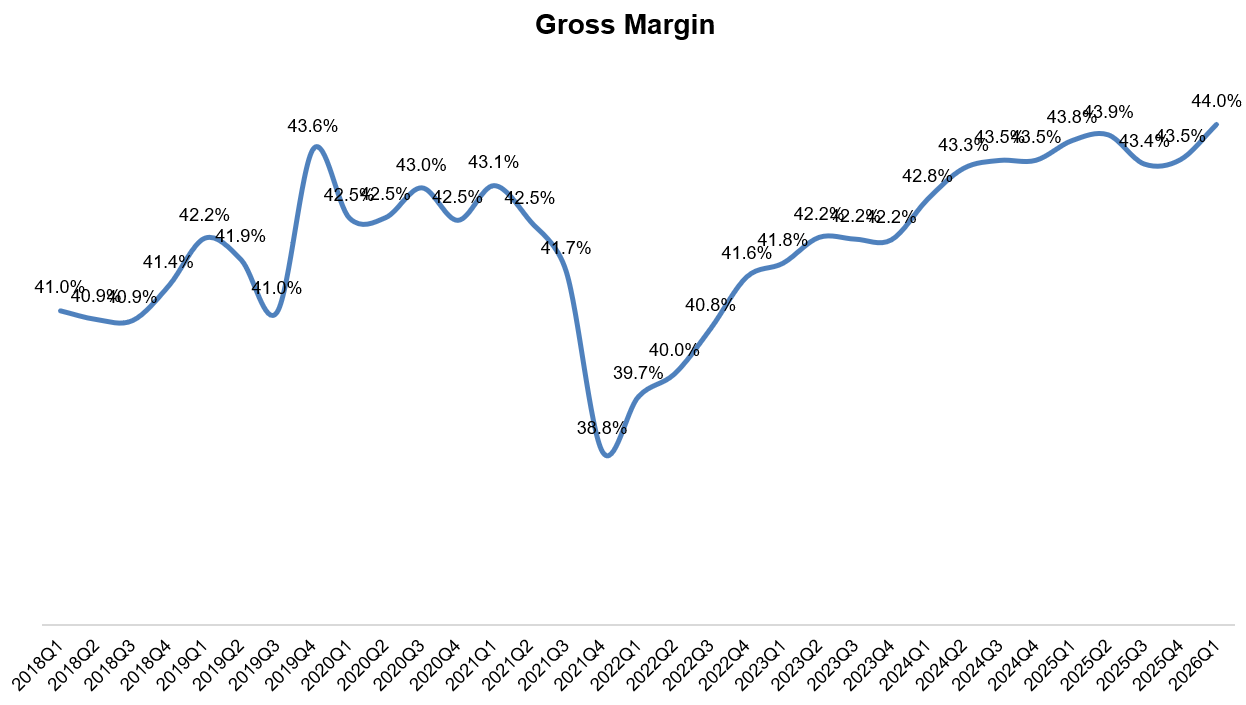

Considering such a brutal backdrop, it is a welcome surprise that FND actually posted its highest ever gross margin in 1Q’26. The biggest driver for margin expansion from 2021-22 trough levels has been the normalization of ocean container rates. Pricing has also been a tailwind. FND has good, better, and best product assortments. Even as transactions declined, the customers who are shopping continue to skew toward better/best price points, which carry higher margin. In four of the last five quarters (including 1Q’26), average price was actually positive. It’s the number of transactions that has been the primary culprit for persistent negative SSS.

However, there is perhaps an underappreciated driver for FND’s long-term future which is getting masked during this terrible EHS trends which I will elaborate behind the paywall.

Subscribers get the daily journal and five+ years of Deep Dives, i.e. full-length analyses with financial models on 65+ companies. The daily is just how I think out loud between the Deep Dives!