Danaher 1Q'26 Update

Danaher had another somewhat uneventful quarter.

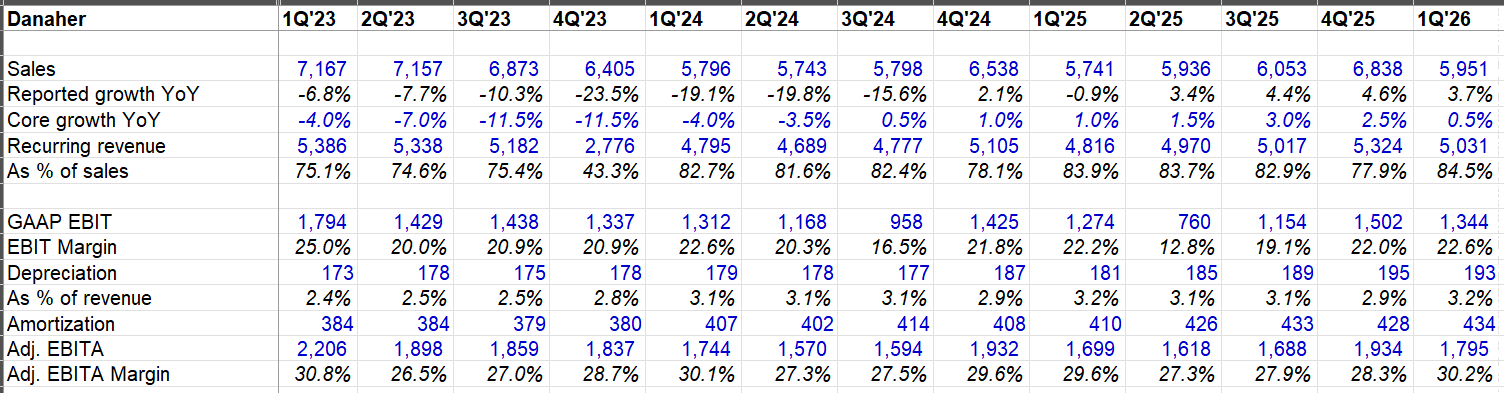

Looking at Danaher’s numbers every quarter is a stark reminder just how anemic the growth has proved to be for a company that enjoys some supposedly secular tailwinds. Even if you adjust for their spin-off of Environmental & Applied solutions segment in 2023, their topline in 1Q’23 would be $5.95 Billion. Three years later in 1Q’26, their topline remains the same: $5.95 Billion!

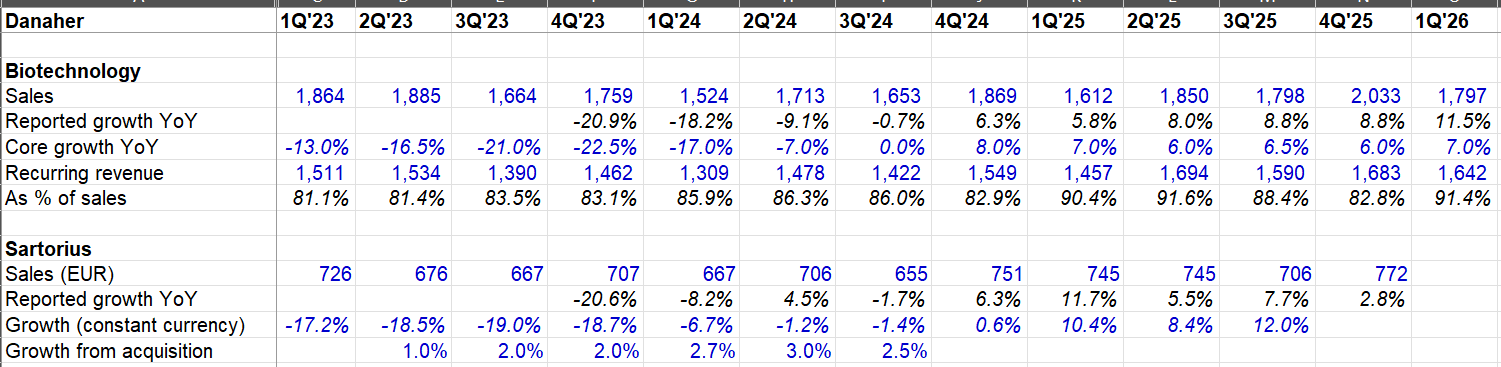

The picture is similar in their biotechnology segment. The inventory destocking that affected them in 2023-24 period is clearly behind them, but growth is still uninspiring at ~6-7%. Sartorius Stedim Biotech, which is more of a pure-play bioprocessing comp, will announce their earnings tomorrow, but their trend has been somewhat similar over the last few years.

But there are signs that we may see a better growth trajectory in the second half and beyond. I will particularly highlight management’s commentary on order growth:

Equipment declined modestly in Q1, but we were encouraged to see orders growth of more than 30%, marking the first quarter of year-over-year equipment order growth in nearly 2 years.

QoQ decline is not surprising since there is some seasonality to it, but if order growth continues at a sustained pace, Danaher’s bioprocessing business should return to comfortable double digit growth.

Margin in biotechnology segment improved YoY to reach 42.7% in 1Q’26. For context, margin in this segment peaked at 46.4% in 2021.

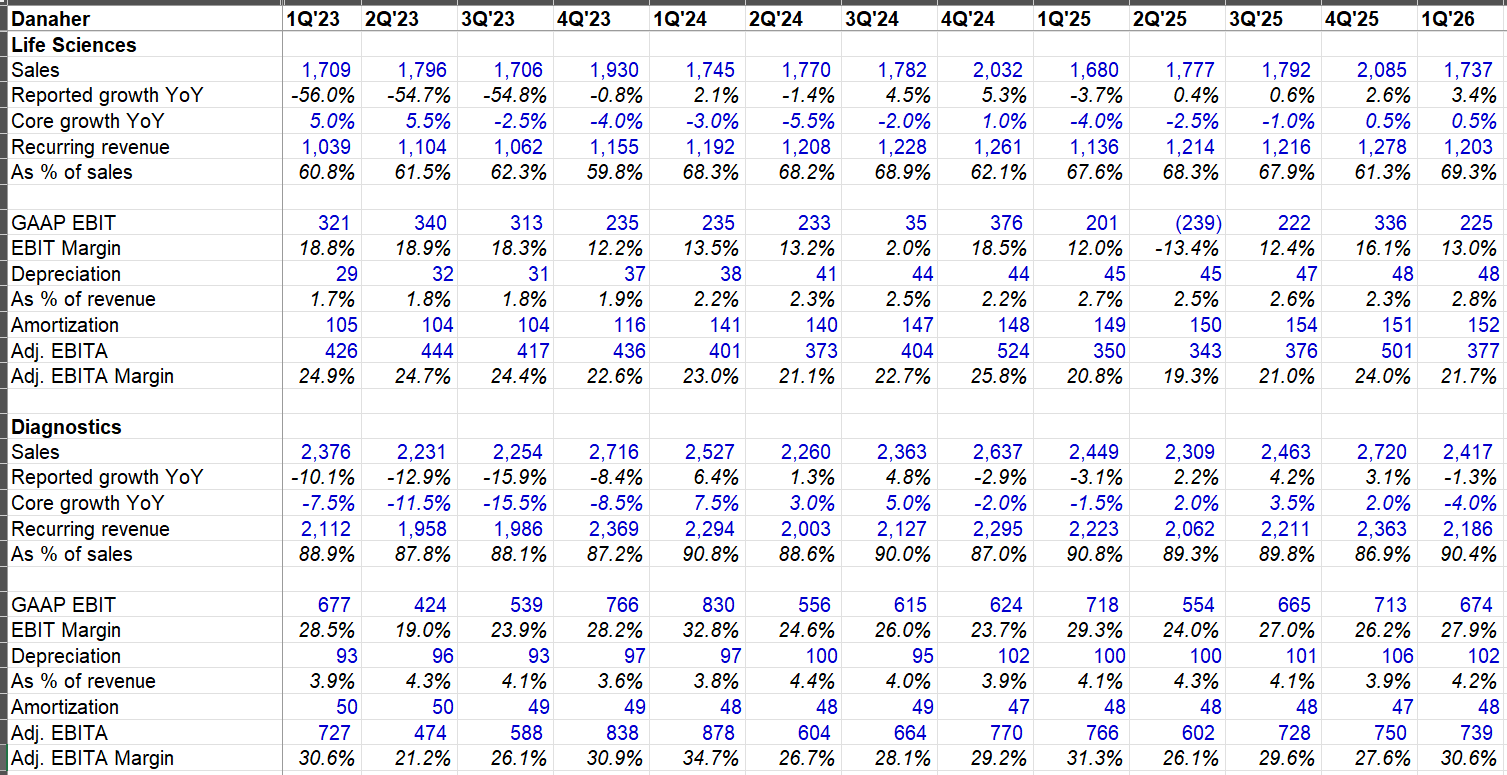

Life Sciences segment’s core revenue grew at only 0.5% despite having an easy comp of -4% in 1Q’25. At least, that’s better than the Diagnostics segment whose core revenue declined by 4% in 1Q’26 despite, again, pretty easy comp of -1.5% in 1Q’25. I won’t bore you with details of headwinds described by management, but these segments have been going through some really uninspiring performance for a while now.

The more inspiring bit during the call yesterday was when an analyst asked about AI’s potential impact on Danaher’s Life Sciences and Diagnostics segment. Rainer Blair, CEO of Danaher, said the following in response (emphasis mine):

“…we think AI is going to be a growth accelerator for the pharma and biotech industry, both in the near and in the long term. And the reason for that is we think that AI will accelerate the drug development and commercialization flywheel and result in better development pipeline yields. So as you know, the average yield in the drug development pipeline today is just above 10%. There’s an enormous opportunity here to improve the yield of the pipeline and to accelerate the biopharma flywheel along with the flywheels of life science tool providers like ourselves.

And so this improved yield drives both growth and profitability and reinvestment in the pharma industry. And that, of course, in turn, drives more investment into discovery, including wet lab validation, development in the clinic as well as commercial drug manufacturing. So in the short term, what we’re seeing actually is incremental more demand, which we expect to accelerate in the building of biologic models. Autonomous science is the current buzzword that refers to the building of biologic models, and of course, that requires automation, which we’re very well represented in. It requires more analytical instruments and it requires more reagents as well. So that’s the short-term impact as this practically new market segment of autonomous science starts to play out here, and that plays out first in discovery and then continues to accelerate through the development pipeline.

And of course, we’re very well positioned here with our life science tools. I mentioned automation, analytical instruments that, of course, increasingly are AI-enabled reagents that support all of those models going forward. And that’s a several year driver. These biologic models are in the single-digit percentage of information coverage required, very different than large language models. These biologic models require significantly more information in order to become general use type of model. So that’s the short term.

And as I indicated then in the long term, what we’re going to see is the cycle time of pharma development being compressed and the hit rate, i.e., the yield to be increased. And that flywheel is going to be very good for patients. It’s going to be very good for the pharma industry and those partners like ourselves that support that industry.

Now as you think about that going through development…these more commercialized drugs means more business for our bioprocessing business. We're the best positioned there with the broadest and deepest portfolio…then lastly, a lot of these drugs are going to be more sophisticated. They are going to require more sophisticated, more accurate diagnostics. If they're not personalized diagnostics, they will require near personalized diagnostics to come online.”

I haven’t done enough work to assess Danaher management’s point of view, but let me share what gives me bit of a pause here. Last week, Max Jaderberg, chief AI officer, and Sergei Yakneen, chief technology officer at Isomorphic Labs appeared on Nvidia AI podcast and shared a vision for the future that may have bit of a tension with the future Danaher likes to imagine. Notice what Nvidia mentioned in their blog (emphasis mine):

“By modeling cellular processes with AI, Isomorphic’s teams can predict molecular interactions with exceptional accuracy. Their advanced AI models enable scientists to computationally simulate how potential therapeutics interact with their targets in complex biological systems. Using AI to reduce dependence on wet lab experiments accelerates the drug discovery pipeline and creates possibilities for addressing previously untreatable conditions.”

If AI lets you do order of magnitude more simulation than you ever could through actual experimentation, wouldn’t that be a potentially secular headwind for at least some part of Danaher’s business? As I have mentioned before, I haven’t done enough work here, so I don’t have a strong opinion yet. But I’m also quite not ready to believe the halcyon future of AI being a secular tailwind for Danaher that management likes me to believe.

Management kept their core revenue guidance of ~3-6% but raised the high end of 2026 EPS guidance from $8.5 to $8.55.

On capital allocation, Danaher maintains its bias to do more M&A. They have already announced they’re going to acquire Masimo for $9.9 Billion. Management mentioned that they believe the acquisition will be accretive at all levels (gross and operating margins) and reach HSD ROIC in year 5. HSD ROIC in year 5? This type of uninspiring ROIC is exactly why I decided to sell the stock late last year. Scuttleblurb in a more recent post also explained why such ROIC trajectory is unlikely to change anytime soon, if ever (emphasis mine):

“The high-single digit ROIC that management expects to achieve on Masimo within 5 years may be disappointing to those who remember the days when the bogey for large platform acquisitions was set at 10%. But targets of significant enough size to move the needle for a buyer as large as Danaher are in scarce supply and generally aren’t managed by idiots who sell at cyclical bottoms. Everyone knows these are valuable properties and I expect them to be taken out at prices that reflect this reality. The days of opportunistically seizing hidden gems at single digit forward EBITA multiples are long over.

I don’t doubt that Danaher will pull out of the current growth slump and eventually return to high-single digit organic growth. China is recovering, A&G demand will eventually come back, and the biologics tailwind remains as strong as ever. Over time, AI may accelerate the pace of drug discovery and streamline processes downstream of that. But it’s reasonable to expect that most of whatever free cash flow drops down from that will be deployed into M&A, the returns from which will drive much of the returns that shareholders realize. Over the last decade, Danaher has spent ~$47bn on life sciences-related acquisitions. EBITDA (ex. spin-offs) has grown by $5.6bn over the same period, implying somewhere in the neighborhood of ~9% after-tax returns over that period (if anything, this is generous since my calculation implicitly gives acquisitions credit for all of the $5.6bn increase in EBITDA over the past 10 years). Danaher will continue to compound value for shareholders, though perhaps at a more modest pace over the next 10 years compared to the last 20.”

Indeed, the next 10 years will likely be more modest than the last 20 for the stock. The starting valuation, despite the stock being flat for the last five years is still on the high-teens. You can, of course, rightly argue that the quality of the business Danaher owns today is likely much better than the collection of industrial assets it owned in 2000-10 period, but the point still remains.

In addition to “Daily Dose” (yes, DAILY) like this, MBI Deep Dives publishes one Deep Dive on a publicly listed company every month. You can find all the 67 Deep Dives here.

Current Portfolio:

Please note that these are NOT my recommendation to buy/sell these securities, but just disclosure from my end so that you can assess potential biases that I may have because of my own personal portfolio holdings. Always consider my write-up my personal investing journal and never forget my objectives, risk tolerance, and constraints may have no resemblance to yours.

My current portfolio is disclosed below: