Adobe's Continued Deceleration

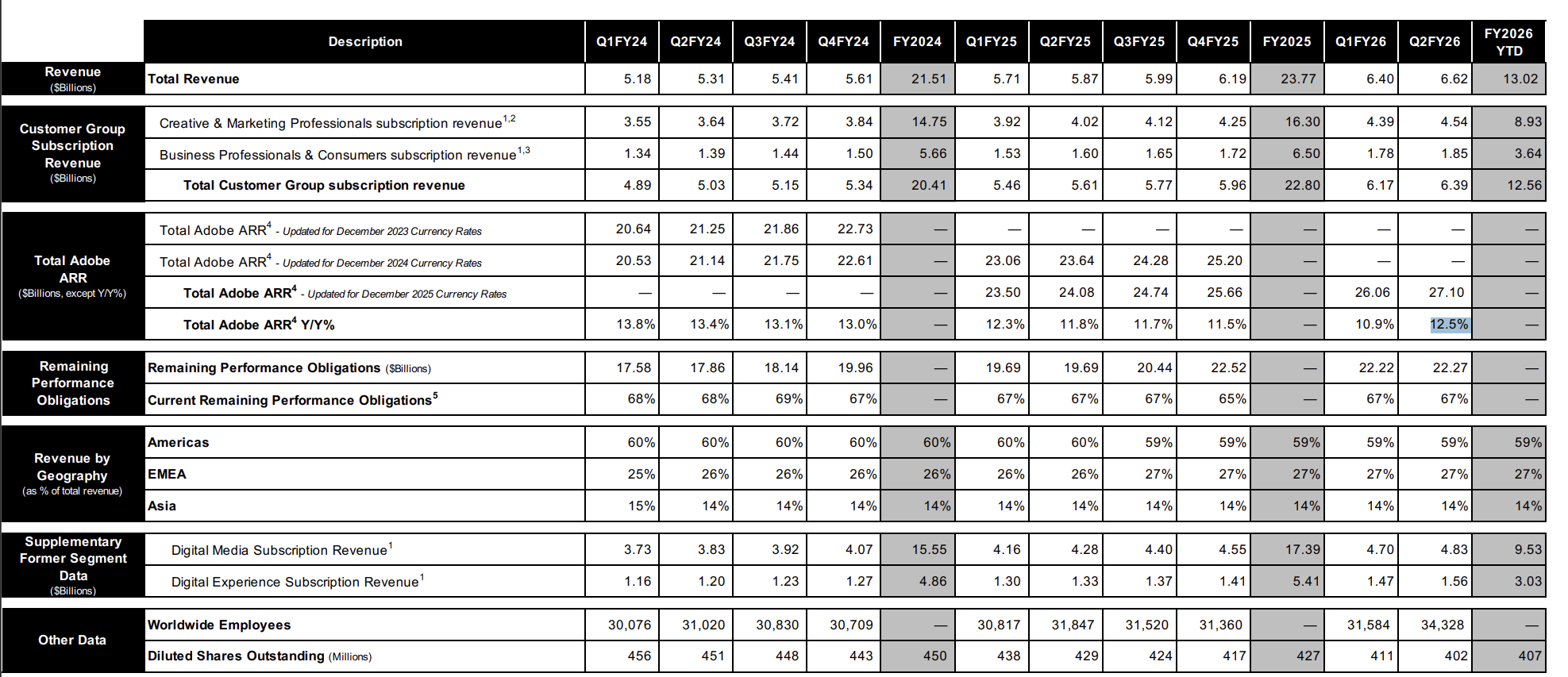

If you’re on X (formerly known as “twitter”), you may be under the impression that Adobe’s growth has accelerated in FY 2Q’26 as I noticed quite a few posts mentioning how total ARR has finally accelerated last quarter. Unfortunately, Adobe’s ARR included $480 million from the recent Semrush acquisition. Once you adjust for the acquisition, the organic ARR growth was 10.5% which implies a ten consecutive quarters of deceleration in revenue growth. That doesn’t quite inspire a lot of confidence!

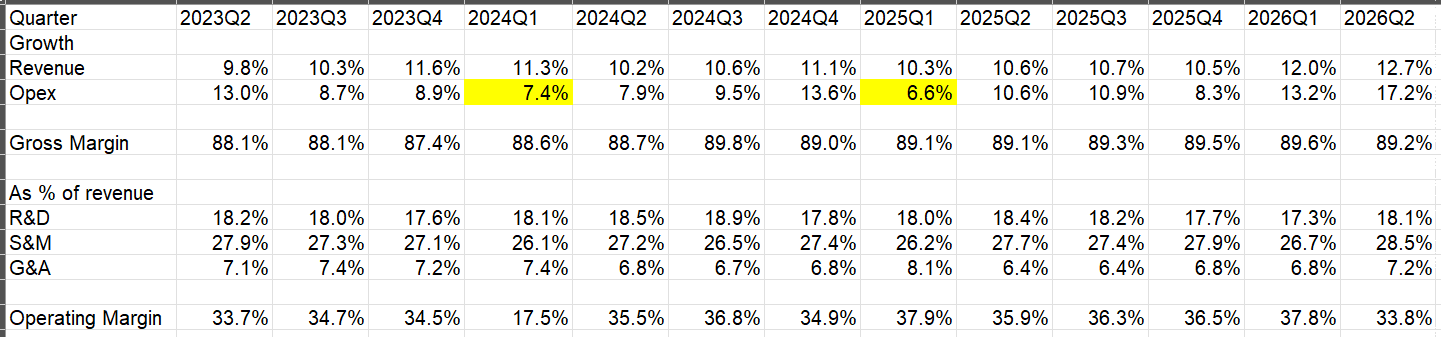

What also doesn’t inspire a lot of confidence is when you notice opex growth of ~17% surpassing revenue growth of ~13% last quarter. However, this opex growth was affected by $70 million non-cash goodwill impairment on the publishing & advertising unit, $30 million loss contingency tied to a litigation settlement, and $5 million Semrush acquisition related expenses. Once you adjust for all these, opex growth would be ~14% YoY which is still a touch above revenue growth last quarter.

Perhaps the more pressing concern was that management maintained its FY’26 Total ARR growth target of 10.2%, but only by folding in the ~$480 million of ARR that came with Semrush which closed in April. Remember, Adobe originally guided for 10.2% ARR growth for FY’26 in their FY 4Q’25 call. So, the fact that they didn’t change the guide despite Semrush acquisition implies they have effectively guided ARR growth down in 2Q’26 call. Adjusting for Semrush acquisition, now their FY’26 growth came to only 8.3% which is almost ~200 bps below the original guide. The high single digit organic growth outcome I called “quite conceivable” in my last Adobe update is now embedded in the guide itself. Management has tried to make the case that they’re intentionally making a short-term trade-off to go after a more compelling longer term opportunity. From the call (emphasis mine):

Our FY '26 total Adobe ARR growth target of 10.2% now reflects both the addition of the Semrush book of business as well as the strategic choice to accelerate MAU freemium growth and defer previously planned Creative Cloud line optimizations. We believe this is the right long-term strategy to expand our customer base and strengthen the foundation for durable growth.

…We believe now is the time to aggressively acquire the next generation of Adobe loyalists. The strategic shift to acquire more freemium customers through Adobe and Firefly lowers our second half ARR growth expectations from individual subscribers. We believe these changes do make Adobe even stronger.

Unfortunately, the messengers are leaving. Narayen announced his retirement in March and remains CEO only until the board finds a successor. Adobe also disclosed that CFO Dan Durn is departing. Management explicitly said the next CEO will own FY’27 planning, and Narayen said the payback from this pivot “will play out, I think, over 2027.” In other words, the team making this promise will largely not be the team delivering on it. Charitably, an outgoing CEO has nothing left to prove and is clearing the deck so his successor starts from a cleaner base. We will have to wait and see if that is indeed the case.

Adobe stock has, of course, been continually punished over the last couple of years and now trades at HSD LTM EV/EBIT multiple.

Many investors understandably wonder whether much of the risk is priced in, perhaps more so than deserved. Software investors who are typically not accustomed to looking at HSD multiples on actual (not fake) operating earnings can be prone to thinking that the stock is priced for death in not-so-distant future. If you feel too tempted, I encourage you to re-read my piece “How elephants may die”:

Serious investors may scoff at the idea of narrative driving the valuation for many companies, but the reality is when it becomes very, very hard to articulate why a company will become more relevant over time and be able to protect its profit pool, the spreadsheet may not be able to rescue such a company. If anything, the spreadsheet may be a lethal tool to show that the company can grow topline for years and still fail to be attractive for the long-term shareholders.

Subscribers get the daily journal and five+ years of Deep Dives, i.e. full-length analyses with financial models on 65+ companies. The daily is just how I think out loud between the Deep Dives!

Current Portfolio

Please note that these are NOT my recommendation to buy/sell these securities, but just disclosure from my end so that you can assess potential biases that I may have because of my own personal portfolio holdings. Always consider my write-up my personal investing journal and never forget my objectives, risk tolerance, and constraints may have no resemblance to yours.

My current portfolio is disclosed below: