Airbnb’s Cost of Market Creation and Regulatory Survival

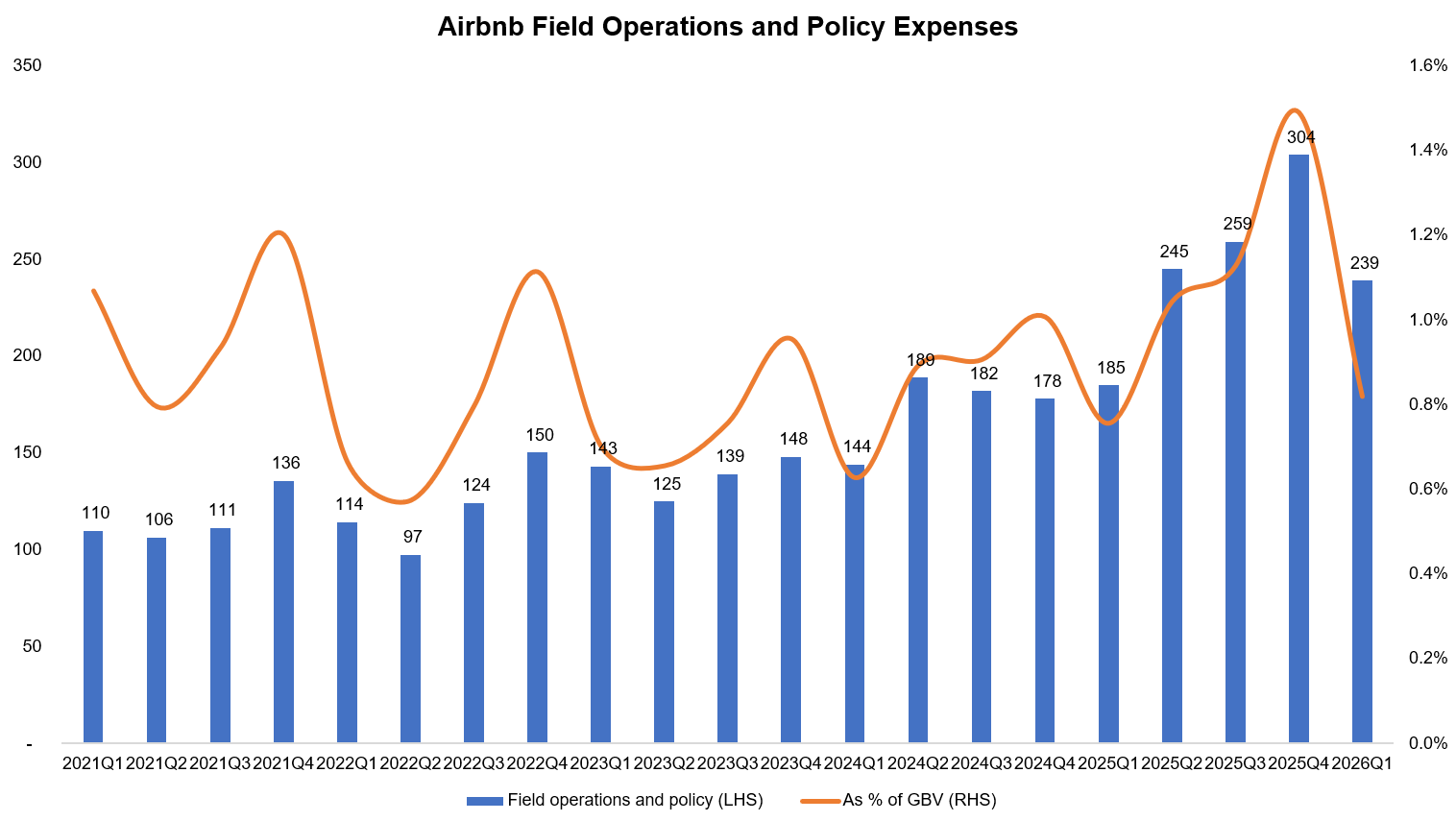

Airbnb is one of those rare marketplaces that derive supermajority of its demand organically and hence, they have the privilege of mostly not needing to pay Google et al for traffic. However, Airbnb appears to have a different “recurring” expense to keep their business growing: field operations and policy expenses which is reported under Sales & Marketing (S&M). To underscore the significance of these costs, let me point out that ~40% of Airbnb’s last year’s S&M was actually field operations and policy expenses. What exactly are these expenses? I explained in a piece early this year:

Field operations basically account for the employees who manage specific local markets, recruit new property Hosts, run host-community events, and manually build localized housing supply to meet traveler demand. As Airbnb started focusing beyond the five core markets, I suspect such field operations cost had a noticeable bump.

Moreover, because Airbnb’s business model can potentially impact local housing markets, it faces intense regulatory scrutiny. This likely necessitates armies of lobbyists, lawyers, and policy experts who negotiate with city councils, mayors, and national governments regarding short-term rental bans, zoning laws etc. As a market leader of alternative accommodation, Airbnb must tackle these issues. This can actually be good news for its competitors such as Booking who can largely coattail on Airbnb’s spending on such regulatory efforts.

As you can see, since there are a lot of different things bucketed in this reporting cost line item, it’s hard to pinpoint what exactly is driving the expenses. Even though I would expect to see operating leverage in this cost line item over time, that’s not what we have seen so far. For example, back in 2021, Airbnb spent 1.0% of its Gross Booking Value (GBV) on field operations and policy expenses. Since then, Airbnb’s GBV almost doubled by 2025. And yet, Airbnb’s field operations and policy expenses was actually 1.1% of its GBV in 2025, implying not much of an operating leverage at all.

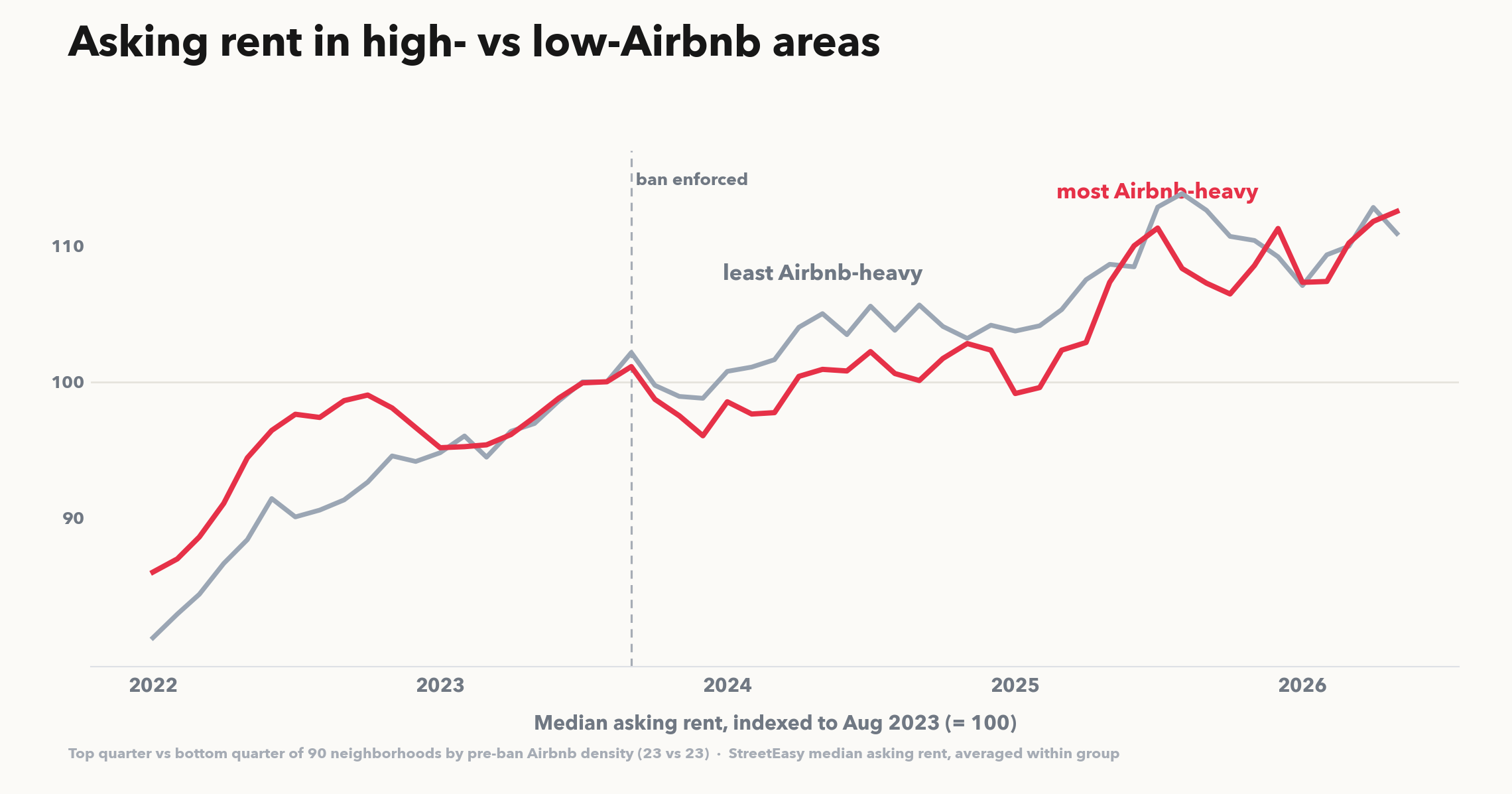

The reality is over the last few years, the regulatory headaches around the impact of short-term rentals on housing has been intensifying. The poster child for such headache is New York City. Almost three years ago, NYC flipped the switch on Local Law 18, its short-term-rental registration and platform-verification regime. Local Law 18 required hosts to register with the city and effectively banned unhosted stays under 30 days which predictably led to a collapse of Airbnb’s supply in NYC. The Office of Special Enforcement says there were more than 38,000 active listings at the start of 2023; by 2025, New York had only 3,000 active short-term-rental registrations. The promise from the law's backers seemed quite simple and intuitive: those units would come back to the long-term market, supply would loosen, and rents would ease.

Jay F. at The Data Stream recently tried to answer whether the reality matches the promises three years after the de-facto ban on Airbnb. He compared rent trends in neighborhoods with high and low concentrations of Airbnb listings, using asking-rent data from both Zillow and StreetEasy. This is what he found (emphasis mine):

“I ran an event-study difference-in-differences: comparing rent trajectories in high-density versus low-density areas, within the same borough and controlling for new construction. To summarize, there was no notable effect size. The best estimate is that the ban saved the typical renter about $52 a year but with a confidence interval of -$71 to +$175 .”

As you can see above, asking rents in the most Airbnb-heavy neighborhoods did not clearly break away from rents in the least Airbnb-heavy group after enforcement. If anything happened, it is difficult to distinguish from ordinary neighborhood-level noise. This should not be particularly surprising. The Data Stream estimates short-term rentals were only 0.59% of New York’s rental stock before the crackdown. Even if every banned listing became a conventional rental, the supply shock would still be small relative to the city. In reality, only 42% of the affected listings had adopted a 30-night minimum by January 2024. Another 44% disappeared from Airbnb, which does not tell us whether they became year-long rentals, returned to owner use, or something else. NYC may not be an exception either since back in 2019, Barron, Kung & Proserpio's US-wide study also would predict relatively minor impact of Airbnb on rent and housing prices. From the US-wide study back in 2019:

“At the median owner-occupancy rate zipcode, we find that a 1% increase in Airbnb listings leads to a 0.018% increase in rents and a 0.026% increase in house prices”

Even though Airbnb has grown lot more since 2019, it appears the impact of Airbnb remains somewhat insignificant. Nonetheless, I’m not quite sure to what extent such data would convince NYC or other cities to not give into such populist impulse of banning short-term rentals. Perhaps everyone loves to find a bogeyman whom you can blame for rising rent or housing prices and as I alluded earlier, blaming Airbnb makes perhaps “intuitive” sense to most people. It is, however, telling that the impact of such ban may lead to unintended consequences. Again, from “The Data Stream”:

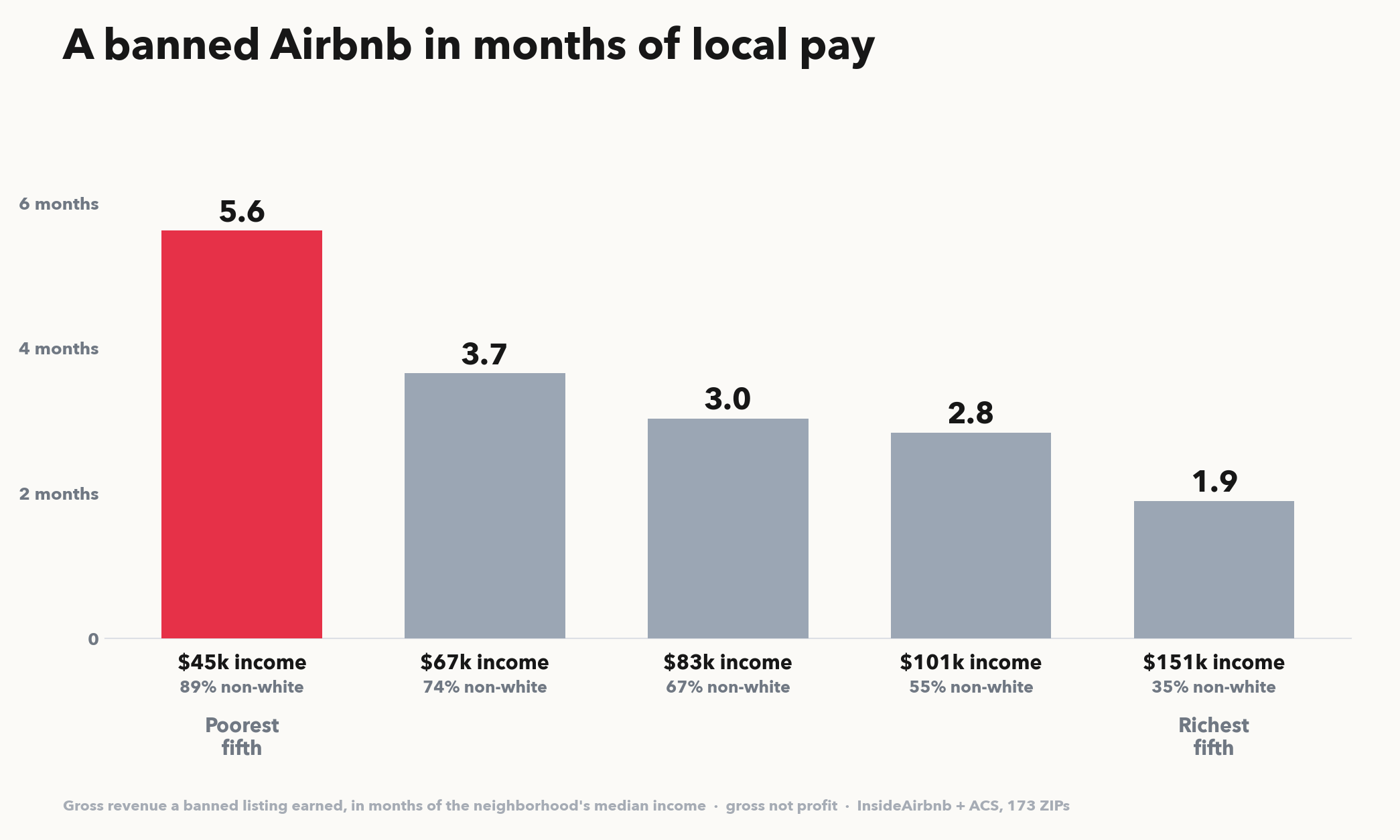

“one of the side-effects from the ban was its disproportionate impact upon the lower-income non-white residents that comprise these neighborhoods. In the richest fifth of zip codes, a lost listing was worth about two months of the neighborhood's median income. In the poorest fifth comprising 89% non-white, it was worth almost six”

So, while I do not necessarily think NYC’s ban would act as a cautionary tale to other cities who may ponder a similar ban, it is still a positive outcome for Airbnb that the evidence shows the impact of Airbnb is rather negligible on rent and housing prices. The opposite would be much more concerning; if NYC found more concrete evidence of Airbnb’s “culpability”, you could imagine plenty of other cities would use that as a further ammunition to capitalize on the sentiment and ban short-term rentals in their cities. Airbnb is fairly resilient to any city specific regulations since no city represents more than 1% of its revenue, but of course it could be become a major headache if very restrictive policies spread like a wildfire to more and more cities over time. In that light, the outcome of NYC ban is bit of a sigh of relief for Airbnb. However, as long as Airbnb continues to fight these regulatory battles, the field operations and policy costs may not see much operating leverage! Airbnb mostly escaped Google’s taxes for generating incremental demand, only to perhaps find themselves in regulatory tentacles that may not go away anytime soon.

Subscribers get the daily journal and five+ years of Deep Dives, i.e. full-length analyses with financial models on 65+ companies. The daily is just how I think out loud between the Deep Dives!

Current Portfolio

Please note that these are NOT my recommendation to buy/sell these securities, but just disclosure from my end so that you can assess potential biases that I may have because of my own personal portfolio holdings. Always consider my write-up my personal investing journal and never forget my objectives, risk tolerance, and constraints may have no resemblance to yours.

My current portfolio is disclosed below: